Sources of Finance for Small Businesses (SQA National 5 Business Management): Revision Note

Exam code: X810 75

Introduction to sources of finance

All businesses need finance to get started, allow them to grow, fund capital investments and their continuing activity

Start-up capital

Is the finance needed by a new business to pay for fixed assets and current assets before it can begin trading

A business usually estimates the amount of start-up capital they need in the business plan

Many small new businesses will get a start-up loan to cover these initial costs

Funds for growth

As a business grows more finance may be needed for capital expenditure

It may require more equipment, buildings, IT equipment or vehicles, which will allow the business to increase output

If a business wants to grow by developing a new product, it will need to spend large amounts of capital on research and development (R&D)

Owner's capital

Personal savings are a key source of funds when a business starts up

Owners may introduce their savings or another lump sum, e.g. money received following a redundancy

Owners may invest more as the business grows or if there is a specific need, e.g. a short-term cash flow problem

Taking on a new partner means new owner's capital is introduced into a small business

Evaluating the use of owner's capital

Advantages | Disadvantages |

|---|---|

|

|

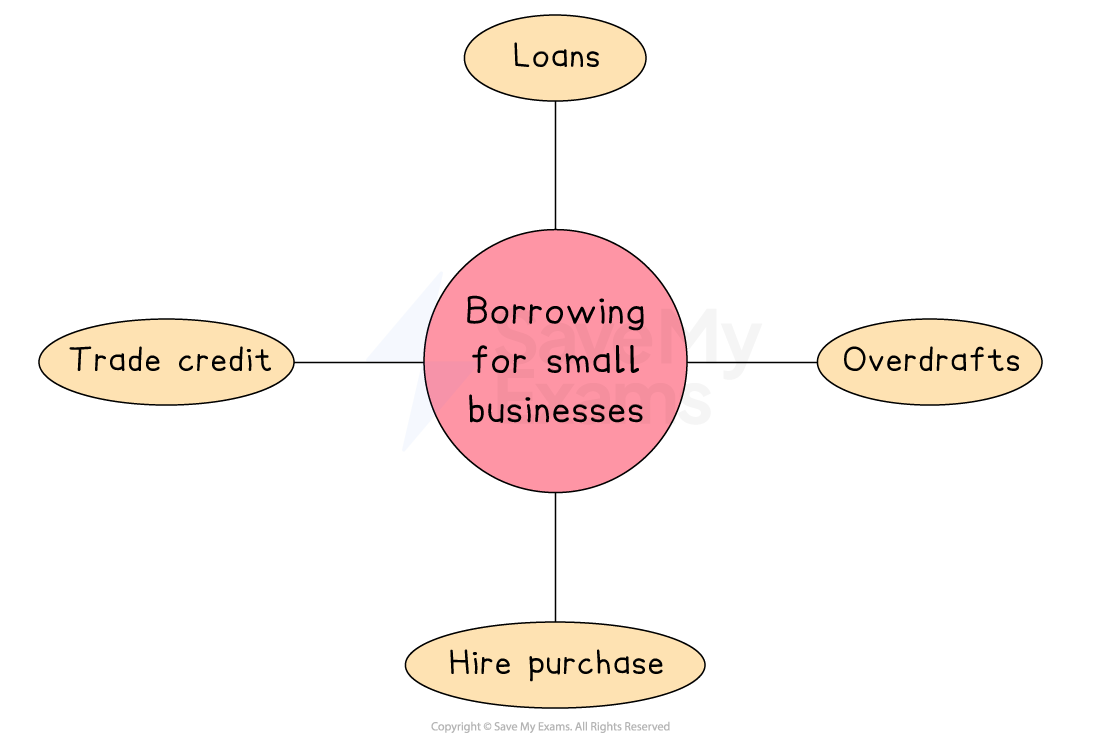

Where do small businesses secure finance from?

Many small businesses rely on short-term borrowing methods that operate internally within their banking arrangements, such as overdrafts or loans secured against business assets

1. Bank overdraft

An overdraft allows a business to withdraw more money than is in its account, up to an agreed limit

Advantages | Disadvantages |

|---|---|

|

|

2. Bank loan

A bank loan provides a fixed amount of money that is repaid with interest over a set period

Advantages | Disadvantages |

|---|---|

|

|

3. Trade credit

Trade credit is when suppliers allow a business to buy goods now and pay later, usually within 30–60 days

Advantages | Disadvantages |

|---|---|

Helps improve short-term cash flow. | Missed payments may damage supplier relationships. |

No interest if paid within the agreed period. | May lose early payment discounts. |

Allows businesses to sell goods before payment is due. | Usually only available to trusted or established firms. |

4. Hire purchase

Hire purchase allows a business to buy an asset and pay for it over time, while using it immediately

Advantages | Disadvantages |

|---|---|

|

|

Examiner Tips and Tricks

Students often overlook why small businesses struggle to raise funds. Banks may see them as risky; they lack collateral, and investors prefer larger firms. Examiners reward answers that explain these barriers rather than simply listing unavailable finance options

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?