Life Memberships & Donations (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

Life memberships

What are life memberships?

A life membership is where a member makes a one-off payment to become a member for life

The member no longer needs to pay the annual subscription fee

Entry fees are similar to life memberships as they are one-off payments

What is the accounting treatment for life memberships?

The full amount received from life memberships does not contribute to that year's surplus calculated in the income and expenditure account

This complies with the accounting concepts

Prudence

Taking the full amount as income in the year received would overstate that year's income

Accruals

The club provides services to life members over many years

The correct accounting treatment is for a proportion of the amount received from life memberships to contribute to income for a specified number of years

The remaining balance of the life membership fund is a non-current liability

It is similar to income received in advance

Except, the income is received years in advance

Examiner Tips and Tricks

The exam question will tell you what percentage is used for yearly income and for how many years.

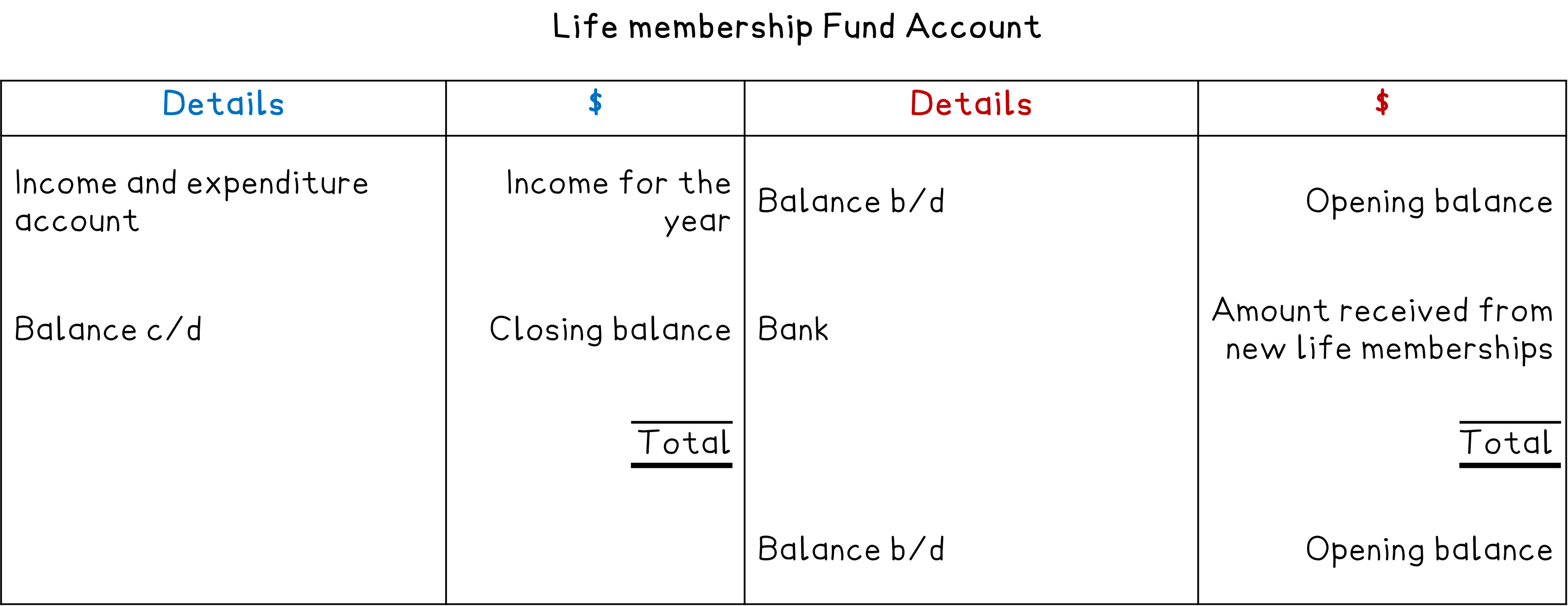

What are the journal entries for life memberships?

When the club receives payment for a life membership

Enter the full amount into the accounts

Debit the bank account

Credit the life membership fund account

At the end of the financial year

Enter the specified proportion of the life membership fund as income

Debit the life membership fund account

Credit the income and expenditure account

Examiner Tips and Tricks

The annual amount of the life membership fund that is released as income is not normally apportioned based on when the member joined. In general, the amount is based on the number of life membership holders at the end of the year. Therefore, it is important to include the number of life memberships purchased during the year.

Worked Example

The TS Club is a club providing tennis facilities to its members. The club admits life members as well as ordinary members.

The life membership fund on 1 June 2024 amounted to $10 350.

The total receipts of the club for the year were as follows:

$ | |

|---|---|

Subscriptions from ordinary members | 31 500 |

Life membership fees | 6 000 |

On 31 May 2024 the club had 10 life members, all of whom had joined after 31 May 2020. 4 new members took out life membership during the year. The life membership fee is to be transferred to income over ten years in equal amounts.

Calculate the balance on the life membership fund after the transfer to the income and expenditure account on 31 May 2025.

Answer:

Calculate the amount received from each life membership

$6 000 ÷ 4 members = $1 500 per member

Calculate the annual income from a life membership

$1 500 ÷ 10 years = $150 per year

Calculate the total number of members at 31 May 2025

10 + 4 = 14

Calculate the balance on the life membership fund

$ | ||

|---|---|---|

Balance on 1 June 2024 | 10 350 | |

New life memberships | 6 000 | |

Income from life memberships | $150 × 14 | (2 100) |

Balance on 31 May 2025 | 14 250 |

$14 250

Donations

What are donations?

Donations are given to clubs and societies from members, other businesses and the government

The table describes the different types of donations:

Type of donation | Description |

|---|---|

General donation |

|

Restricted donation |

|

Grants covering multiple years |

|

What is the accounting treatment for donations?

The accounting treatment is very similar to life memberships

For a general donation

The full amount is included in the income and expenditure account

For a restricted donation

Amounts are only included in the income and expenditure account when they are used

Parts of the donation might be used each year over several years

The remaining balance of the donation is a current or non-current liability

For a grant covering multiple years

An amount of the grant that is proportional to the year is included in the income and expenditure account

For example, if a grant of $3 000 is given at the start of the year and is intended to last for 3 years, then $1 000 is included as income for the year

The remaining balance of the grant is a current or non-current liability

Examiner Tips and Tricks

The remaining balance of a restricted donation or grant is often called deferred income in exam questions.

What are the journal entries for donations?

General donations

When the club receives the donation

Enter the full amount into the accounts

Debit the bank account

Credit the donations account

At the end of the financial year

Enter the full amount of the general donations

Debit the donations account

Credit the income and expenditure account

Grants covering multiple years

When the club receives the grant

Enter the full amount into the accounts

Debit the bank account

Credit the donations account

At the end of the financial year

Enter the proportion relating to the current year

Debit the donations account

Credit the income and expenditure account

Restricted donations

When the club receives the donation for a specific purpose

Open a new bank account for the amount and create a trust fund in the books of account

Enter the full amount

Debit the special bank account

Credit the trust fund account

When money is used from the trust fund to cover the cost of an activity

Enter the specific amount paid into the accounts

Debit the relevant account

E.g. non-current asset

Credit the special bank account

At the end of the financial year

Enter the total amount used from the trust fund that year into the accounts

Debit the trust fund account

Credit the income and expenditure account

Worked Example

The TS Club is a club providing tennis facilities to its members.

The TS Club receives grants and donations which may cover several years.

At 1 June 2024, TS Club had a liability for deferred income from grants and donations amounting to $3 400.

During the year ending 31 May 2025, TS Club received grants and donations totalling $5 200.

The amount $4 400 was posted to the income and expenditure account on 31 May 2025 for grants and donations.

Calculate the total of deferred income after the transfer to the income and expenditure account on 31 May 2025.

Answer:

$ | |

|---|---|

Balance on 1 June 2024 | 3 400 |

New grants and donations | 5 200 |

Income from grants and donations | (4 400) |

Balance on 31 May 2025 | 4 200 |

$4 200

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?