Statement of Profit or Loss (Cambridge (CIE) A Level Business): Revision Note

Exam code: 9609

The purpose of the statement of profit or loss

The statement of profit or loss shows the income and expenditure of a business over a period of time - usually a year - and identifies the amount of profit made

Statement of profit or loss: key terminology and calculations

Term | Explanation |

|---|---|

Sales revenue |

|

Cost of sales |

|

Gross profit |

|

Expenses |

|

Profit from operations |

|

Taxation |

|

Profit for the year |

|

Dividends |

|

Retained earnings |

|

The structure of the statement of profit or loss

The statement of profit or loss is divided into three parts

The trading account

The profit and loss account

The appropriation account

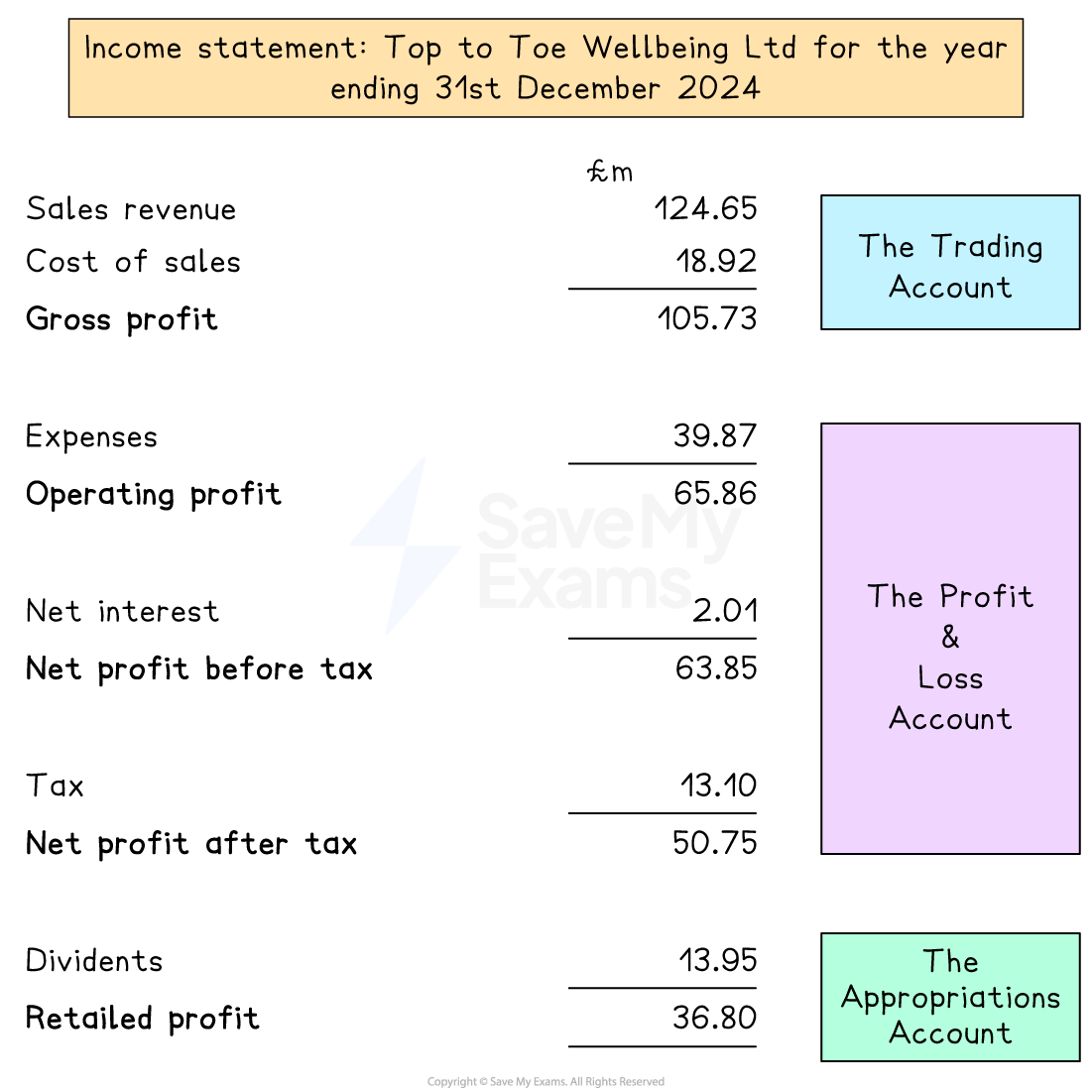

An example income statement

The trading account

The trading account is where the cost of sales is deducted from sales revenue to calculate the gross profit

In 2024 Top to Toe Wellbeing Limited's sales revenue was £124.65m and its cost of sales were £18.92m

The gross profit for the period was therefore

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2214%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2243.5%22%20y%3D%2214%22%3E124%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2258.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2269.5%22%20y%3D%2214%22%3E65%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2283.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22100.5%22%20y%3D%2214%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22117.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22131.5%22%20y%3D%2214%22%3E18%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22141.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22152.5%22%20y%3D%2214%22%3E92%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22166.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2251%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2251%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2243.5%22%20y%3D%2251%22%3E105%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2258.5%22%20y%3D%2251%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2269.5%22%20y%3D%2251%22%3E73%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2283.5%22%20y%3D%2251%22%3Em%3C%2Ftext%3E%3C%2Fsvg%3E)

The profit and loss account

The profit and loss account deducts a series of expenses to determine the operating profit for the period

In 2024 gross profit was £105.73m and expenses were £39.87m

The operating profit was therefore

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2214%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2243.5%22%20y%3D%2214%22%3E105%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2258.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2269.5%22%20y%3D%2214%22%3E73%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2283.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22100.5%22%20y%3D%2214%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22117.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22131.5%22%20y%3D%2214%22%3E39%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22141.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22152.5%22%20y%3D%2214%22%3E87%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22166.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2251%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2251%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2251%22%3E65%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2250.5%22%20y%3D%2251%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2261.5%22%20y%3D%2251%22%3E86%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2251%22%3Em%3C%2Ftext%3E%3C%2Fsvg%3E)

The business also paid £2.01m interest

The profit before tax was therefore

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2214%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2214%22%3E65%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2250.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2261.5%22%20y%3D%2214%22%3E86%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2292.5%22%20y%3D%2214%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22109.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22119.5%22%20y%3D%2214%22%3E2%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22125.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22136.5%22%20y%3D%2214%22%3E01%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22150.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2251%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2251%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2251%22%3E63%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2250.5%22%20y%3D%2251%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2261.5%22%20y%3D%2251%22%3E85%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2251%22%3Em%3C%2Ftext%3E%3C%2Fsvg%3E)

The business also paid £13.10m tax

The profit after tax for the period was therefore

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2214%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2214%22%3E63%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2250.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2261.5%22%20y%3D%2214%22%3E85%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2292.5%22%20y%3D%2214%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22109.5%22%20y%3D%2214%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22123.5%22%20y%3D%2214%22%3E13%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22133.5%22%20y%3D%2214%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2214%22%3E10%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%22158.5%22%20y%3D%2214%22%3Em%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2251%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2226.5%22%20y%3D%2251%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2251%22%3E50%3C%2Ftext%3E%3Ctext%20font-family%3D%22math19df71cc037e14b064558084cb4%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2250.5%22%20y%3D%2251%22%3E.%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2261.5%22%20y%3D%2251%22%3E75%3C%2Ftext%3E%3Ctext%20font-family%3D%22Arial%22%20font-size%3D%2214%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2251%22%3Em%3C%2Ftext%3E%3C%2Fsvg%3E)

The appropriations account

The appropriations account shows how profits are distributed for the period

In 2024 Head to Toe Wellbeing Limited distributed £13.95m to shareholders as dividends

£36.80m was therefore retained as profit

Amending the statement of profit or loss

Making a change to one section of the statement of profit or loss has an impact on other sections

Worked Example

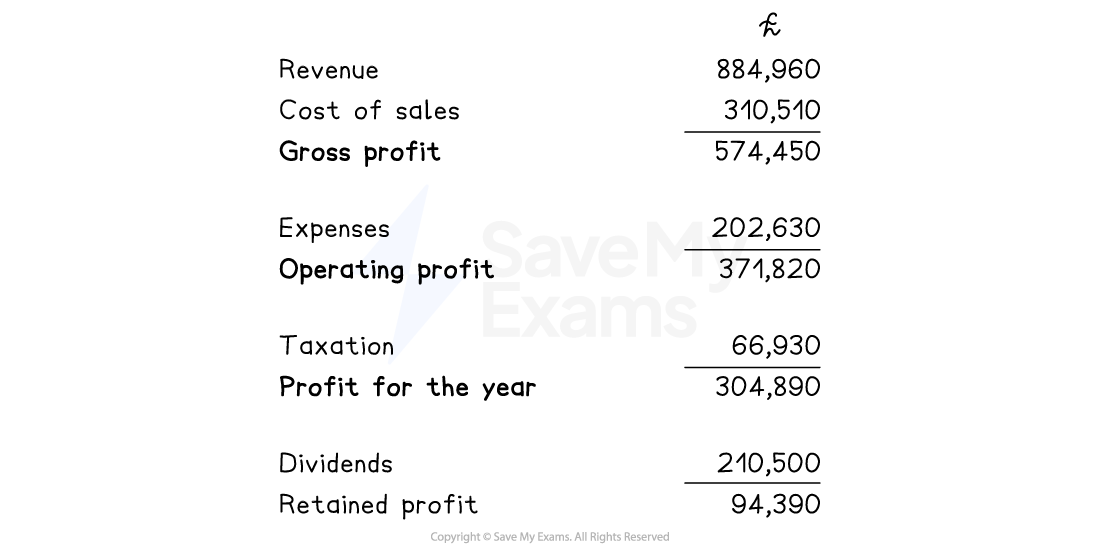

Pershore Plumbers Ltd's accountant has sent the interim statement of profit and loss to Helen, the business owner. She has been asked to check the statement before it is sent to Companies House

Pershore Plumbers Ltd - Statement of profit or loss for the year ending 31st March 2025

Helen identifies three errors

Sales revenue for the period was actually £889,540

The business received a tax refund of £12,220 during the year

The business paid dividends of £220,500 to shareholders

Recalculate the statement of profit or loss to reflect these changes.

(4)

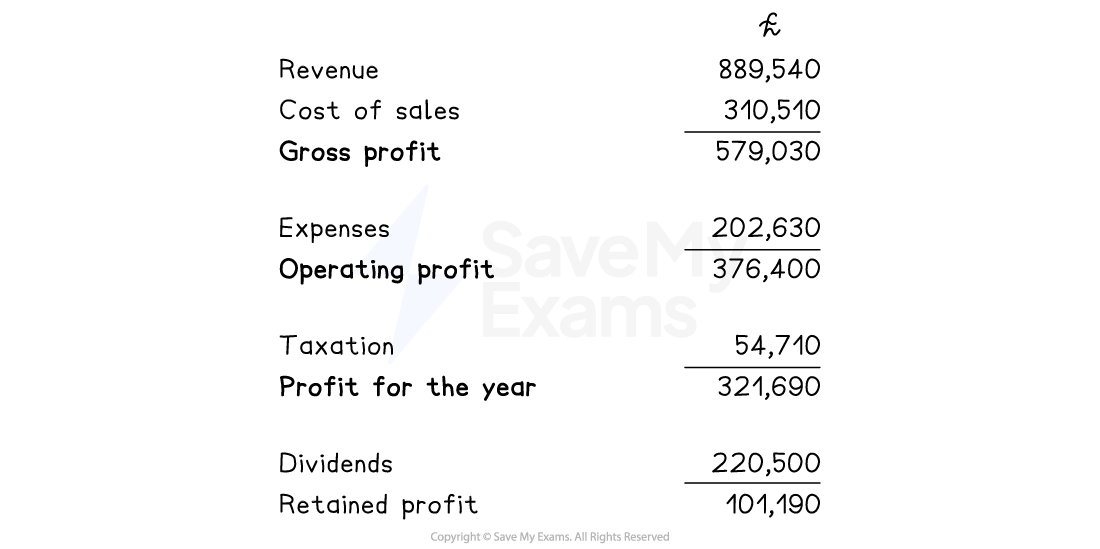

Step 1: Calculate gross profit given the updated revenue figure

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2221.5%22%20y%3D%2216%22%3EGross%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2266.5%22%20y%3D%2216%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2298.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22142.5%22%20y%3D%2216%22%3ERevenue%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22186.5%22%20y%3D%2216%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22215.5%22%20y%3D%2216%22%3ECost%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22243.5%22%20y%3D%2216%22%3Eof%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22272.5%22%20y%3D%2216%22%3Esales%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2263%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%2263%22%3E889%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%2263%22%3E540%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22105.5%22%20y%3D%2263%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22124.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2263%22%3E310%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22160.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22176.5%22%20y%3D%2263%22%3E510%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%22110%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%22110%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%22110%22%3E579%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%22110%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%22110%22%3E030%3C%2Ftext%3E%3C%2Fsvg%3E) (1)

(1)

Step 2: Recalculate operating profit

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2236.5%22%20y%3D%2216%22%3EOperating%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2296.5%22%20y%3D%2216%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22128.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22158.5%22%20y%3D%2216%22%3EGross%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22203.5%22%20y%3D%2216%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22235.5%22%20y%3D%2216%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22282.5%22%20y%3D%2216%22%3EExpenses%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2263%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%2263%22%3E579%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%2263%22%3E030%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22105.5%22%20y%3D%2263%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22124.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2263%22%3E202%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22160.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22176.5%22%20y%3D%2263%22%3E630%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%22110%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%22110%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%22110%22%3E376%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%22110%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%22110%22%3E400%3C%2Ftext%3E%3C%2Fsvg%3E) (1)

(1)

Step 3: Calculate profit for the year given the tax refund

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2214.5%22%20y%3D%2216%22%3ETax%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2240.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2259.5%22%20y%3D%2216%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2275.5%22%20y%3D%2216%22%3E66%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2286.5%22%20y%3D%2216%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22102.5%22%20y%3D%2216%22%3E930%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22128.5%22%20y%3D%2216%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22147.5%22%20y%3D%2216%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22163.5%22%20y%3D%2216%22%3E12%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22174.5%22%20y%3D%2216%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22190.5%22%20y%3D%2216%22%3E220%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22216.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22235.5%22%20y%3D%2216%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22251.5%22%20y%3D%2216%22%3E54%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22262.5%22%20y%3D%2216%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22278.5%22%20y%3D%2216%22%3E710%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2220.5%22%20y%3D%2263%22%3EProfit%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2255.5%22%20y%3D%2263%22%3Efor%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2281.5%22%20y%3D%2263%22%3Ethe%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22111.5%22%20y%3D%2263%22%3Eyear%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22139.5%22%20y%3D%2263%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22188.5%22%20y%3D%2263%22%3EOperating%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22248.5%22%20y%3D%2263%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22280.5%22%20y%3D%2263%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22307.5%22%20y%3D%2263%22%3ETax%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%22110%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%22110%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%22110%22%3E376%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%22110%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%22110%22%3E500%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22105.5%22%20y%3D%22110%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22124.5%22%20y%3D%22110%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22140.5%22%20y%3D%22110%22%3E54%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22151.5%22%20y%3D%22110%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22167.5%22%20y%3D%22110%22%3E710%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%22157%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%22157%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%22157%22%3E321%3C%2Ftext%3E%3Ctext%20font-family%3D%22math164afa8eacc29041f17144b9f42%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%22157%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%22157%22%3E790%3C%2Ftext%3E%3C%2Fsvg%3E) (1)

(1)

Step 4: Calculate retained profit given updated dividends

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2232.5%22%20y%3D%2216%22%3ERetained%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2288.5%22%20y%3D%2216%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22120.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22153.5%22%20y%3D%2216%22%3EProfit%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22188.5%22%20y%3D%2216%22%3Efor%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22214.5%22%20y%3D%2216%22%3Ethe%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22244.5%22%20y%3D%2216%22%3Eyear%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22272.5%22%20y%3D%2216%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22322.5%22%20y%3D%2216%22%3EDividends%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%2263%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%2263%22%3E321%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%2263%22%3E690%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22105.5%22%20y%3D%2263%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22124.5%22%20y%3D%2263%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2263%22%3E220%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22160.5%22%20y%3D%2263%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22176.5%22%20y%3D%2263%22%3E500%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%228.5%22%20y%3D%22110%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2227.5%22%20y%3D%22110%22%3E%26%23xA3%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2247.5%22%20y%3D%22110%22%3E101%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1c3eabe56388c5f9cb7de19517e%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2263.5%22%20y%3D%22110%22%3E%2C%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2279.5%22%20y%3D%22110%22%3E190%3C%2Ftext%3E%3C%2Fsvg%3E) (1)

(1)

Pershore Plumbers Ltd - Updated statement of profit or loss for the year ending 31st March 2025

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?