Syllabus Edition

First teaching 2025

First exams 2027

Allowance for Irrecoverable Debts (Cambridge (CIE) IGCSE Accounting): Revision Note

Exam code: 0452 & 0985

Allowance for irrecoverable debts

What is an allowance for irrecoverable debts?

An allowance for irrecoverable debts is an estimation for the amount of sales in a given financial period which will result in irrecoverable debts

The amount for the allowance for irrecoverable debts can be determined using different methods

It could be a fixed percentage of the trade receivables at the end of a financial period

It could be a fixed amount based on data from previous years

It could factor in how long debts have been outstanding

It could be based on which individuals are unlikely to settle their debts

A business should use the same method for accounting for the allowance each year

This adheres to the accounting principle of consistency

An allowance for irrecoverable debts is similar to a provision for depreciation of a non-current asset

The allowance for irrecoverable debts estimates a reduction in an asset

The asset is the amount owed by trade receivables

However, the reduction is kept in an allowance account which is separate from the asset accounts

Why do businesses set up allowance for irrecoverable debts?

Businesses use an allowance for irrecoverable debts to adhere to the accounting principles:

Prudence

Matching

The principle of prudence is applied because:

The assets are not overstated

The allowance reduces the trade receivables by a realistic amount

The profit for the year is not overstated

The potential losses are factored into the expenses

The principle of matching is applied because:

An estimate of irrecoverable debts is made based on sales in a given period

This estimate is then treated as an expense for the same period as the original sales

How do I set up an allowance for irrecoverable debts?

The allowance is set up at the end of the financial period

The business estimates the amount of sales in that period that will result in irrecoverable debts

This is normally a percentage of the trade receivables at the end of the financial period

This amount is debited to the statement of profit or loss as an expense

A credit entry is made in the allowance for irrecoverable debts account

The balance of an allowance for irrecoverable debts account will be on the credit side because it represents a reduction in an asset

Examiner Tips and Tricks

No entries are made in any account in the sales ledger for the allowance for irrecoverable debts. Entries are made in these accounts when debts are actually written off.

Worked Example

On 31 March 2024, Josef is owed $42 000 by credit customers. Josef decides to create an allowance for irrecoverable debts, set at 5% of trade receivables.

Prepare journal entries for the creation of an allowance for irrecoverable debts account on 31 March 2024. A narrative is not required.

Journal

Date | Details | Debit $ | Credit $ |

Answer:

Calculate the allowance for irrecoverable debts

5% × $42 000 = $2 100

Start with the account to be debited

The statement of profit or loss

Then include the account to be credited

The allowance for irrecoverable debts account

Journal

Date | Details | Debit $ | Credit $ |

2024 Mar 31 | Statement of profit or loss | 2 100 | |

Allowance for irrecoverable debts | 2 100 |

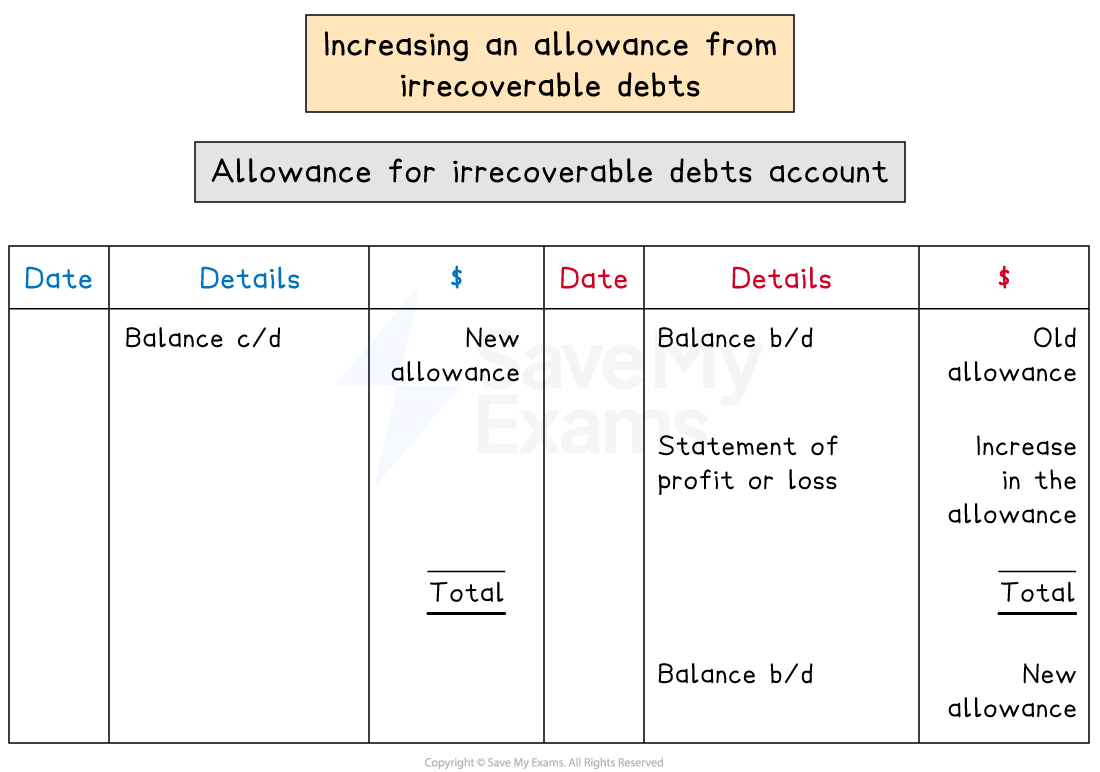

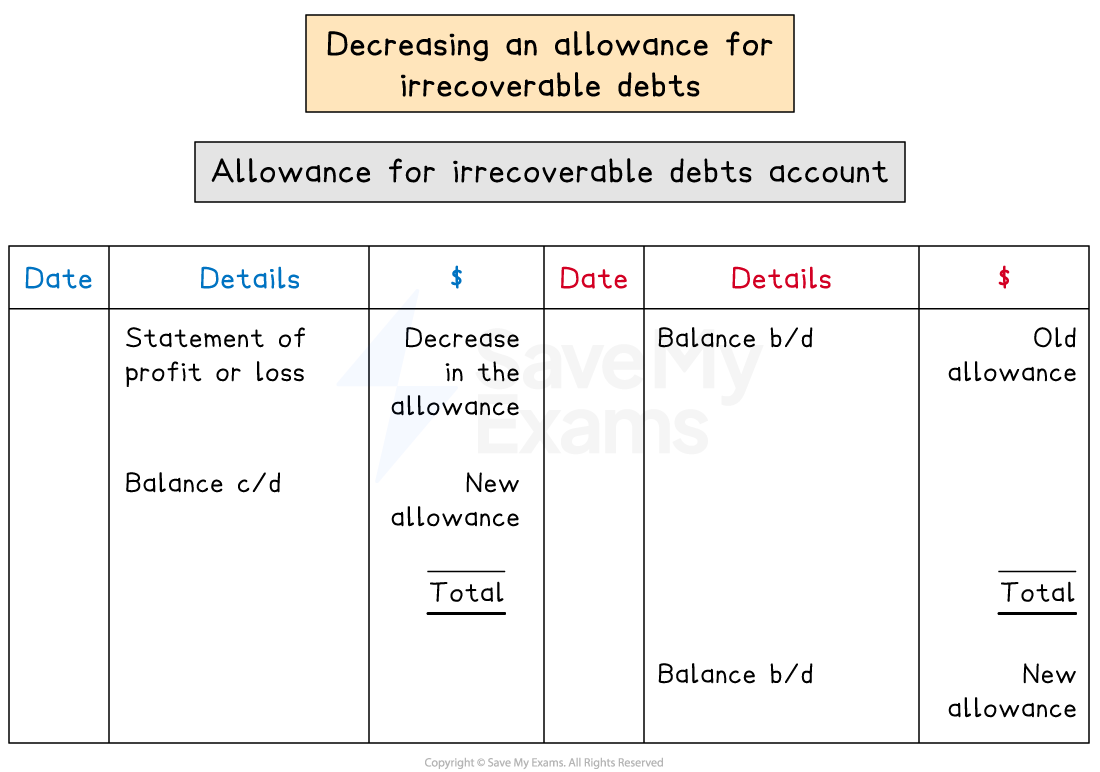

Adjustments to an allowance for irrecoverable debts

How do I update an allowance for irrecoverable debts at the end of a financial period?

The allowance for irrecoverable debts is reviewed at the end of each year and the amount might be updated

At the end of the financial period

Calculate the new allowance for irrecoverable debts

This will be the opening balance of the allowance for irrecoverable debts account for the next financial period

Enter it on the credit side

Enter the corresponding closing balance on the debit side of the allowance for irrecoverable debts account for the current financial period

Calculate the difference and enter it on the appropriate side to make the account balance

This value will be transferred to the statement of profit or loss

If the allowance for irrecoverable debts increases:

The difference will be on the credit side

This will be debited to the statement of profit or loss as an expense

If the allowance for irrecoverable debts decreases:

The difference will be on the debit side

This will be credited to the statement of profit or loss as an income

How does an allowance for irrecoverable debts affect the financial statements?

At the end of a financial period, the balance from the allowance for irrecoverable debts account appears on the statement of financial position

It is listed under trade receivables

The balance is subtracted from the balance for trade receivables

The difference in the allowance between the start of the year and the end of the year appears on the statement of profit or loss

If the allowance has increased, it appears with the other expenses

If the allowance has decreased, it appears with the other income

Examiner Tips and Tricks

When an allowance for irrecoverable debts is first created, the whole amount is charged as an expense to the statement of profit or loss, this is because the allowance has increased from $0.

Worked Example

Ricardo keeps an allowance for irrecoverable debts at a rate of 3% of trade receivables. On 1 March 2023, the balance of the allowance for irrecoverable debts was $1 530. On 29 February 2024, the trade receivables were $49 500, of which $1 000 should be written off as irrecoverable debts.

(a) Prepare the allowance for irrecoverable debts account for Ricardo. Balance the account on 29 February 2024 and bring down the balance on 1 March 2024.

(b) State how the allowance for irrecoverable debts affects the profit for the year ended 29 February 2024.

Answer:

Subtract the irrecoverable debts from the trade receivables

$49 500 - $1 000 = $48 500

Calculate the new allowance for irrecoverable debts

3% × $48 500 = 1 455

Calculate the change in the allowance

$1 530 - $1 455 = $75

(a)

Enter the details into the allowance for irrecoverable debts account

Remember, the balance b/d is on the credit side

Ricardo

Allowance for Irrecoverable Debts Account

Date | Details | $ | Date | Details | $ |

2024 Feb 29 |

Statement of profit or loss |

75 | 2023 Mar 1 |

Balance b/d |

1 530 |

Feb 29 | Balance c/d | 1 455 |

| ||

1 530 | 1 530 | ||||

2024 Feb 29 |

Balance b/d |

1 455 |

(b)

The allowance for irrecoverable debts has decreased. This will be credited to the statement of profit or loss and treated as an income.

The allowance for irrecoverable debts increases the profit for the year by $75

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?