Statement of Changes in Equity (Cambridge (CIE) AS Accounting): Revision Note

Exam code: 9706

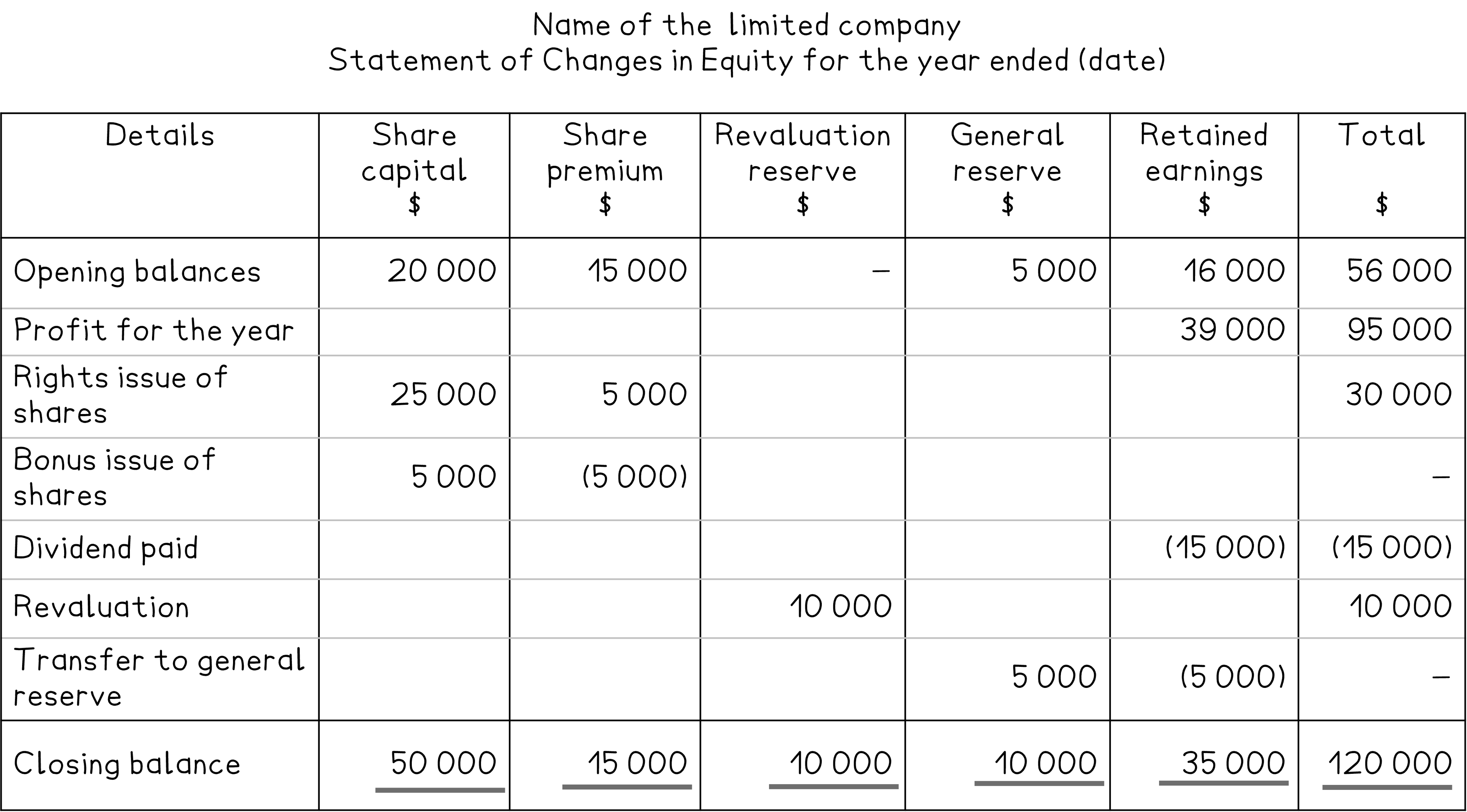

Statements of changes in equity

What is a statement of changes in equity?

A statement of changes in equity is a statement showing how the equity of a limited company has changed over a year

It shows the changes to:

The share capital

The share premium

The revaluation reserve

The retained earnings

The general reserve

It shows how the profits are used

Some of the profits will be distributed to the shareholders as dividends

The remaining profits are carried forward to the next financial year as retained earnings

Some of the retained earnings might be transferred to the general reserve

What are the reasons for the changes in the value of the total equity?

The equity of the limited company is likely to change due to the following

The profit for the year is added to the retained earnings

The profit is distributed or paid to shareholders in the form of interim and final dividends

Some of the profit for the year is transferred to the general reserve

How are dividends treated on the statement of changes in equity?

Shareholders get a share or portion of the profits as dividends

The statement of changes in equity shows the dividends paid to shareholders during the year for any ordinary shares

Dividends that are paid halfway through the year are known as interim dividends

Dividends that are paid at the end of the year are known as final dividends

Dividends proposed by the directors to be paid are not to be included in the statement of changes in equity until the amount is paid

How are rights issues and bonus issues treated on the statement of changes in equity?

A rights issue increases the total equity

Increase the share capital and share premium

The total equity increases

A bonus issue does not change the total equity

Increase the share capital

Decrease the share premium before other reserves

Do not use the revaluation reserve

Worked Example

On 1 April 2023, P and Q Limited supplied the following information:

In total, there were 800 000 ordinary shares of $0.75 each

The balance of the share premium was $100 000

The balance of the general reserve was $62 000

The retained earnings amounted to $55 000

On 31 March 2024, P and Q Limited supplied the following information:

The profit for the year ended 31 March 2024 was $70 000

On 1 January 2024, an interim dividend of $32 000 was paid

On 1 February 2024, a bonus issue of shares was made of one ordinary shares for every eight shares held

Reserves were maintained in their most flexible formOn 31 March 2024, $12 000 was transferred from the retained earnings to the general reserve

On 31 March 2024, the directors proposed the payment of an ordinary share dividend of 10%

Prepare the statement of changes in equity for the year ended 31 March 2024 for P and Q Limited.

Answer:

Identify the key information given on 1 April 2023

In total, there were 800 000 ordinary shares of $0.75 each

Calculate the ordinary share capital on 1 April 2023 by multiplying the number of shares by the price of a share

Ordinary share capital: 800 000 × $0.75 = $600 000

The balance of the share premium was $100 000

This is the opening balance on the statement of changes in equity

The balance of the general reserve was $62 000

This is the opening balance on the statement of changes in equity

The retained earnings amounted to $55 000

This is the opening balance on the statement of changes in equity

Identify the key information given on 31 March 2024

The profit from operations for the year ended 31 March 2024 was $90 000

This is before the finance costs are subtracted

On 1 January 2024, an interim dividend of $32 000 for the ordinary shares was paid

This will decrease the retained earnings

The interim dividend was paid in the current year so it is entered on the statement of changes in equity

On 1 February 2024, a bonus issue of shares was made of one ordinary shares for every eight shares held

Reserves were maintained in their most flexible form800 000 ÷ 100 000 new shares issues

100 000 × $0.75 = $75 000 increase in share capital

Decrease the hare premium

On 31 March 2024, $12 000 was transferred from the retained earnings to the general reserve

This will decrease the retained earnings but increase the general reserve

On 31 March 2024, the directors proposed the payment of an ordinary share dividend of 10%

Any proposed dividend at the end of the year that remains unpaid, should not be included on the statement of changes in equity

Complete the statement of changes in equity using the required format

Remember to total up rows and columns

Put brackets around values if they are to be subtracted.

P and Q Limited Statement of Changes in Equity for the year ended 31 March 2024 | |||||

Share capital $ | Share premium $ | General Reserve $ | Retained Earnings $ | Total $ | |

On 1 April 2023 | 600 000 | 100 000 | 62 000 | 55 000 | 817 000 |

Profit for the year | 70 000 | 70 000 | |||

Dividend paid | (32 000) | (32 000) | |||

Bonus issue | 75 000 | (75 000) | - | ||

Transfer to general reserve | 12 000 | (12 000) | - | ||

On 31 March 2024 | 600 000 | 25 000 | 74 000 | 81 000 | 855 000 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?