The Accounting Process (Cambridge (CIE) AS Accounting): Revision Note

Exam code: 9706

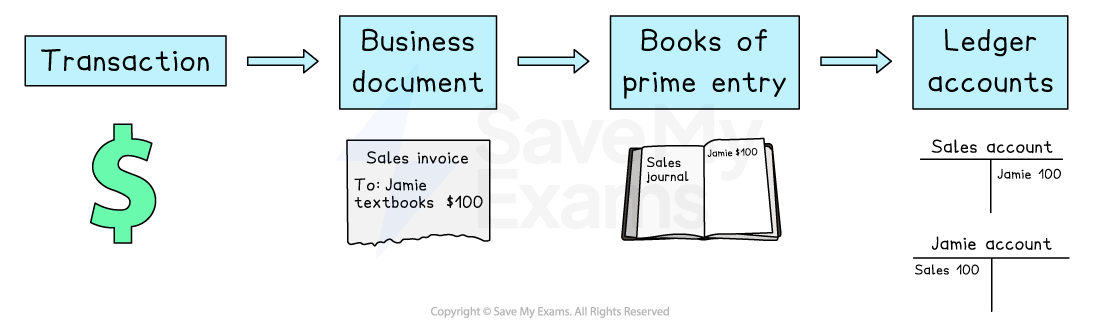

The accounting process

What is the accounting process?

Stage 1: Transaction

A transaction takes place

Examples include:

The sale or purchase of goods, a service or an asset

Withdrawing or depositing cash

Paying an expense or receiving income

Stage 2: Business document

A business document is issued or received

This is a record of the transaction

Stage 3: Book of prime entry

The amount is entered into a book of prime entry

This collates the different types of transactions

Stage 4: Ledger account

The entries from the books of prime entry are entered into the ledger accounts

These are part of the double-entry accounting system

Examiner Tips and Tricks

The aim of the accounting process is to have the information in the ledger accounts so that financial statements can be produced at the end of the accounting period.

Financial statements

What are financial statements?

Financial statements are produced each year

They show a summary of the business activity during the year

The financial statements that most businesses produce are:

statement of profit or loss

statement of financial position

What is a statement of profit or loss?

An accountant prepares a statement of profit or loss for a business to measure the profit or a loss

The profit or loss is the difference between the total income and the total expenses

A profit is made if the income is higher than the expenses

A loss is made if the income is lower than the expenses

It can also show the gross profit for a trading business

This is the profit from trading activities

Gross profit = revenue - cost of sales

It is important to produce a statement of profit or loss to measure the performance and profitability of a business

It can be used to monitor the progress of the business

If a profit is made, the owner is making money on their investment

If a loss is made, the owner might have to make changes to the business

What is a statement of financial position?

An accountant prepares a statement of financial position to show the current values of the

assets

liabilities

capital or equity

It can be used to calculate the working capital

This is the amount of money a business would have left if it converted all of its current assets into cash and paid off its current liabilities

Working capital = current assets - current liabilities

It is important to produce a statement of financial position to measure the liquidity of a business

It can be used to make decisions about the business

If there is a lot of cash, then the business might decide to purchase more non-current assets

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?