Revaluation Account (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

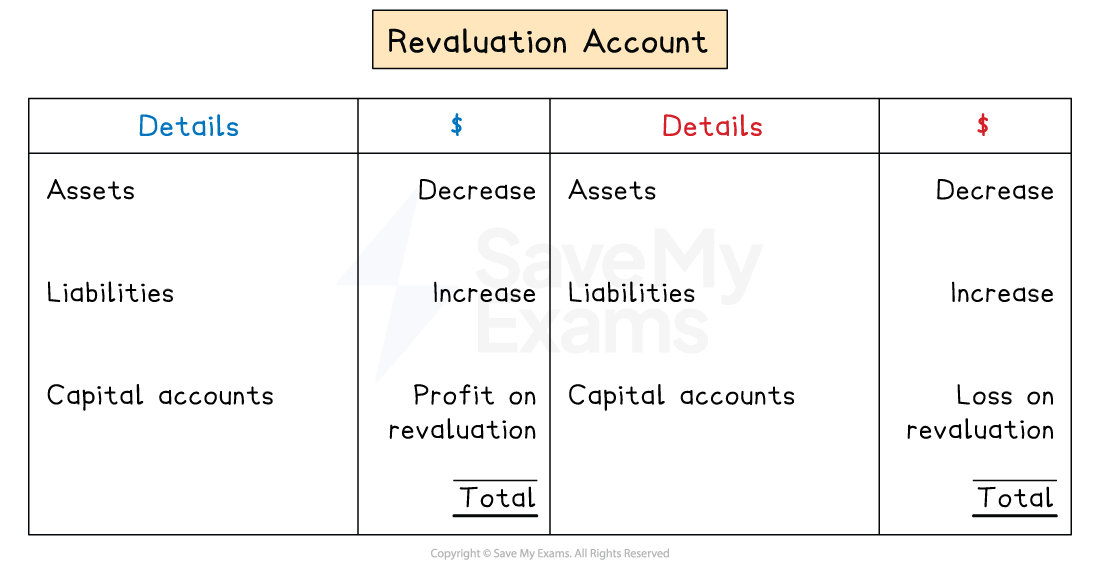

Revaluation account

What is a revaluation account?

A revaluation account is a temporary account

It is used to calculate the net profit or loss when adjusting the book values of assets and liabilities to their current fair values

It is used when a partnership continues to operate but its structure changes

Such as the introduction of a new partner or the retirement of an existing partner

Why is a revaluation account used?

It is important that an accurate current value of a business is found before making any changes to the structure of the partnership

The assets might have increased in value since their purchase

The current partners should benefit from this increase before changing the structure

Revaluing assets and liabilities, before changing the structure of the partnership, ensure that

new partners do not unfairly benefit from past gains

new partners are not unfairly penalised for past losses

How do I prepare a revaluation account?

STEP 1

Work out the increase or decrease of each assetIncreases are on the credit side

Decreases are on the debit side

STEP 2

Work out the increase or decrease of each liabilityIncreases are on the debit side

Decreases are on the credit side

STEP 3

Find the balancing figureIt is a net profit on revaluation if it is on the debit side

It is a net loss on revaluation if it is on the credit side

STEP 4

Share the net profit or loss on revaluation between the partners' capital accounts using the old profit-sharing ratio

Examiner Tips and Tricks

If you struggle to remember what goes on which side, then consider the other side of the transaction.

For example, if an asset increases in value, then the asset account will have a debit entry to increase its value. Therefore, the revaluation account will have a credit entry.

Questions do not tend to ask you to prepare the revaluation account, they mainly ask you to find the effects on the capital accounts. However, it is helpful to sketch a quick revaluation account to help with this calculation.

Worked Example

Ameena and Bilal are in partnership and share profits and losses in the ratio 7:4 respectively.

The following balances were available on 31 December 2025.

$ | |

|---|---|

Vehicles at cost | 30 000 |

Accumulated depreciation of vehicles | 12 500 |

Trade receivables | 62 500 |

Inventory | 11 000 |

Capital accounts | |

Ameena | 60 000 |

Bilal | 35 000 |

Ameena and Bilal admit a new partner, Carry, on 1 January 2026. Profits and losses are to be shared between Ameena, Bilal and Carry in the ratio 4:2:1 respectively.

They agree the following valuations:

$ | |

|---|---|

Vehicles | 20 000 |

Inventory | 9 000 |

They also agreed to write off trade receivables' balances totalling $6 000 as irrecoverable debts.

Find the balance on Ameena's capital account after the revaluation.

Answer:

Calculate the net book value of the vehicles before the revaluation

$30 000 - $12 500 = $17 500

Calculate the increase in value of the vehicles

$20 000 - $17 500 = $2 500

Calculate the decrease in inventory

$11 000 - $9 000 = $2 000

Work out the net loss on revaluation

$ | |

|---|---|

Increase in vehicles | 2 500 |

Decrease in inventory | (2 000) |

Decrease in trade receivables | (6 000) |

Loss on revaluation | (5 500) |

Find the share of the loss for Ameena using the old ratio

![]()

Note that the revaluation account would look like:

Revaluation account

$ | $ | ||||

|---|---|---|---|---|---|

2026 | 2026 | ||||

Jan 1 | Inventory | 2 000 | Jan 1 | Vehicles | 2 500 |

Trade receivables | 6 000 | Capital - Ameena (loss on revaluation) | 3 500 | ||

| Capital - Bilal (loss on revaluation) | 2 000 | |||

8 000 | 8 000 |

Calculate Ameena's capital account balance

$ | |

|---|---|

Increase in vehicles | 2 500 |

Balance on 31 December 2025 | 60 000 |

Loss on revaluation | (3 500) |

Balance on 1 January 2026 | 56 500 |

$56 500

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?