Zoo

Sue is managing director and the sole owner of Zoo Ltd, a luxury fashion handbag business. Sue has helped the company to grow over the last forty years, taking responsibility for the key decisions for the business as a whole. She does, however, think carefully about the design of her employees’ jobs. She delegates many tasks to her team in areas such as marketing and operations and is good at praising her employees for their achievements. Zoo sells through independent fashion retailers in the UK. The average price of its handbags to all UK retailers is £250.

Last year Sue’s son Mike joined the business. Sue wants him to take over the company in the future. Mike had just finished his business degree at university and is eager to prove himself. Mike wants to increase the annual profits of the business by at least 60% in the next few years and make returns on all future investments of at least 25%. Until now, sales of the business have typically grown by 2% a year.

Mike has been negotiating on his own to win a contract with a very large fashion retailer, Nexia, to sell Zoo handbags. Nexia has stores in the UK and throughout Europe. Nexia has told Mike that it refuses to discuss the contract further unless Zoo has the ability to produce on a much larger scale.

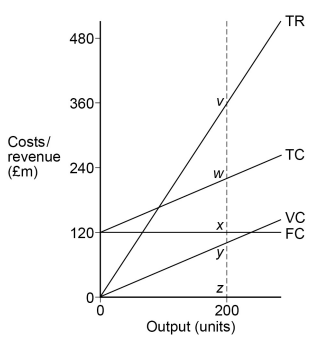

For Zoo this means it would need to invest £1 500 000 in new production capacity. This would increase fixed costs by £160 000 a year but would not affect its variable costs per unit.

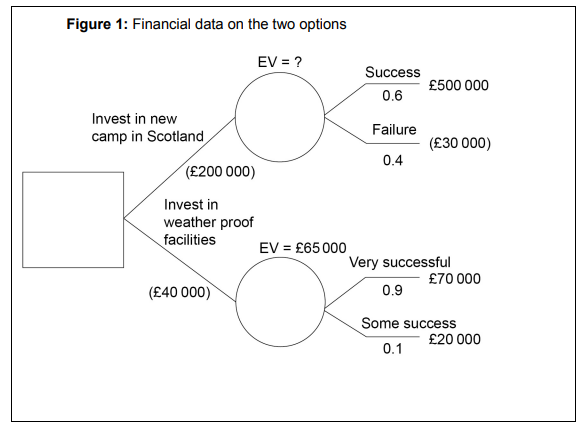

Mike has told Sue that there is an 80% chance that the contract will go ahead if Zoo invests in more capacity. The decision whether to invest in more capacity remains with Sue.

The bags for Nexia will be produced in addition to its current output. If Nexia is happy with sales in the first few years, bigger contracts may follow.

Appendix A: The terms of the potential contract

Appendix B: Other Zoo production and finance data

Current output of Zoo: 12 000 bags a year

Variable costs of producing a Zoo bag: £130

Current annual fixed costs: £660 000

Appendix C: Zoo human resource performance data 2017–2018