Syllabus Edition

First teaching 2025

First exams 2027

Identifying & Classifying Costs (Cambridge (CIE) IGCSE Business): Revision Note

Exam code: 0450, 0986 & 0264, 0774

Introduction to costs

Businesses incur a range of costs

Examples include purchasing raw materials, paying staff salaries and wages and paying utility bills such as electricity

These costs can be classified as follows:

Fixed costs

Variable costs

Total costs

Average costs

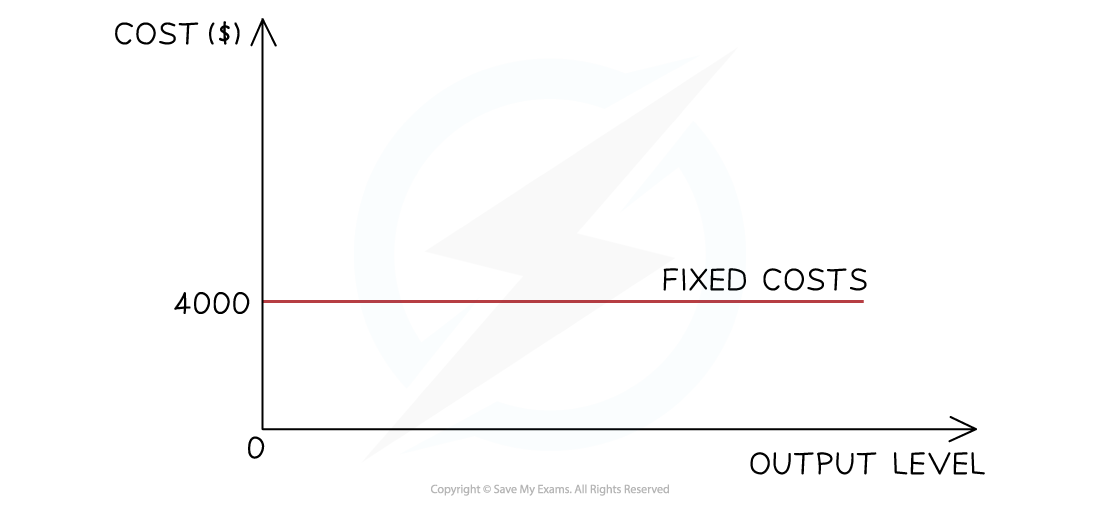

Fixed costs

Fixed costs (FC) are costs that do not change as the level of output changes

These have to be paid whether the output is zero or 5000 units

Examples include rent, management salaries, insurance and bank loan repayments

Fixed costs can be plotted on a graph as a horizontal line

The fixed costs for this firm are $4,000 at all levels of output

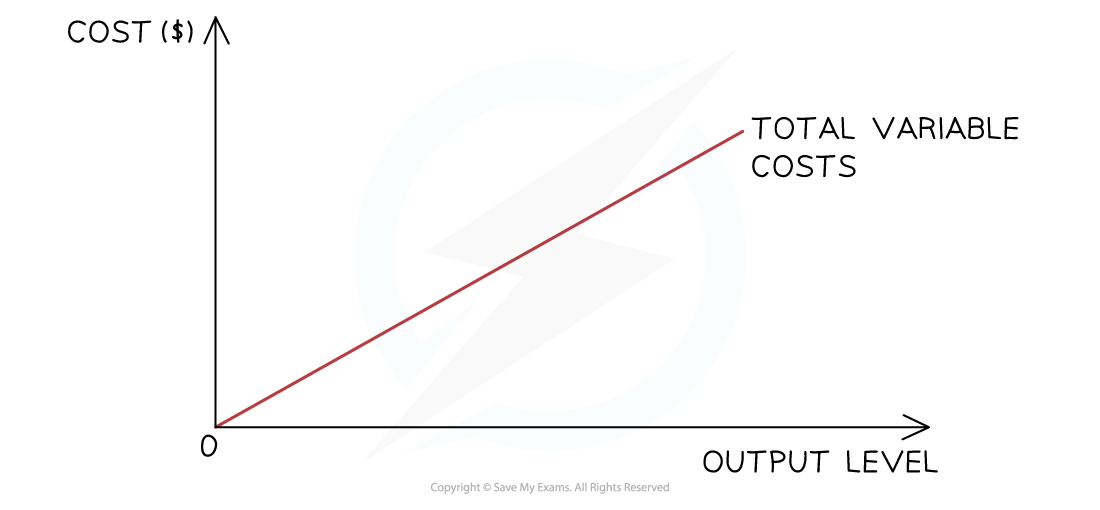

Variable costs

Variable costs (VC) are costs that are directly linked to output

They increase as output increases and vice versa

Examples include raw material costs and wages of workers directly involved in production

Variable costs are plotted on a graph as an upwards sloping line, starting at 0

Total costs

The total cost is the sum of the variable and fixed costs

Total costs are calculated using the formula

![]()

The total costs cannot be 0, as all firms have some level of fixed costs

Total costs are plotted on a graph as an upwards sloping line, parallel to the variable costs, starting at the level of fixed costs

Average costs

The average cost is the typical cost of producing one unit of output

It is sometimes called the unit cost

As a firm grows, it is able to increase its scale of output generating efficiencies that lower its average total costs (AC) of production

These efficiencies are called economies of scale

As a firm continues increasing its scale of output, it will reach a point where its average total costs (AC) start to increase

These inefficiencies are called diseconomies of scale

Examiner Tips and Tricks

Always set out each step when calculating fixed, variable, total and average costs. Even if your final figure is wrong, clear working can earn method marks

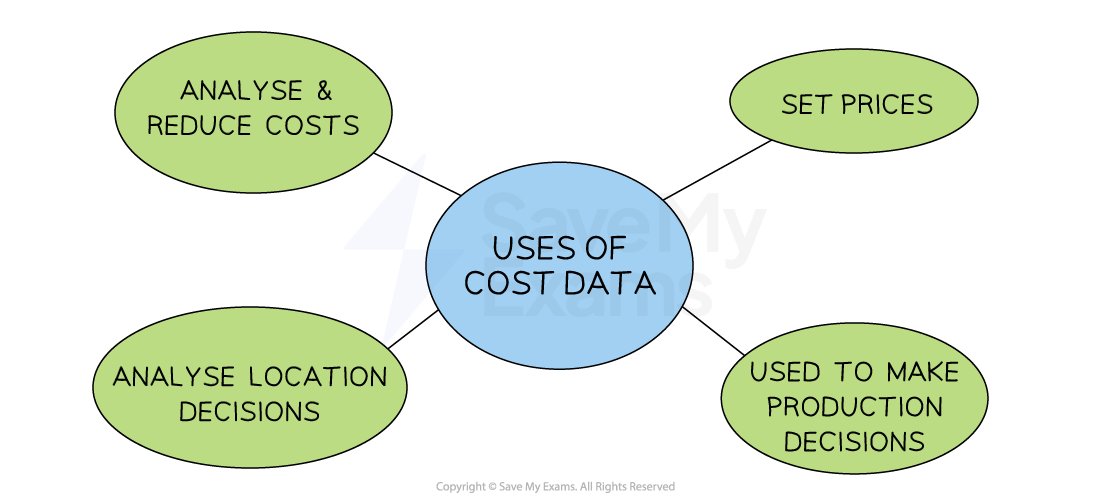

Using cost data to make decisions

Businesses can use cost data to make data-driven business decisions

1. To reduce costs

Accurate cost data helps a business see if costs are too high

Reducing costs is a key way to increase profit

Fixed costs can be reduced by moving to cheaper premises, lowering staff salaries, cutting promotional spending or using cheaper utility suppliers

Variable costs can be lowered by buying cheaper or bulk raw materials, or outsourcing delivery

Businesses must consider how cost-cutting affects customer service, product quality and delivery speed

Paying lower wages may lead to less experienced or skilled staff

Cheaper materials might reduce product quality

2. To set prices

Costs are important when deciding the selling price.

They directly affect how much profit a business makes.

For example, if a cake costs $3 to make and the business wants to make a $1 profit on each cake, it must sell them for $4

3. To make production decisions

If production costs are higher than revenue, the business will make a loss

The business must decide whether to keep or stop making it

This depends on factors including

Whether it’s a new product, with sales likely to rise

Whether fixed costs will need to be paid, even if production stops

4. To make location decisions

Renting or buying premises is a major cost

Some areas are cheaper than others

Businesses must compare these savings to other factors like transport, closeness to customers and available workers

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?