Reasons For the Economic Boom (Cambridge (CIE) IGCSE History): Revision Note

Exam code: 0470 & 0977

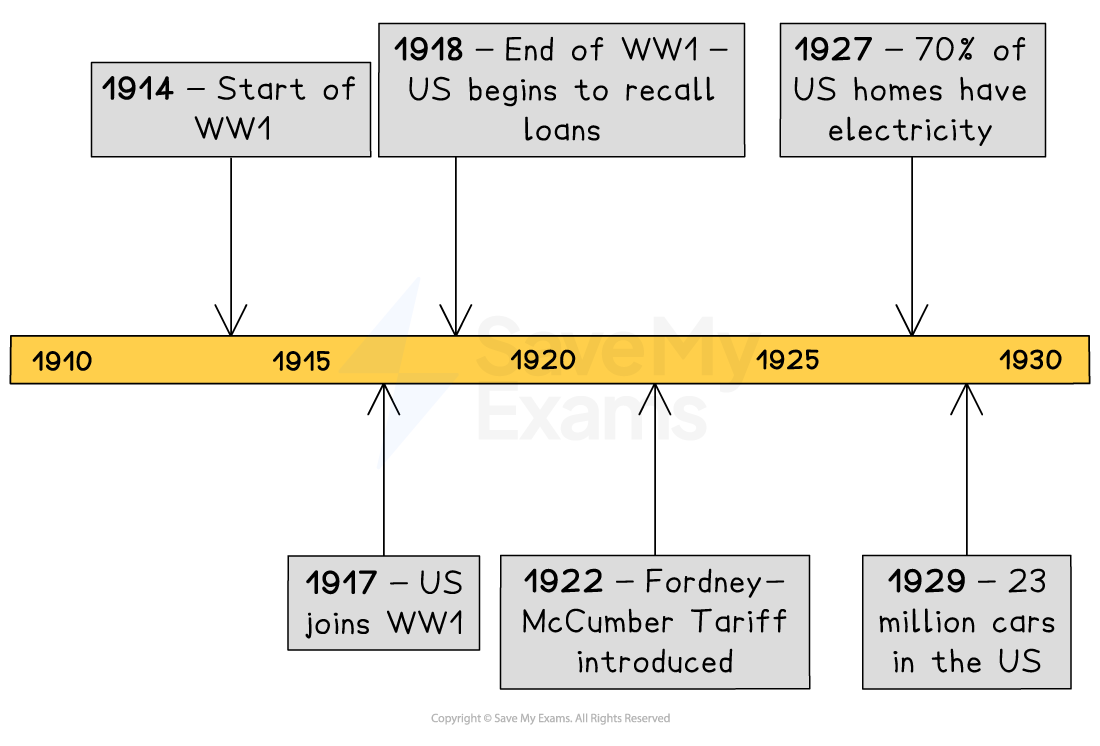

Timeline & Summary

An economic boom is a period of rapid economic growth and prosperity within a country. During the 1920s, the US experienced an economic boom. Many factors contributed to this growth. One key factor was the emergence of new industries and technologies — such as cars, radios and consumer appliances — due to innovation and investment.

In the 1920s, there was also an increase in consumer spending. Workers had more disposable income than ever before due to rising wages and increased access to credit. This allowed more US citizens to purchase goods and services. Businesses had to produce more to meet this demand, further increasing their profits.

Republican government policies also helped the economy boom. They cut taxes and allowed businesses to operate without government intervention. This promoted business investment and entrepreneurship.

The economic boom of the 1920s had a significant impact on the US. It led to a rising standard of living, increased urbanisation and the emergence of a modern consumer culture. The widespread availability of consumer technology transformed daily life for many US citizens. New products and wealth offered an opportunity for leisure and entertainment.

The First World War

Many American citizens did not want the US to join the First World War

They believed that the US should remain neutral

The US eventually entered the war in 1917

The US did not suffer as much as European countries in the First World War

No fighting occurred on US soil

The US suffered fewer casualties

Before entering the First World War, the US gave loans to Allied countries

At the end of the conflict, the US began to recall the loans to Europe, which increased American wealth

The UK repaid $7.5b to the US

The First World War did not destroy US industry or infrastructure

European countries needed goods to rebuild their infrastructure and economies

The US began selling goods to overseas markets that were unable to make their own

Mass production

Mass production is a way of making lots of products quickly. This can involve:

Machinery

Improving the manufacturing process

Many US industries embraced mass production in the 1920s

The car industry was one of the key industries to use mass production

In 1913, Henry Ford developed the concept of the moving assembly line with the Ford Model T car

The car moved through the factory on a conveyor belt

Each worker and machine only focused on one task in the car’s production; for example, attaching the front bumper

The car moved through each stage until it was fully assembled

Each Model T was the same colour (black) and had the same engine size, which reduced costs

In the 1920s, one Model T was made every ten seconds

By 1929, there were 23m cars in the US

The mass production of cars led to improvements in the US road network, as well as the development of cities and suburbs

The expansion of the car industry also led to the growth of other industries

Steel, rubber, glass, leather and oil manufacturers all boomed because they supplied parts to the car industry

Other American industries soon adopted the assembly line

This made more and more goods affordable for US citizens

New technology

In 1916, only 15 per cent of American homes had electricity

By 1927, this had increased to 70 per cent

New electrical gadgets such as refrigerators, vacuum cleaners and washing machines were bought in huge numbers by Americans in the 1920s

The number of radios owned by Americans increased from 60,000 in 1919 to 10m by 1929

Hire-purchase schemes

Hire-purchase is a small loan that enables a person to purchase goods without having the money needed to buy them outright

Consumers can buy a product such as a vacuum cleaner on credit

Consumers then pay for the product in monthly instalments over many months

Hire-purchase became very popular in 1920s America

It meant that people could buy a lot of products without needing to pay for them on the day of purchase

This encouraged people to buy more new goods than they could necessarily afford

This, in turn, encouraged mass production and increased profits for businesses

Republican policies

The Republican Party tried to help American business in the 1920s in a number of ways

Reducing taxes

By giving less money to the government, businesses made more profits

The businesses could then invest their profits back into the company. For example, they could build new factories and employ new workers

Having a laissez-faire approach to business

This is French for “allow to do”

It meant that the Republican government did not interfere with how businesses were run

In addition to this, Congress passed the Fordney–McCumber Tariff in 1922

This placed a tariff or tax on foreign goods entering the US

This made foreign-made goods more expensive and encouraged American consumers to buy goods made in the US

Confidence in the economy

Many US citizens believed that the economic boom would last forever

This led to more workers purchasing shares in companies than ever before

Many workers bought shares “on the margin”

This meant that they borrowed money using low-interest loans and used it to buy the shares

The demand for shares caused prices to rise and led to many working class people making large profits on the stock market

They used these profits to pay off their loans and then buy consumer goods, such as cars and refrigerators, or invest in more shares

This all helped to boost the US economy

Worked Example

What policies did Republican Governments follow in the 1920s to encourage industrial growth?

[4 marks]

Answer:

Republican governments attempted to encourage industrial growth in a number of ways. One way was by lowering taxes. This led to businesses making higher profits, as they did not have to pay as much in tax. The idea was that the business owners would invest these profits in their business and expand it. This would lead to an ever bigger and more profitable business that, even though it paid a lower rate of tax, would eventually give more money to the government because it was making bigger profits.

Another attempt to encourage industrial growth was the Fordney–McCumber Tariff of 1922. This placed a tax or tariff on goods imported into the US. The idea was that, by making foreign goods more expensive, US consumers would buy American goods and boost American businesses.

Examiner Tips and Tricks

Many of the factors that led the American economic boom in the 1920s are connected to each other. It is important that you are able to explain how developments such as mass production led to increased consumer confidence, which increased wealth and led to more sales of consumer goods etc. Remember, none of these developments occurred in isolation from each other, but they combined to create the boom.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?