Syllabus Edition

First teaching 2025

First exams 2027

Factors of Production and Their Rewards (Cambridge (CIE) IGCSE Economics): Revision Note

Exam code: 0455 & 0987

The factors of production

Factors of production are the resources used to produce goods and services

Land, labour, capital and enterprise

The production of any good or service requires the use of a combination of all four factors of production

Goods are physical objects that can be touched (tangible) e.g. mobile phone

Services are actions or activities that one person performs for another (intangible) e.g. manicure, car wash

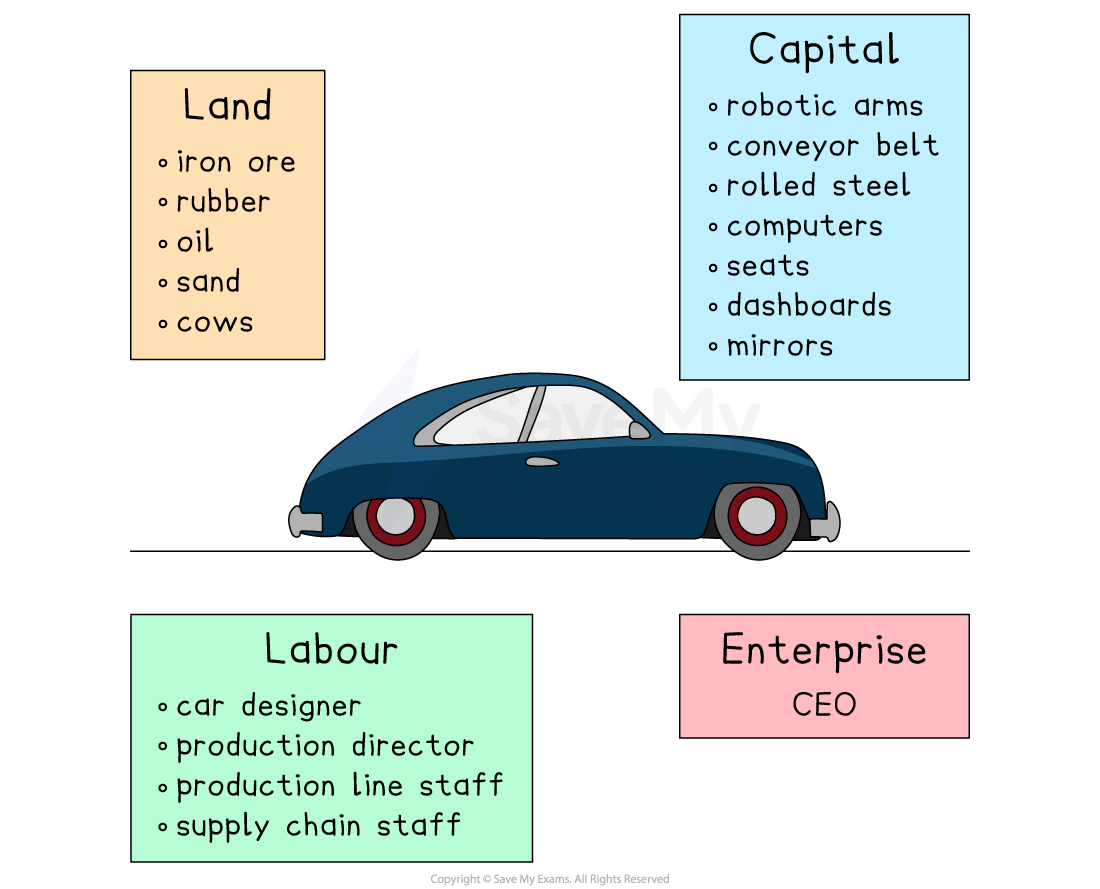

The four factors of production

1. Land

Non man-made natural resources available for production

Some countries have a vast amount of a particular natural resource and so are able to specialise in its production

E.g., oil, wood, fish, corn, iron ore

2. Labour

The human input into the production process

Labour involves mental or physical effort

Not all labour is of the same quality

It can be skilled or unskilled

Some workers are more productive than others because of their education, training and experience

3. Capital

Capital is any man-made resource that is used to produce goods and services

E.g., tools, buildings, machines and computers

4. Enterprise

Enterprise involves taking risks in setting up or running a firm

An entrepreneur decides on the combination of the factors of production necessary to produce good and services with the aim of generating profit

Some of the factors of production required to produce a motor car

Rewards for the factors of production

In a market economic system, the factors of production are privately owned by households or firms (the terms 'market' and 'free market' are used interchangeably)

They make these resources available to firms that use them to produce goods and services

Firms purchase land, labour and capital from households in factor markets

Households receive the following financial rewards for selling their factors of production. This reward is called factor income

The factor income for land → rent

The factor income for labour → wages

The factor income for capital → interest

The factor income for entrepreneurship → profit

Examiner Tips and Tricks

In Paper 1, MCQs frequently require you to apply your understanding of the factors of production by presenting you with a short scenario - and then asking you to identify which factors of production are mentioned in the scenario.

Be careful that you do not identify man-made products as non man-made products, e,g. fertiliser is a capital good (man-made) even though it is an ingredient in the production of many agricultural products

Causes of changes in the quantity and quality of factors of production

If the quantity or quality of a country's factors of production change, then the productive potential of the country also changes

If the quantity or quality increases, this corresponds to an outward shift of the potential output of an economy, as shown on a production possibilities curve model (see Subtopic 1.4.1). The country is able to produce more

If the quantity or quality decreases, this corresponds to an inward shift of the potential output of an economy, as shown on a production possibilities curve model. The country now cannot produce as much as it used to

What changes the quantity and quality?

Factor | Explanation |

|---|---|

Technological advances |

|

Changes in the costs of production |

|

Changes in relative productivity |

|

Changes in education and skills |

|

Changes in government regulations |

|

Demographic changes and migration |

|

Competition policy |

|

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?