Short-Run Production (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

Short-run production function

The production function shows the relationship between inputs used in production and the level of output produced

In the short run, at least one factor of production is fixed, meaning it cannot be changed quickly

Firms increase output mainly by adjusting variable factors

When additional variable factors are added to fixed factors, output changes according to the production function

Fixed factors of production

Inputs that cannot be changed in the short run

Their quantity remains constant as output changes

Examples include:

Machinery

Buildings

Land

Large equipment

Variable factors of production

Inputs that can be changed in the short run

Firms adjust these to increase or decrease production

Examples include:

Labour

Raw materials

Energy inputs

Types of product

1. Total product (TP)

Total product (TP) is the total quantity of output produced using a given amount of labour and other inputs

For example:

A bakery produces 100 loaves of bread with one baker

With two bakers, output increases to 180 loaves

As more workers are added, total output increases, although the rate of increase may change

2. Marginal product (MP)

Marginal product (MP) is the additional output produced by employing one more unit of labour

Formula:

![]()

Where:

ΔTP = change in total product

ΔQL = change in quantity of labour

For example:

Output increases from 100 loaves to 180 loaves when a second worker is hired

The marginal product of the second worker is 80 loaves

Marginal product shows how much extra output each additional worker produces

3. Average product (AP)

Average product (AP) measures the output produced per worker

Formula:

![]()

Where:

TP = total product

QL = quantity of labour

For example:

If three bakers produce 240 loaves, then

format('truetype')%3Bfont-weight%3Anormal%3Bfont-style%3Anormal%3B%7D%3C%2Fstyle%3E%3C%2Fdefs%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2211.5%22%20y%3D%2230%22%3EAP%3C%2Ftext%3E%3Ctext%20font-family%3D%22math17f39f8317fbdb1988ef4c628eb%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2235.5%22%20y%3D%2230%22%3E%3D%3C%2Ftext%3E%3Cline%20stroke%3D%22%23000000%22%20stroke-linecap%3D%22square%22%20stroke-width%3D%221%22%20x1%3D%2250.5%22%20x2%3D%2277.5%22%20y1%3D%2223.5%22%20y2%3D%2223.5%22%2F%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2264.5%22%20y%3D%2216%22%3ETP%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2264.5%22%20y%3D%2241%22%3EQL%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2211.5%22%20y%3D%2281%22%3EAP%3C%2Ftext%3E%3Ctext%20font-family%3D%22math17f39f8317fbdb1988ef4c628eb%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2235.5%22%20y%3D%2281%22%3E%3D%3C%2Ftext%3E%3Cline%20stroke%3D%22%23000000%22%20stroke-linecap%3D%22square%22%20stroke-width%3D%221%22%20x1%3D%2250.5%22%20x2%3D%2280.5%22%20y1%3D%2274.5%22%20y2%3D%2274.5%22%2F%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2265.5%22%20y%3D%2267%22%3E240%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2265.5%22%20y%3D%2292%22%3E3%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2211.5%22%20y%3D%22118%22%3EAP%3C%2Ftext%3E%3Ctext%20font-family%3D%22math17f39f8317fbdb1988ef4c628eb%22%20font-size%3D%2216%22%20text-anchor%3D%22middle%22%20x%3D%2235.5%22%20y%3D%22118%22%3E%3D%3C%2Ftext%3E%3Ctext%20font-family%3D%22Times%20New%20Roman%22%20font-size%3D%2218%22%20text-anchor%3D%22middle%22%20x%3D%2257.5%22%20y%3D%22118%22%3E80%3C%2Ftext%3E%3C%2Fsvg%3E)

So the average product is 80 loaves per worker

The law of diminishing returns

The law of diminishing returns (also called the law of variable proportions) states that:

When increasing amounts of a variable factor are added to a fixed factor, the marginal product of the variable factor will eventually fall

This occurs because the fixed factor becomes a constraint on production.

For instance, in a small coffee shop:

The first barista works efficiently alone

A second barista improves output, but not as dramatically

By the time a sixth barista is hired, they may be crowding each other, leading to minimal gains in output

Eventually, adding more workers does not increase total output significantly and may even reduce efficiency

Short-run production in a coffee shop

Workers | Total Product | Marginal Product | Average Product |

|---|---|---|---|

1 | 100 | 100 | 100 |

2 | 180 | 80 | 90 |

3 | 240 | 60 | 80 |

4 | 280 | 40 | 70 |

5 | 300 | 20 | 60 |

This table shows how output increases with each additional worker, but at a decreasing rate

Eventually, output plateaus, illustrating diminishing returns

Stages of production

The law of diminishing returns leads to three stages of production

Firms usually operate in Stage 2, where production is still increasing but diminishing returns have begun

Stage 1: Increasing returns

Marginal product increases

Workers specialise and production becomes more efficient

Stage 2: Diminishing returns

The marginal product begins to fall

Additional workers still increase output but at a decreasing rate

Stage 3: Negative returns

The marginal product becomes negative

Too many workers cause crowding and inefficiency

Total output may begin to fall

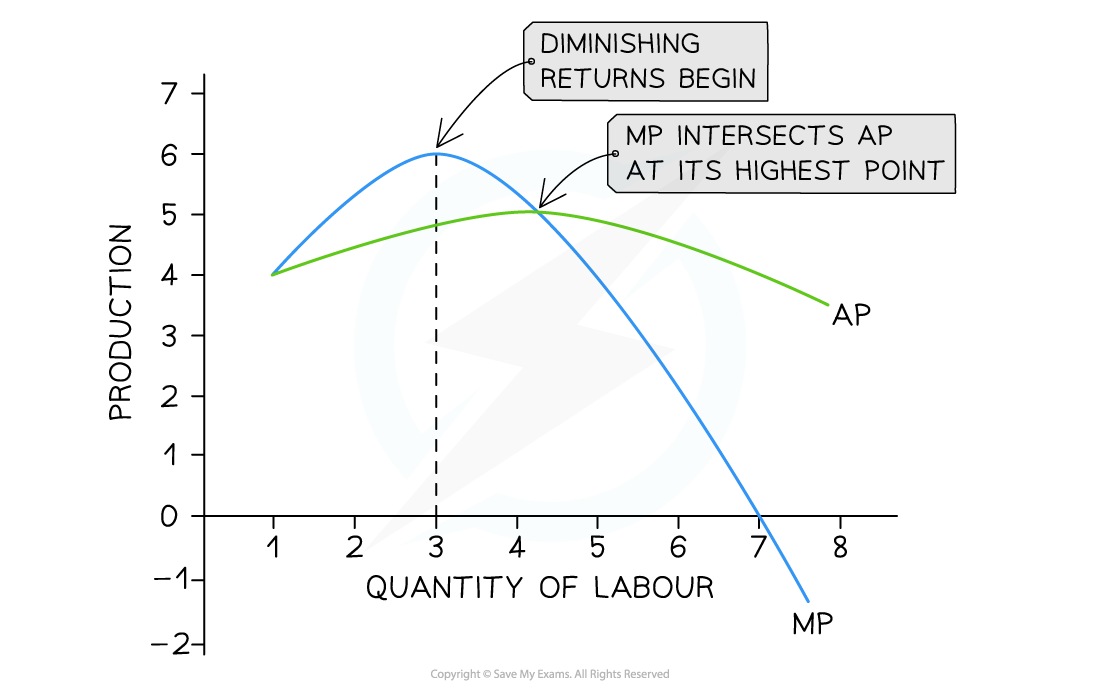

Diagram analysis

A small food van selling burgers at a music festival increases productivity up to the third worker as workers specialise and the grill is used more efficiently

After this point, workers begin to get in each other's way and there is limited grill space (capital), so the marginal product of labour begins to fall

Hiring additional workers still increases total product, but at a diminishing rate

When the 7th worker is hired, the marginal product becomes negative, causing total product to fall

Understanding the short-run production function helps firms

Decide how many workers to hire

Estimate the cost of increasing output

Identify the point at which adding more labour becomes inefficient

It also supports broader economic analysis of resource allocation, productivity, and cost structures in different industries

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?