Economic Resources (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

The factors of production

Factors of production are the resources used to produce goods and services

Land, labour, capital and enterprise

The production of any good/service requires the use of a combination of all four factors of production

Goods are physical objects that can be touched (tangible) e.g. mobile phone

Services are actions or activities that one person performs for another (intangible) e.g. manicure, car wash

The four factors of production

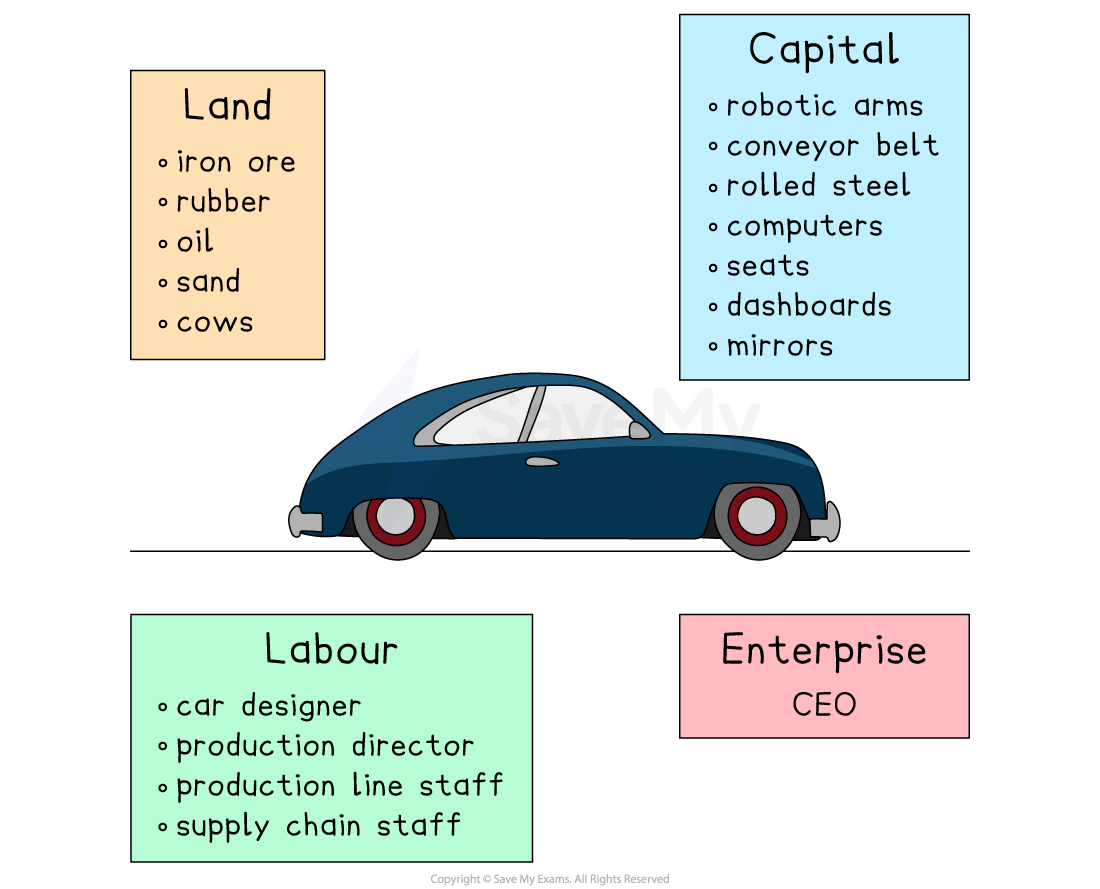

1. Land

Non man-made natural resources available for production

Some countries have a vast amount of a particular natural resource and so are able to specialise in its production

E.g., oil, wood, fish, corn, iron ore

2. Labour

The human input into the production process

Labour involves mental or physical effort

Not all labour is of the same quality

It can be skilled or unskilled

Some workers are more productive than others because of their education, training and experience

3. Capital

Capital is any man-made resource that is used to produce goods and services

E.g., tools, buildings, machines and computers

4. Enterprise

Enterprise involves taking risks in setting up or running a firm

An entrepreneur decides on the combination of the factors of production necessary to produce good and services with the aim of generating profit

Some of the factors of production required to produce a motor car

The difference between human capital and physical capital

Physical capital

Refers to tangible assets like factories, machinery, and infrastructure

Created through investments by businesses and governments

Especially crucial for economic growth in low-income and lower-middle-income countries

Both quality and quantity of physical capital matter

Human capital

Represents the value of labour in driving productivity and future economic growth

Includes skills, knowledge, and experience of individuals and the workforce

Seen as an investment by individuals, employers, and governments

Influences future earnings and national economic performance

Rewards for the factors of production

In a free market economic system, the factors of production are privately owned by households or firms

Households make these resources available to firms that use them to produce goods/services

Firms purchase land, labour, and capital from households in factor markets

Households receive the following financial rewards (factor income) for selling their factors of production

The factor income for land → rent

The factor income for labour → wages

The factor income for capital → interest

The factor income for entrepreneurship → profit

Specialisation and the division of labour

The division of labour is when a task is broken up into several component tasks

This allows workers to specialise by focusing on one (or a few) of the components that make up the production process and thereby gain significant skill in doing it

This results in higher output per worker and so increases productivity

Based on observations made during a visit to a pin factory, famous economist Adam Smith developed the ideas of specialisation and the division of labour

He noted that a single worker could not make more than 20 pins a day as it involved around 18 different processes, such as cutting the wire, sharpening the end, stamping the head etc.

However, if the labour was divided up into different tasks and workers specialised in just that one task, Adam Smith estimated that just 10 workers could produce 48,000 pins per day

Specialisation occurs on several different levels

On an individual level

On a business level, for example, one firm may only specialise in manufacturing drill bits for concrete work

On a regional level, for example, Silicon Valley has specialised in the tech industry

On a global level, as countries seek to trade, for example Bangladesh specialises in textiles and exports them to the world

Advantages and disadvantages of the division of labour and specialisation

Pros | Cons |

|---|---|

|

|

|

|

|

|

|

|

|

|

Pros and cons of the division of labour and specialisation in international trade

Pros | Cons |

|---|---|

|

|

|

|

|

|

|

|

The role of entrepreneurs

Entrepreneurs play a vital role in organising production by bringing the factors of production together to create business ventures

They often take financial risks, using either their own funds or borrowed capital, in pursuit of new opportunities

Success in entrepreneurship typically depends on a mix of personal traits and strategic thinking

An entrepreneur is a person who is willing and able to create a new business idea or invention and takes risks in pursuing success

Successful entrepreneurs can identify and pursue opportunities, create value for customers and build thriving businesses

Entrepreneurs display three main characteristics

1. They organise resources

An entrepreneur must be able to gather and coordinate the resources necessary to start and operate a business

E.g., when Michael Dell started his computer company from his garage, he had to organise resources such as space, computers, software tools, and employees, and manage the finances

2. They take risks

Entrepreneurship involves taking risks – financial, personal, or professional

E.g., an entrepreneur may invest their life savings into a new venture or quit a secure job to start their own business

They may also take risks by introducing new products or entering new markets

These risks can pay off with great rewards, but they can also lead to failure and financial loss

As a business grows an entrepreneur may make the decision to employ staff to help with its day-to-day operations

The entrepreneur may take on the role of mentor, supporting new staff members to carry out their tasks in a particular way

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?