Goodwill (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

Goodwill

What is goodwill?

Goodwill is an intangible non-current asset

It has no physical existence

It cannot be sold separately from the business

Why might a business have goodwill?

The following are reasons why a business might have goodwill

A good reputation, well-known brand and strong image

Having many loyal customers

Having good relationships with suppliers

Being in a good location

Having experienced and efficient employees

What is the difference between inherent and purchased goodwill?

Inherent goodwill is internally generated

A business gains this naturally over time by their continued efforts

Inherent goodwill is not included in the financial statements or maintained in the book of accounts because:

its valuation is highly subjective as there is not an agreed formula to measure it

the assets of a business should not be overstated according to the prudence concept

the factors that create goodwill (like reputation) are difficult to measure in monetary terms

Purchased goodwill is gained when a business is purchased or taken over by another business

Purchased goodwill is calculated by subtracting the fair value of the net assets from the price paid

Purchased goodwill is included in the financial statements and maintained in the book of accounts

Why should I use a goodwill account for inherent goodwill?

Use a goodwill account when there is a change in a partnership

change in the partners' profit-sharing ratio

introduction of a new partner

retirement of an existing partner

dissolution of a partnership

The partners' capital accounts are adjusted so that the goodwill account can be immediately written off

The value of the goodwill is added to the partners' capital accounts using the old profit-sharing ratio

These are credit entries to the capital accounts

The goodwill is then eliminated by subtracting the value from the partners' capital accounts using the new profit-sharing ratio

These are debit entries to the capital accounts

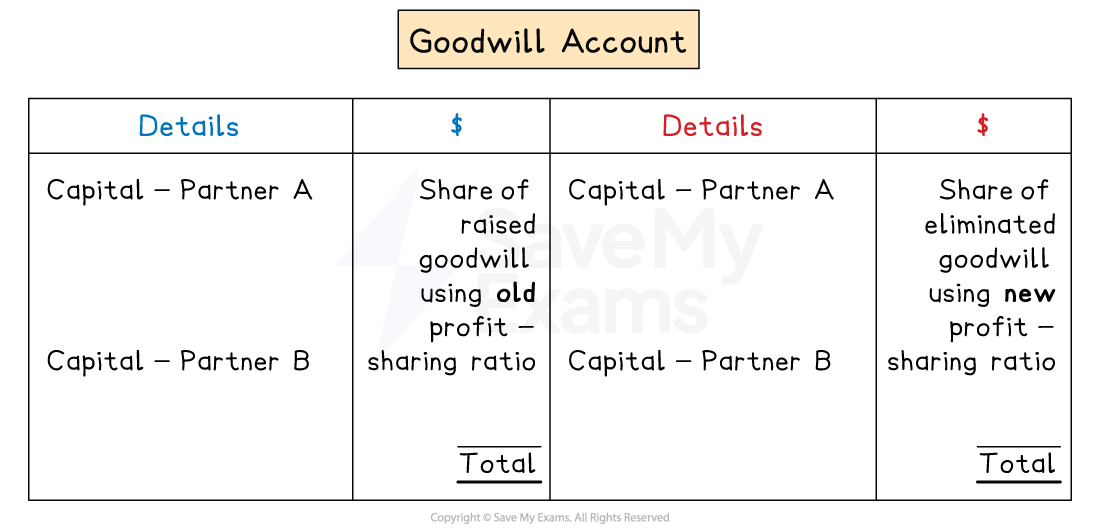

What is the layout of a goodwill account?

Goodwill is raised by making entries on the debit side

It is shared between the partners' capital accounts using the old ratio

It is on the debit side as it represents an asset

Goodwill is written off by making entries on the credit side

It is shared between the partners' capital accounts using the new ratio

Examiner Tips and Tricks

You will not be asked to prepare a goodwill account for inherent goodwill. However, you can still use one if you find them helpful.

Worked Example

Tom and Jerry are in a partnership and they share profits and losses equally.

On 1 January 2026, they changed their partnership agreement so that the profit and loss sharing ratio would be Tom 40% and Jerry 60%.

The balances on the capital accounts at 31 December 2025 were:

$ | |

|---|---|

Tom | 40 000 |

Jerry | 50 000 |

Goodwill was valued at two times the average profits of the last three years.

The profits for the last three years were:

$ | |

|---|---|

2025 | 42 000 |

2024 | 38 000 |

2023 | 31 000 |

Calculate the capital account balance of each partner at 1 January 2026.

Answer:

Calculate the average profit of the last three years

![]()

Find the value of the goodwill

![]()

Calculate the share of the goodwill using the old ratio

Tom: ![]()

Jerry: ![]()

Calculate the share of the goodwill using the new ratio

Tom: ![]()

Jerry: ![]()

Calculate the new capital balances

Add the share of goodwill using the old ratio

Subtract the share of goodwill using the new ratio

Tom $ | Jerry $ | |

|---|---|---|

Balance at 31 December 2025 | 40 000 | 50 000 |

Goodwill | 37 000 | 37 000 |

Goodwill eliminated | (29 600) | (44 400) |

Capital account at 1 January 2026 | 47 400 | 42 600 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?