Factors of Production (SQA National 5 Business Management): Revision Note

Exam code: X810 75

Capital, enterprise, land and labour

Factors of production are the resources used to produce goods and services

They include land, labour, capital and enterprise

The production of any good or service requires the use of a combination of all four factors of production

Goods are physical objects that can be touched (tangible), e.g., a mobile phone

Services are actions or activities that one person performs for another (intangible), e.g., a manicure or car wash

An explanation of the four factors of production

Land | Capital |

|---|---|

|

|

Labour | Enterprise |

|

|

Adding value

Adding value is the process of taking raw materials and using them in such a way that the end product created is worth more than the cost to make it

It is therefore the difference between the price charged to the customer and the cost of inputs required to create the product or service

For example, customers are prepared to pay more for frozen oven chips than they would be willing to pay for a bag of potatoes

The greater the added value, the more successful the business is likely to be and the higher their profits

Product and marketing teams explore ways to increase added value

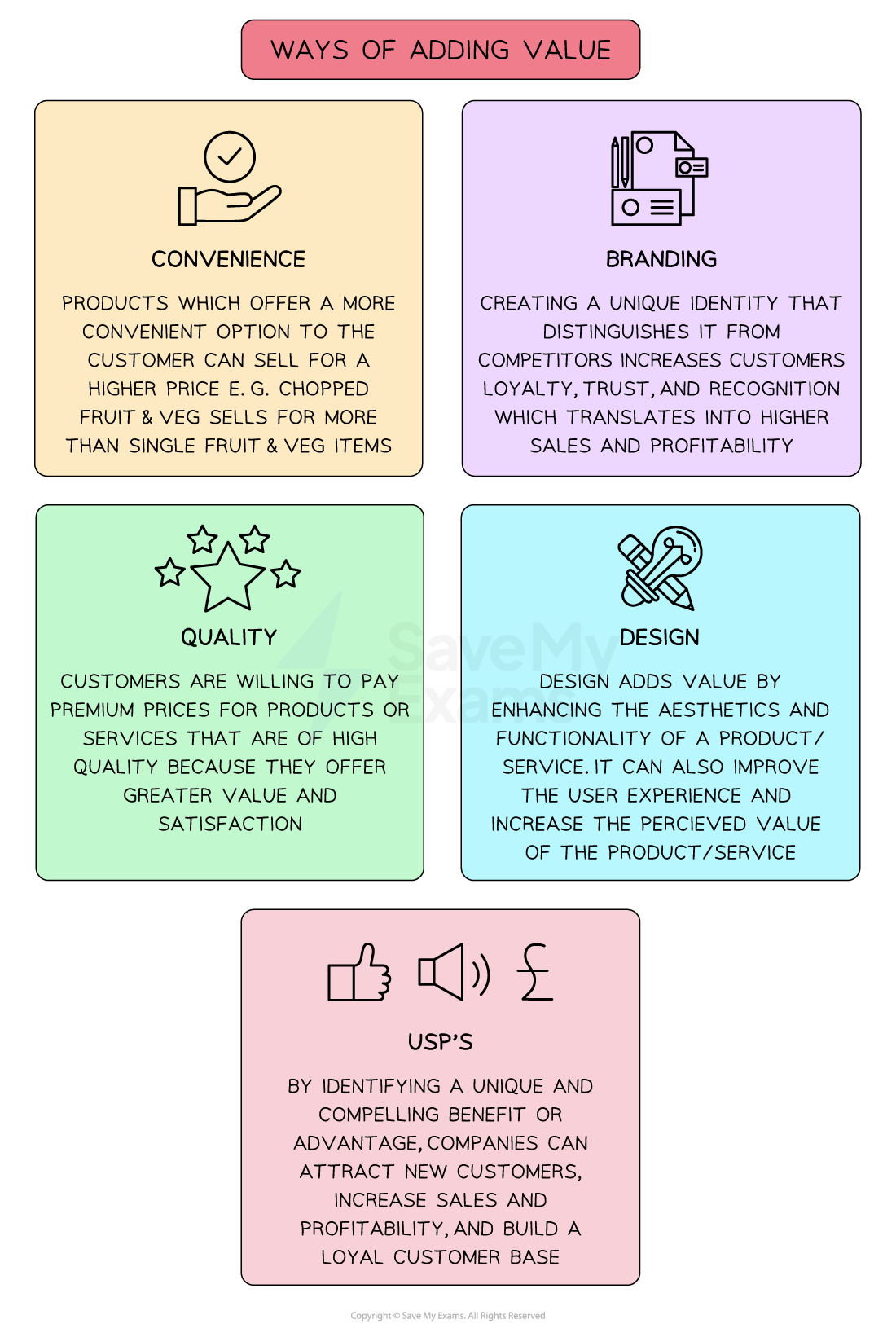

Examples of added value

Method | Example |

|---|---|

Branding |

|

Convenience |

|

Quality |

|

Unique selling points (USPs) |

|

Design |

|

Examiner Tips and Tricks

Don’t confuse adding value with profit – adding value is the difference between the cost of inputs and the selling price, whereas profit is what remains after all business costs have been paid

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?