International Trade (Cambridge (CIE) A Level Business): Revision Note

Exam code: 9609

An introduction to international influences

International trade is the exchange of goods and services across national borders

Exporting is the selling of goods or services from the home country to a customer in another country

E.g. A UK chocolate manufacturer ships bars to supermarkets in Germany

Importing is buying goods or services from producers in another country for use or resale at home

E.g. A Mexican furniture shop sells flat-pack desks manufactured by a producer in Poland

Exports generate extra sales revenue for businesses selling their goods abroad

Imports result in money leaving the country, which generates extra revenue for foreign businesses

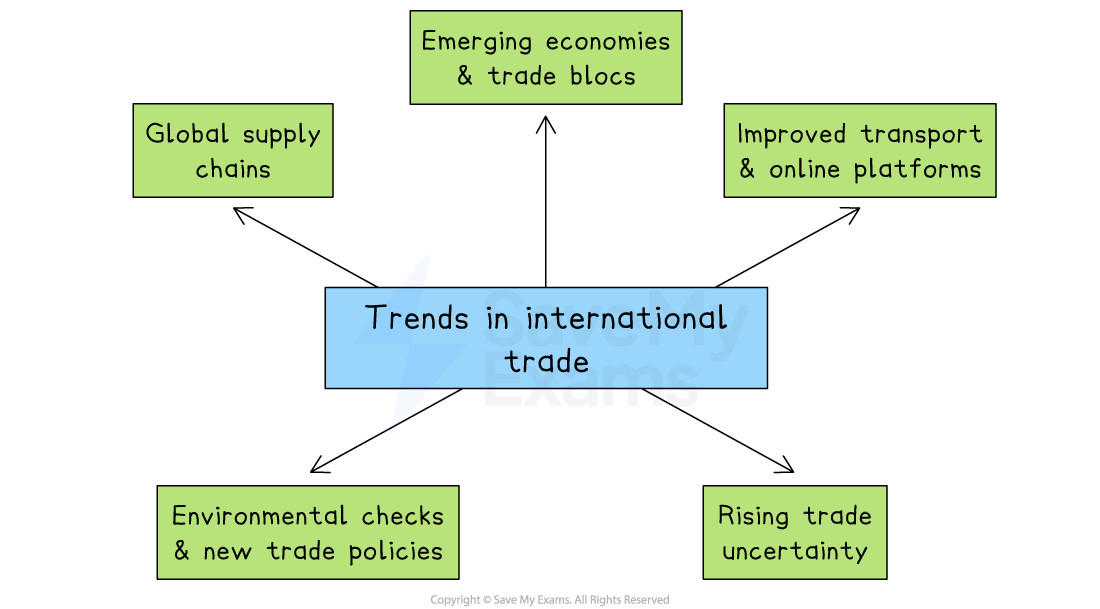

Trends in international trade

Global supply chains and digital services

Many products are made in several countries before they reach the customer.

E.g. A smartphone can be designed in the United States, use chips from Taiwan, be assembled in Vietnam and sold around the world

Emerging economies and trade blocs

China, India and Mexico now produce much of the world’s manufactured goods

Trade blocs like the EU and USMCA lower tariffs for members, but businesses must follow each bloc’s rules

Improved transport and online platforms

Container ships and air freight make international delivery faster and cheaper

Even small firms can sell online to customers in other countries

Environmental checks and new trade policies

Customers and governments examine carbon footprints, working conditions and data security before buying or approving goods

New trade rules encourage firms to adjust their supply chains to meet these higher standards and reduce risk

Rising trade uncertainty

Exchange rates, tariffs and political tensions change more often, making international trade less predictable

E.g. The USA has recently applied high levels of tariffs to a wide range of consumer goods manufactured in China

This encourages firms to develop more flexible supply chains

Benefits of increased international trade

Benefit | Explanation |

|---|---|

Larger customer base |

|

Economies of scale |

|

Lower input costs |

|

Risk spreading |

|

Access to new ideas and technology |

|

The importance of international trade links

International trade links, such as shared markets, digital agreements and transport routes, lower barriers to trade and reduce risk when trading internationally

They can help managers make decisions, including

Where to source supplies

Where to produce

How to distribute goods or services

International trade links and business decisions

International trade link | How it shapes business decisions |

|---|---|

|

|

|

|

|

|

The impact of trade agreements on business

International trade agreements set the ground rules for buying and selling across borders

By lowering tariffs, standardising product rules or protecting foreign investors, these agreements reduce risk and cost for firms

As a result, managers decide where to locate factories, how to price products and which new markets to enter based on the protection and opportunities each agreement offers

Examples of trade agreements

Trade agreement | Example | How it shapes business decisions |

|---|---|---|

Free Trade Agreements (FTAs) |

|

|

Customs unions and common markets |

|

|

Global trade rules |

|

|

The role of technology in international trade

Technology removes many barriers, such as distance, paperwork and payment difficulties, that once limited international trade

Uses of technology in international trade

Technology | Explanation | How it helps firms trade across borders |

|---|---|---|

Mobile payment systems |

|

|

Digital sales platforms |

|

|

Cloud collaboration & digital freight tools |

|

|

Blockchain for trade finance and traceability |

|

|

Artificial Intelligence (AI) applications |

|

|

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?