Realisation Account (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

Realisation account

What is a realisation account?

A realisation account is used when a business (usually a partnership) is being dissolved, sold, or acquired by another business

It is a temporary account

It is opened only when the business is closing

It is used to close the accounting books of the old partnership and calculate the final profit or loss on realisation

This is the overall net gain or loss made from selling off or dissolving the business

The resulting profit or loss is then transferred to the partners' capital accounts in their profit-sharing ratio

The realisation account is then closed

It is very similar to a revaluation account

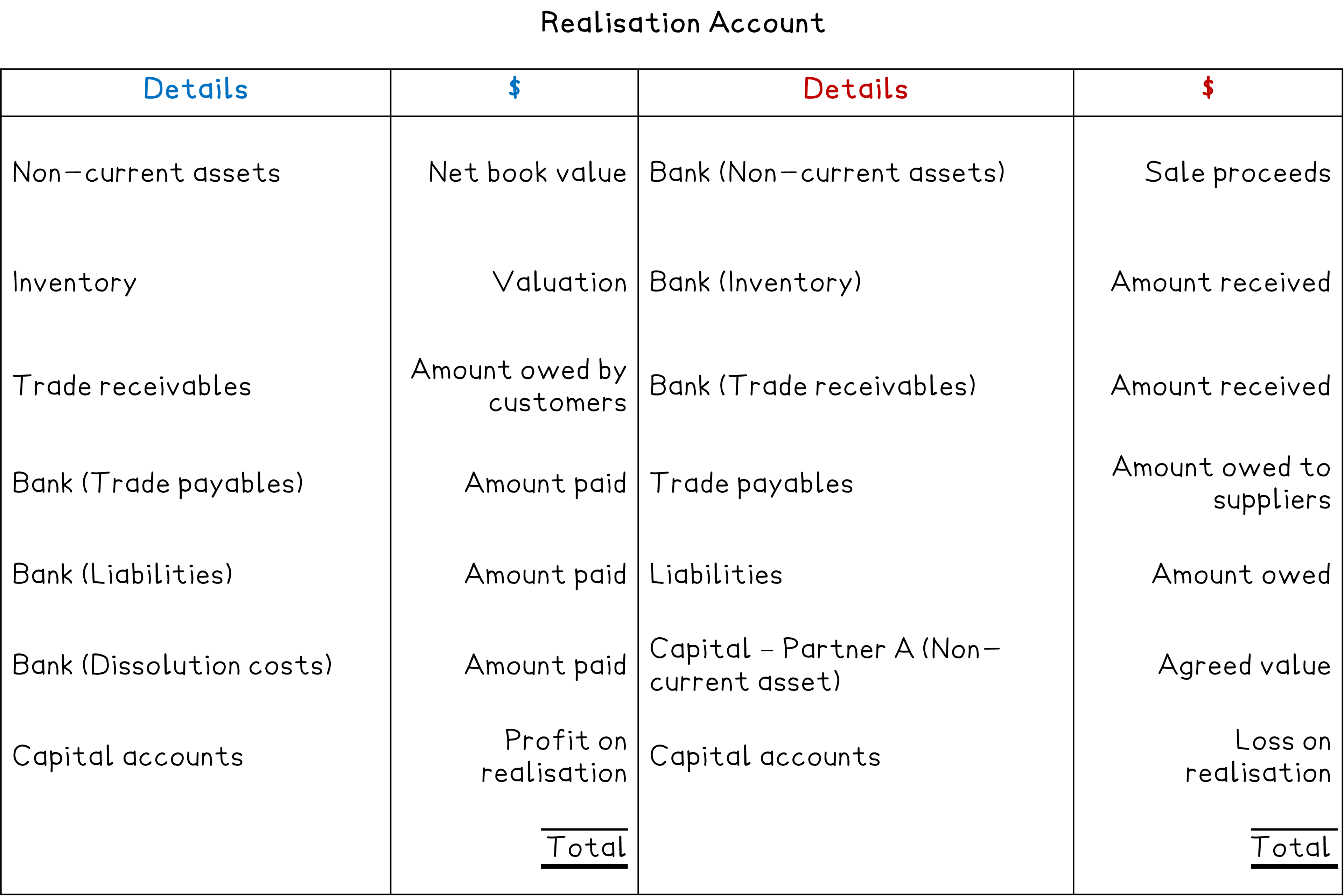

How do I prepare a realisation account?

STEP 1

Enter the non-current assets into the realisation accountNon-The current net book value is entered on the debit side

The proceeds from the sale of the assets is entered on the credit side

This includes an agreed amount if a partner takes an asset for their personal use

STEP 2

Enter the current assets (apart from the bank balance) into the realisation accountThe current amount owed by customers is entered on the debit side

The actual amount received is entered on the credit side

STEP 3

Enter the liabilities (apart from the bank overdraft) into the realisation accountThe current amount owed to suppliers is entered on the credit side

The actual amount paid is entered on the debit side

STEP 4

Enter any additional amounts such as discounts or realisation costsExpenses are entered on the debit side

Such as discount allowed, realisation costs

Incomes are entered on the credit side

Such as discount received

STEP 5

Find the balancing figureIt is a net profit on realisation if it is on the debit side

It is a net loss on realisation if it is on the credit side

STEP 6

Share the net profit or loss on realisation between the partners' capital accounts using the profit-sharing ratio

Examiner Tips and Tricks

Remember, the bank balance or the bank overdraft is not entered into the realisation account.

If you struggle to remember what goes on which side, then consider the other side of the transaction.

For example, to remove a loan, a debit entry is made in its account. Therefore, the entry in the realisation account is on the credit side.

Worked Example

Clark and Lois were in partnership sharing profits and losses in the ratio 3:2 respectively.

The statement of financial position at 31 December 2025 was as follows:

$ | $ | $ | |

|---|---|---|---|

Assets | |||

Non-current assets | 125 000 | ||

Current assets | |||

Inventory | 37 000 | ||

Trade receivables | 23 000 | 60 000 | |

Total assets | 185 000 | ||

Capital and liabilities | |||

Capital | Clark | Lois | Total |

Capital accounts | 80 000 | 60 000 | 140 000 |

Current accounts | (1 000) | 5 000 | 4 000 |

79 000 | 65 000 | 144 000 | |

Non-current liabilities | |||

Bank loan | 20 000 | ||

Current liabilities | |||

Bank overdraft | 8 000 | ||

Trade payables | 13 000 | 21 000 | |

Total capital and liabilities | 185 000 |

The partners agreed to dissolve the partnership on 31 December 2025.

The following transactions took place as part of the dissolution process.

As part of his settlement, Clark took a vehicle with a net book value of $20 000.

As part of her settlement, Lois took a vehicle with a net book value of $25 000.

All remaining non-current assets were sold for $75 000.

Inventory was sold for $29 000.

Irrecoverable debts of $500 were written off and the remaining credit customer paid their balances in full.

$22 500 was paid to clear the bank loan including early repayment charges.

Trade payables were paid in full.

Dissolution costs of $3 000 were paid.

Prepare the realisation account to record the dissolution of the partnership.

Answer:

Calculate the amount received from trade receivables

$23 000 - $500 = $22 500

Enter the amounts into the realisation account

Find the balancing figure

$223 500 - $204 500 = $19 000

Share the figure between Clark and Lois

$19 000 ÷ (3 + 2) = $3 800

Clark: 3 × $3 800 = $11 400

Lois: 2 × $3 800 = $7 600

$ | $ | ||

|---|---|---|---|

Non-current assets | 125 000 | Capital - Clark (Vehicle) | 20 000 |

Inventory | 37 000 | Capital - Lois (Vehicle) | 25 000 |

Trade receivables | 23 000 | Bank (Non-current assets) | 75 000 |

Bank (Bank loan) | 22 500 | Bank (Inventory) | 29 000 |

Bank (Trade payables) | 13 000 | Bank (Trade receivables) | 22 500 |

Dissolution costs | 3 000 | Bank loan | 20 000 |

Trade payables | 13 000 | ||

Capital - Clark (Loss on realisation) | 11 400 | ||

| Capital - Lois (Loss on realisation) | 7 600 | |

223 500 | 223 500 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?