Manufacturing Account (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

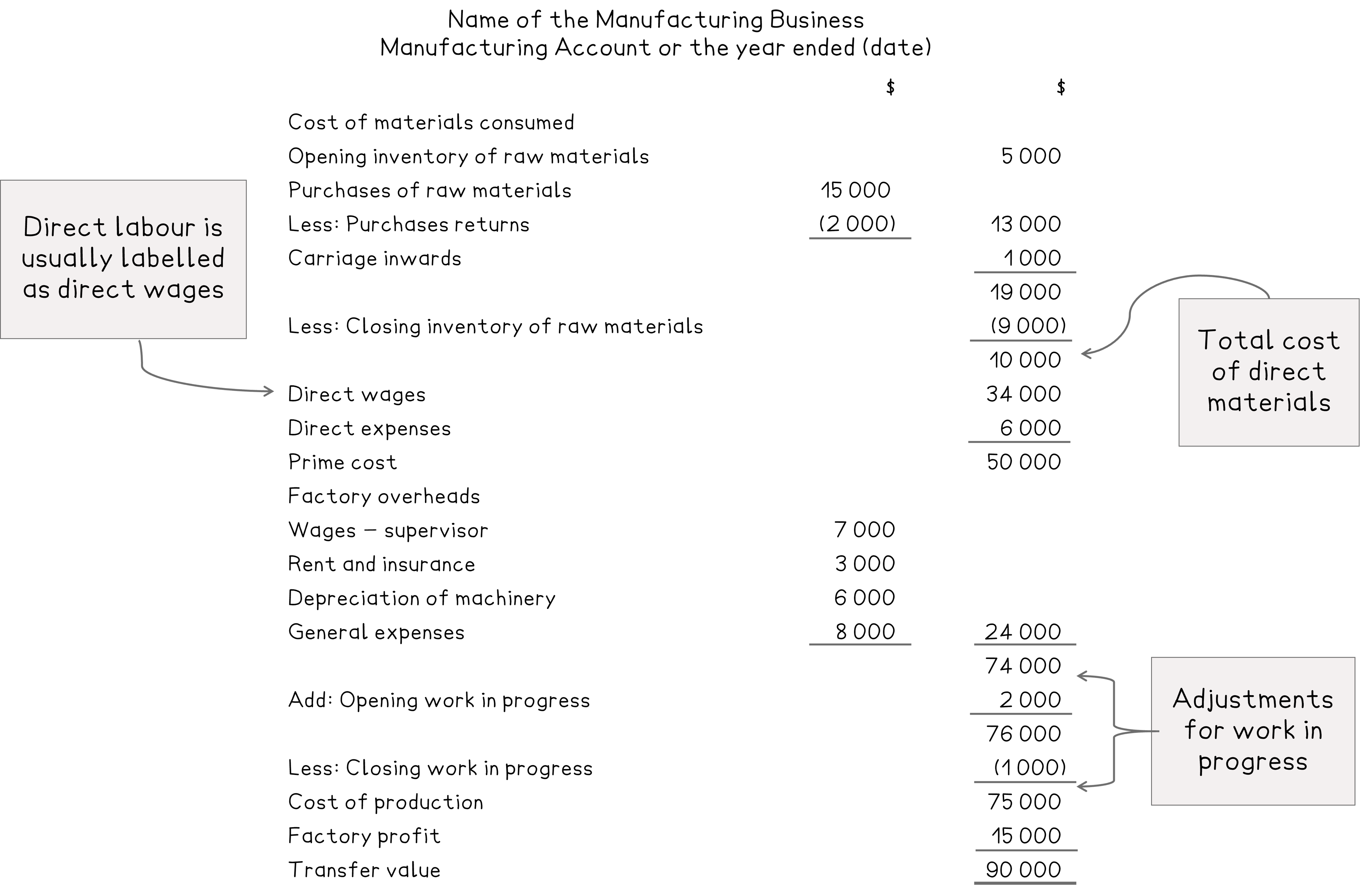

Manufacturing accounts

What is the total cost of production?

The total cost of production is the total of the direct costs and the indirect costs

This is adjusted due to the work in progress not being finished

Add the value of the work in progress from the beginning of the year

Subtract the value of the work in progress from the end of the year

This is similar to dealing with inventory when calculating the net purchases for a trading business

Cost of production

= Direct materials

+ Direct labour

+ Direct expenses

+ Factory overheads

+ Opening work in progress

- Closing work in progress

Examiner Tips and Tricks

A business might use a factory and an office. Only the factory expenses are included in the cost of production.

How do I complete a manufacturing account?

STEP 1

Calculate the cost of materials consumedStart with the opening inventory of raw material

Add the purchases of raw materials

Subtract purchases returns

Add carriage inwards

Subtract the closing inventory of raw materials

STEP 2

Calculate the prime costStart with the cost of materials consumed

Add direct labour

Add direct expenses

STEP 3

Calculate the cost of factory overheadsAdd together any costs linked to the factory but not the production

The production costs should be included in the prime cost

STEP 4

Add the prime cost and the factory overheadsSTEP 5

Adjust for the work in progress to calculate the cost of productionAdd the opening balance for the work in progress to the current total cost

Subtract the closing balance for the work in progress

This final value is the cost of production

STEP 6

Add the factory profit to calculate the transfer valueYou will have to find the mark-up on the cost of production

Examiner Tips and Tricks

Remember the finished goods do not appear on the manufacturing account. They appear on the statement of profit or loss.

Worked Example

Comfy Chairs is a manufacturer of specialist garden chairs. It applies a rate of factory profit of 30%.

The following information is available from the business for the year ended 31 August 2023.

$ | |

Inventory at 1 September 2022 | |

Raw materials | 45 000 |

Work in progress | 6 000 |

Finished goods | 51 000 |

Inventory at 31 August 2023 | |

Raw materials | 53 750 |

Work in progress | 8 000 |

Finished goods | 42 000 |

Purchases of raw materials | 160 000 |

Factory rent | 24 000 |

Royalties | 3 440 |

Depreciation of factory equipment | 6 400 |

Factory heating and lighting | 5 500 |

Wages of factory operatives | 16 000 |

Wages of factory supervisor | 8 000 |

Factory insurance | 4 220 |

Prepare the manufacturing account of Comfy Chairs for the year ended 31 August 2023.

Answer:

Identify:

The direct materials

Raw materials and purchases

The direct labour

Wages of factory operatives

The direct expenses

Royalties

Ignore the inventory of finished goods

The other costs are the factory overheads

Prepare the account in the required format

Multiply the cost of production by 30% to get the factory profit

$216 810 × 30% = $65 043

Comfy Chairs Manufacturing Account for the year ended 31 August 2023 | ||

Cost of material consumed | ||

Opening inventory of raw materials | 45 000 | |

Purchases of raw materials | 160 000 | |

205 000 | ||

Less: Closing inventory of raw materials | (53 750) | |

151 250 | ||

Direct wages - factory operatives | 16 000 | |

Direct expenses - royalties | 3 440 | |

Prime cost | 170 690 | |

Factory overheads | ||

Factory rent | 24 000 | |

Factory insurance | 4 220 | |

Wages - supervisor | 8 000 | |

Factory heating and lighting | 5 500 | |

Depreciation of factory equipment | 6 400 | 48 120 |

218 810 | ||

Add: Opening work in progress | 6 000 | |

224 810 | ||

Less: Closing work in progress | (8 000) | |

Cost of production | 216 810 | |

Factory profit | 65 043 | |

Transfer value | 281 853 | |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?