Factory Profit & Unrealised Profit (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

Factory profit

What is factory profit?

Factory profit is an additional amount added to the cost of production before the finished goods are transferred to the statement of profit or loss

Factory profit is also called manufacturing profit

It is usually expressed as a percentage mark-up on the cost of production

Why might businesses account for factory profit?

Businesses apply a rate of factory profit so that they can compare the transfer value with the sale prices of the same goods offered by competitors

This is known as benchmarking

The managers can then decide whether to continue to produce the goods or purchase them from a supplier

The manufacturing department can be treated as a separate profit centre and its performance can be evaluated

Targets can be set for the factory profit

What is the accounting treatment for factory profit?

The factory profit is calculated

Multiply the cost of production by the rate of factory profit

Add the factory profit to the cost of production to give the transfer value in the manufacturing account

This is a debit entry to the manufacturing account

The transfer value is then used to calculate the cost of sales and then the gross profit

The factory profit is then added to the gross profit

This essentially eliminates the factory profit from the transfer value

This ensures that the factory profit does not lower the profit for the year

This is a credit entry to the statement of profit or loss

Worked Example

P Limited is a manufacturing business. It applies a rate of factory profit of 20%.

At 1 January 2025, the finished goods inventory at transfer value was $28 800.

The cost of production for the goods produced during the year ended 31 December 2025 was $314 000.

At 31 December 2025, the finished goods at transfer value was $21 600.

Find the transfer value of the goods produced for the year ended 31 December 2025.

Answer:

Multiply the cost of production by the rate of factory profit to find the factory profit

20% × $314 000 = $62 800

Add this to the cost to find the transfer value

$314 000 + $62 800 = $376 800

Unrealised profit

What is unrealised profit?

Unrealised profit is the amount of the factory profit that is included in the valuation of closing inventory of the manufactured goods

Goods are transferred to the statement of profit or loss using the transfer value which includes the factory profit

This profit has not been earned for the goods that remain unsold at the end of the year

What is a provision for unrealised profit?

A provision for unrealised profit is used to show the true valuation of the inventory held at the end of the year

It is very similar to an allowance for irrecoverable debts

It complies with the prudence concept by ensuring that the assets are not overstated

The balance on the provision for unrealised profit account is the amount of valuation of the closing finished goods that arises due to the rate of factory profit

How do I calculate the balance of the provision for unrealised profit?

Use the formula

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Cline%20stroke%3D%22%23000000%22%20stroke-linecap%3D%22square%22%20stroke-width%3D%221%22%20x1%3D%222.5%22%20x2%3D%22182.5%22%20y1%3D%2223.5%22%20y2%3D%2223.5%22%2F%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2262.5%22%20y%3D%2216%22%3EFactory%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22114.5%22%20y%3D%2216%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22142.5%22%20y%3D%2216%22%3E%25%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2217.5%22%20y%3D%2241%22%3E100%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2239.5%22%20y%3D%2241%22%3E%25%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1b1c7f48efedbe049bdfa534d0f%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2256.5%22%20y%3D%2241%22%3E%2B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2292.5%22%20y%3D%2241%22%3EFactory%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2241%22%3Eprofit%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22172.5%22%20y%3D%2241%22%3E%25%3C%2Ftext%3E%3Ctext%20font-family%3D%22math1b1c7f48efedbe049bdfa534d0f%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22193.5%22%20y%3D%2230%22%3E%26%23xD7%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22232.5%22%20y%3D%2230%22%3ETransfer%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22286.5%22%20y%3D%2230%22%3Evalue%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22317.5%22%20y%3D%2230%22%3Eof%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22340.5%22%20y%3D%2230%22%3Ethe%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22381.5%22%20y%3D%2230%22%3Eclosing%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22440.5%22%20y%3D%2230%22%3Efinished%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22494.5%22%20y%3D%2230%22%3Egoods%3C%2Ftext%3E%3C%2Fsvg%3E)

For example, suppose the rate of factory profit is 25% mark-up on cost and finished goods at transfer value is $20 000

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Cline%20stroke%3D%22%23000000%22%20stroke-linecap%3D%22square%22%20stroke-width%3D%221%22%20x1%3D%222.5%22%20x2%3D%2232.5%22%20y1%3D%2223.5%22%20y2%3D%2223.5%22%2F%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2218.5%22%20y%3D%2216%22%3E25%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2217.5%22%20y%3D%2241%22%3E125%3C%2Ftext%3E%3Ctext%20font-family%3D%22math13d2dc549f508103e95d72be633%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2243.5%22%20y%3D%2230%22%3E%26%23xD7%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2258.5%22%20y%3D%2230%22%3E%24%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2274.5%22%20y%3D%2230%22%3E20%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22100.5%22%20y%3D%2230%22%3E000%3C%2Ftext%3E%3Ctext%20font-family%3D%22math13d2dc549f508103e95d72be633%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22122.5%22%20y%3D%2230%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22137.5%22%20y%3D%2230%22%3E%24%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22148.5%22%20y%3D%2230%22%3E4%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22170.5%22%20y%3D%2230%22%3E000%3C%2Ftext%3E%3C%2Fsvg%3E)

The fractional part of the formula is the factory profit margin

In the example above, the factory profit margin is

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Cline%20stroke%3D%22%23000000%22%20stroke-linecap%3D%22square%22%20stroke-width%3D%221%22%20x1%3D%222.5%22%20x2%3D%2232.5%22%20y1%3D%2223.5%22%20y2%3D%2223.5%22%2F%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2218.5%22%20y%3D%2216%22%3E25%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2217.5%22%20y%3D%2241%22%3E125%3C%2Ftext%3E%3Ctext%20font-family%3D%22math13d2dc549f508103e95d72be633%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2243.5%22%20y%3D%2230%22%3E%26%23xD7%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2265.5%22%20y%3D%2230%22%3E100%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2287.5%22%20y%3D%2230%22%3E%25%3C%2Ftext%3E%3Ctext%20font-family%3D%22math13d2dc549f508103e95d72be633%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22104.5%22%20y%3D%2230%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22122.5%22%20y%3D%2230%22%3E20%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22139.5%22%20y%3D%2230%22%3E%25%3C%2Ftext%3E%3C%2Fsvg%3E)

The remaining value of the closing finished goods is the cost to produce them

In the example above, the goods cost

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%226.5%22%20y%3D%2216%22%3E%24%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2222.5%22%20y%3D%2216%22%3E20%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2248.5%22%20y%3D%2216%22%3E000%3C%2Ftext%3E%3Ctext%20font-family%3D%22math135b31cfba37a56451b4768509d%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2274.5%22%20y%3D%2216%22%3E%26%23x2212%3B%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2289.5%22%20y%3D%2216%22%3E%24%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22100.5%22%20y%3D%2216%22%3E4%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22122.5%22%20y%3D%2216%22%3E000%3C%2Ftext%3E%3Ctext%20font-family%3D%22math135b31cfba37a56451b4768509d%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%22144.5%22%20y%3D%2216%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22159.5%22%20y%3D%2216%22%3E%24%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22175.5%22%20y%3D%2216%22%3E16%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%22201.5%22%20y%3D%2216%22%3E000%3C%2Ftext%3E%3C%2Fsvg%3E)

If you know the balance of the provision, then you can find the transfer value of the finished goods by rearranging the formula

Examiner Tips and Tricks

Remember, you use a mark-up percentage to find the transfer value. But if you have the transfer value, you use the margin percentage to find the provision for unrealised profit.

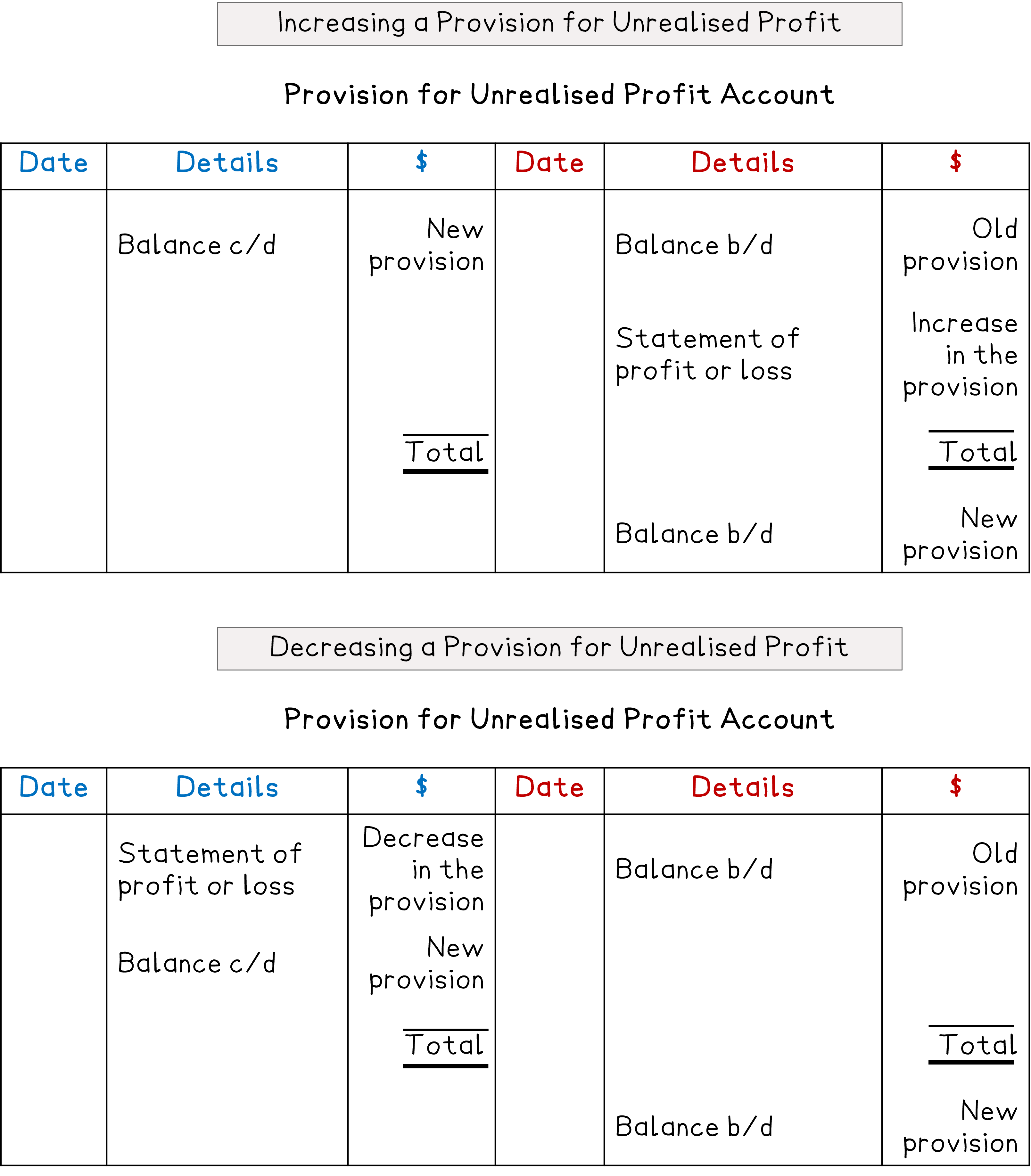

How do I make entries in the provision for unrealised profit account?

STEP 1

Calculate the opening balance and enter this on the credit sideThis uses the value of the opening finished goods

This might be given in the question

STEP 2

Calculate the closing balance and enter this on the debit sideThis uses the value of the closing finished goods

STEP 3

Calculate the change in the balance of the provisionIt is entered on the credit side if it is an increase

It is entered on the debit side if it is a decrease

The other side of the transaction is entered in the statement of profit or loss

Worked Example

P Limited is a manufacturing business. It applies a rate of factory profit of 20%.

At 1 January 2025, the finished goods inventory at transfer value was $28 800.

The cost of production for the goods produced during the year ended 31 December 2025 was $314 000.

At 31 December 2025, the finished goods at transfer value was $21 600.

Prepare the provision for unrealised profit account for the year ended 31 December 2025.

Answer:

Calculate the opening balance of the provision for unrealised profit

![]()

Calculate the closing balance of the provision for unrealised profit

![]()

Calculate the decrease

![]()

Provision for unrealised profit account

$ | $ | ||

|---|---|---|---|

Statement of profit or loss | 1 200 | Balance b/d | 4 800 |

Balance c/d | 3 600 |

| |

4 800 | 4 800 | ||

Balance b/d | 3 600 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?