Profit Statements (Cambridge (CIE) AS Accounting): Revision Note

Exam code: 9706

Profit statements using absorption costing

What are profit statements?

Profit statements show the profit or loss made from selling a product/service

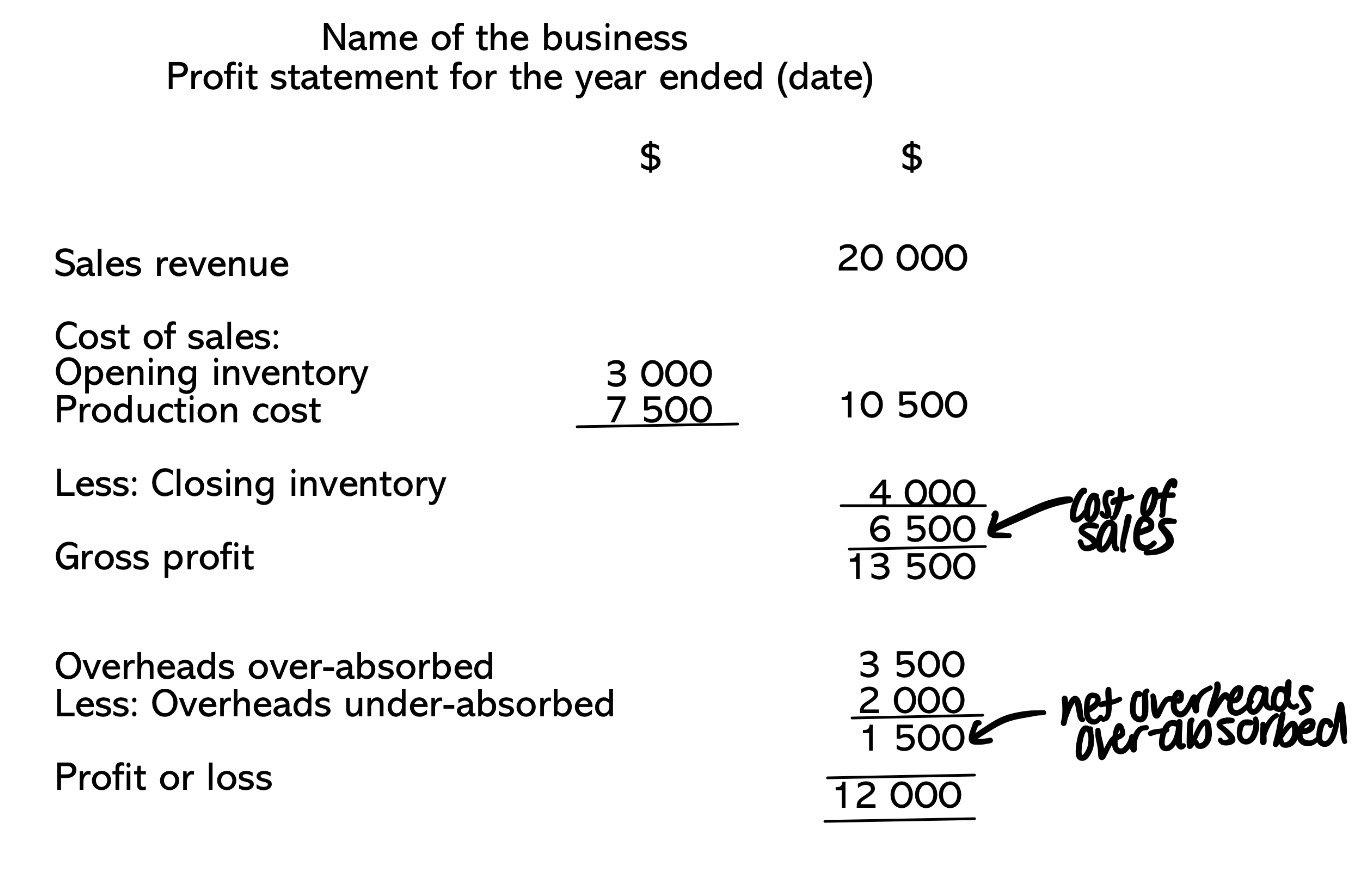

How do I prepare a profit statement using absorption costing?

STEP 1

Calculate the sales revenue

Selling price per unit × number of units sold

STEP 2

Calculate the cost of sales

Start with opening inventory

Add production cost

Including the fixed costs

Subtract closing inventory

STEP 3

Calculate the gross profitSales revenue - cost of sales

STEP 4

Adjust for the under-absorption or over-absorption to find the profit or lossAdd overheads over-absorbed

Subtract overheads under-absorbed

STEP 5

Subtract any other non-production costs to calculate the profit or loss

Worked Example

Jane manufactures a single product. She uses a system of absorption costing.

The following budgeted data is available for one unit of the product.

$ | |

|---|---|

Selling price | 14 |

Direct materials | 4 |

Direct labour | 3 |

Budgeted production: 20 000 units per month

Budgeted fixed overheads: $23 000 per month

On 1 August, Jane held 2 000 units.

The following actual results are available.

Sales: 12 000 units

Production: 18 000 units

Fixed overheads: $25 000

Prepare the profit statement for the month of August to calculate the profit or loss.

Answer:

Sales revenue

$14 × 12 000 = $168 000

Production cost

Direct materials

$4 × 18 000 = $72 000

Direct labour

$3 × 18 000 = $54 000

Fixed overheads

25 000 ÷ 20 000 = $1.25 per unit

$1.25 × 18 000 = $22 500

Total

$72 000 + $54 000 + $22 500 = $148 500

Opening inventory

($4 + $3 + $1.25) × 2 000 = $16 500

Closing inventory

Opening inventory + Production - Sales

= 2 000 + 18 000 - 12 000

= 8 000 units

($4 + $3 + $1.25) × 8 000 = $66 000

Calculate the overheads that are over-absorbed or under-absorbed

Actual overheads - Overheads absorbed

25 000 - 22 500 = 2 500 under-absorbed

Profit statement for the month of August

$ | ||

|---|---|---|

Revenue | 168 000 | |

Cost of sales: | ||

Opening inventory | 16 500 | |

Production costs | 148 500 | |

Less: Closing inventory | (66 000) | (99 000) |

Gross profit | 69 000 | |

Less: Overheads under-absorbed | (2 500) | |

Profit for the month | 66 500 |

Profit for August is $66 500

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?