Statement of Profit or Loss (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

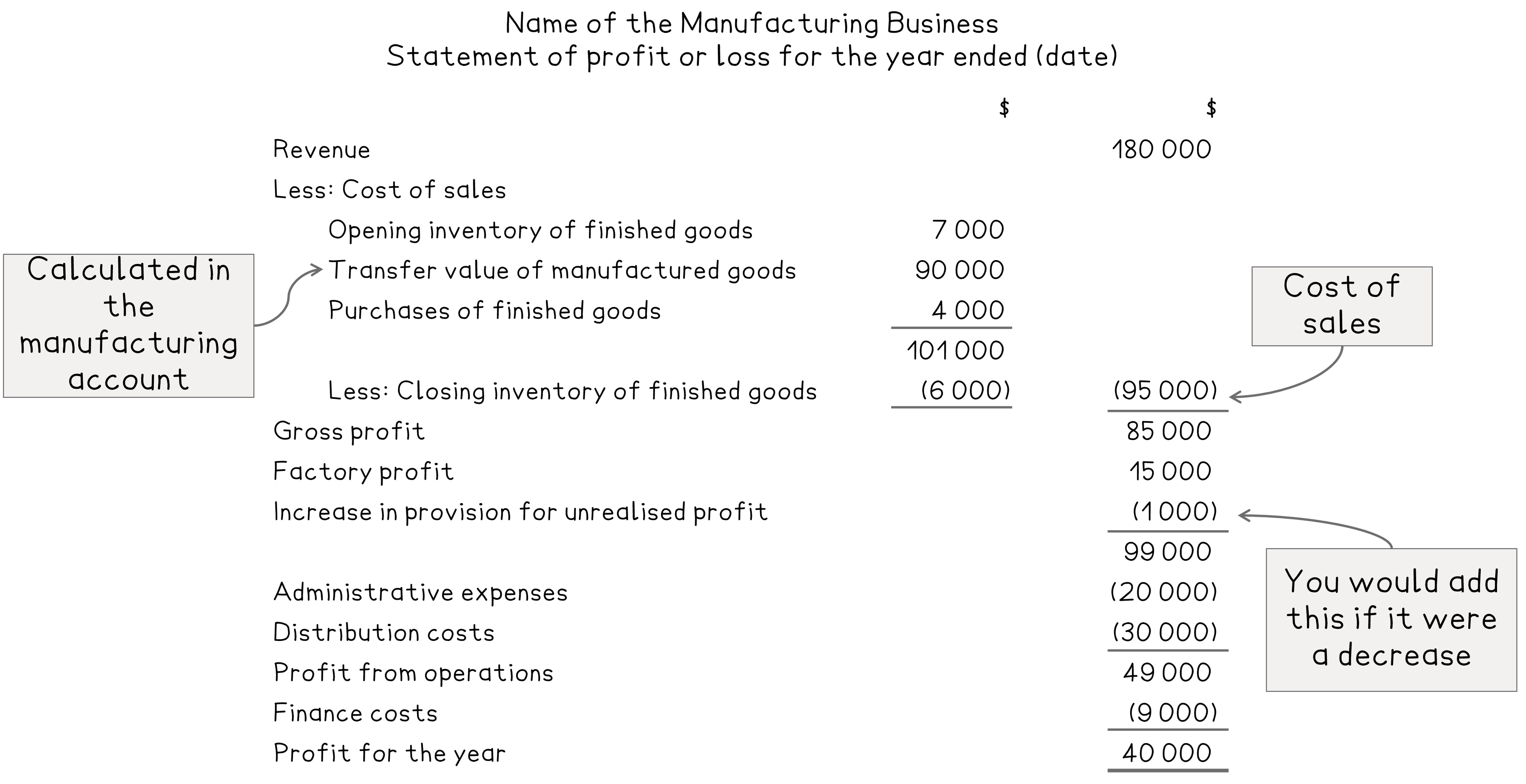

Statements of profit or loss for manufacturing businesses

What is the layout of the statement of profit or loss of a manufacturing business?

The statement of profit or loss for a manufacturing business is prepared in a similar way to the other types of trading businesses

The statement of profit or loss is prepared after the manufacturing account

For the trading section:

Use the inventory for finished goods

Use the goods at transfer value in place of purchases

The business might have also purchased extra finished goods

Add this in the calculation of the cost of sales

Make adjustments after the gross profit for the factory profit and the change in the provision for unrealised profit

Add the factory profit

If the provision for unrealised profit has increased, then subtract the change

If the provision for unrealised profit has decreased, then add the change

For the profit and loss section:

Only include expenses that relate to the non-production aspects of the business

Such as advertising, carriage outwards, etc

The expenses related to manufacturing are included in the cost of production

A business might use a factory and an office

The factory expenses are included in the cost of production

The office expenses are included in the profit and loss section

Worked Example

Pablo owns a small carpet and rug factory, making bespoke carpets for local furniture businesses. He applies a rate of factory profit of 20%.

The following balances are provided at 31 December 2023.

$ | |

Revenue | 280 050 |

Inventory at 1 January 2023 | |

Raw materials | 7 100 |

Work in progress | 10 420 |

Finished goods | 12 450 |

Purchases of raw materials | 96 200 |

Wages of factory workers | 38 000 |

Wages of factory supervisors | 28 500 |

Wages of office and sales staff | 48 000 |

Insurance and rates | 15 000 |

General factory expenses | 13 180 |

General office expenses | 25 750 |

Factory equipment at cost | 120 000 |

Provision for depreciation of factory equipment at 1 January 2023 | 40 000 |

Provision for unrealised profit at 1 January 2023 | 2 075 |

Additional Information

Inventory at 31 December 2023

Raw materials $6 860

Work in progress $10 885

Finished goods $14 640

Insurance and rates are to be apportioned ⅓ to the office and ⅔ to the factory

Factory equipment is to be depreciated at 15% using the reducing balance method

(a) Prepare the manufacturing account for the year ended 31 December 2023.

(b) Prepare the statement of profit or loss for the year ended 31 December 2023.

Answer:

Deal with the additional information

Inventory at 31 December 2023

These appear as current assets on the statement of financial position

The raw materials and work in progress appear on the manufacturing account

The finished goods appear on the statement of profit or loss

Insurance and rates are to be apportioned ⅓ to the office and ⅔ to the factory

Find the amount for the office

⅓ × $15 000 = $5 000

This appears in the profit and loss section of the statement of profit or loss

Find the amount for the factory

⅔ × $15 000 = $10 000

This appears on the manufacturing account as a factory overhead

Factory equipment is to be depreciated at 15% using the reducing balance method

Find the net book value of the factory equipment

$120 000 - $40 000 = $80 000

Calculate the year's depreciation charge

15% × $80 000 = $12 000

This appears on the manufacturing account as a factory overhead

Multiply the cost of production by 20% to find the factory profit

$197 655 × 20% = $39 531

(a)

Prepare the manufacturing account

Pablo Manufacturing Account for the year ended 31 December 2023 | ||

$ | $ | |

Cost of material consumed | ||

Opening inventory of raw materials | 7 100 | |

Purchases of raw materials | 96 200 | |

103 300 | ||

Less: Closing inventory of raw materials | (6 860) | |

96 440 | ||

Direct wages - factory workers | 38 000 | |

Prime cost | 134 440 | |

Factory overheads | ||

Wages - Supervisors | 28 500 | |

Insurance and rates | 10 000 | |

General expenses | 13 180 | |

Depreciation of factory equipment | 12 000 | 63 680 |

198 120 | ||

Add: Opening work in progress | 10 420 | |

208 540 | ||

Less: Closing work in progress | (10 885) | |

Cost of production | 197 655 | |

Factory profit | 39 531 | |

Transfer value | 237 186 | |

(b)

Calculate the balance of the provision for unrealised profit account

![]()

Calculate the increase in the provision

$2 440 - $2 075 = $365

Prepare the trading section of the statement of profit or loss

Pablo Statement of Profit or Loss (trading section) for the year ended 31 December 2023 | ||

$ | $ | |

Revenue | 280 050 | |

Less: Cost of sales | ||

Opening inventory of finished goods | 12 450 | |

Goods at transfer value | 237 186 | |

249 636 | ||

Less: Closing inventory of finished goods | (14 640) | (234 996) |

Gross Profit | 45 054 | |

Factory profit | 39 531 | |

Increase in provision for unrealised profit | (365) | |

84 220 | ||

Insurance and rates | 5 000 | |

Wages of office and sales staff | 48 000 | |

General office expenses | 25 750 | (78 750) |

Profit for the year | 5 470 | |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?