Schedule of Non-current Assets (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

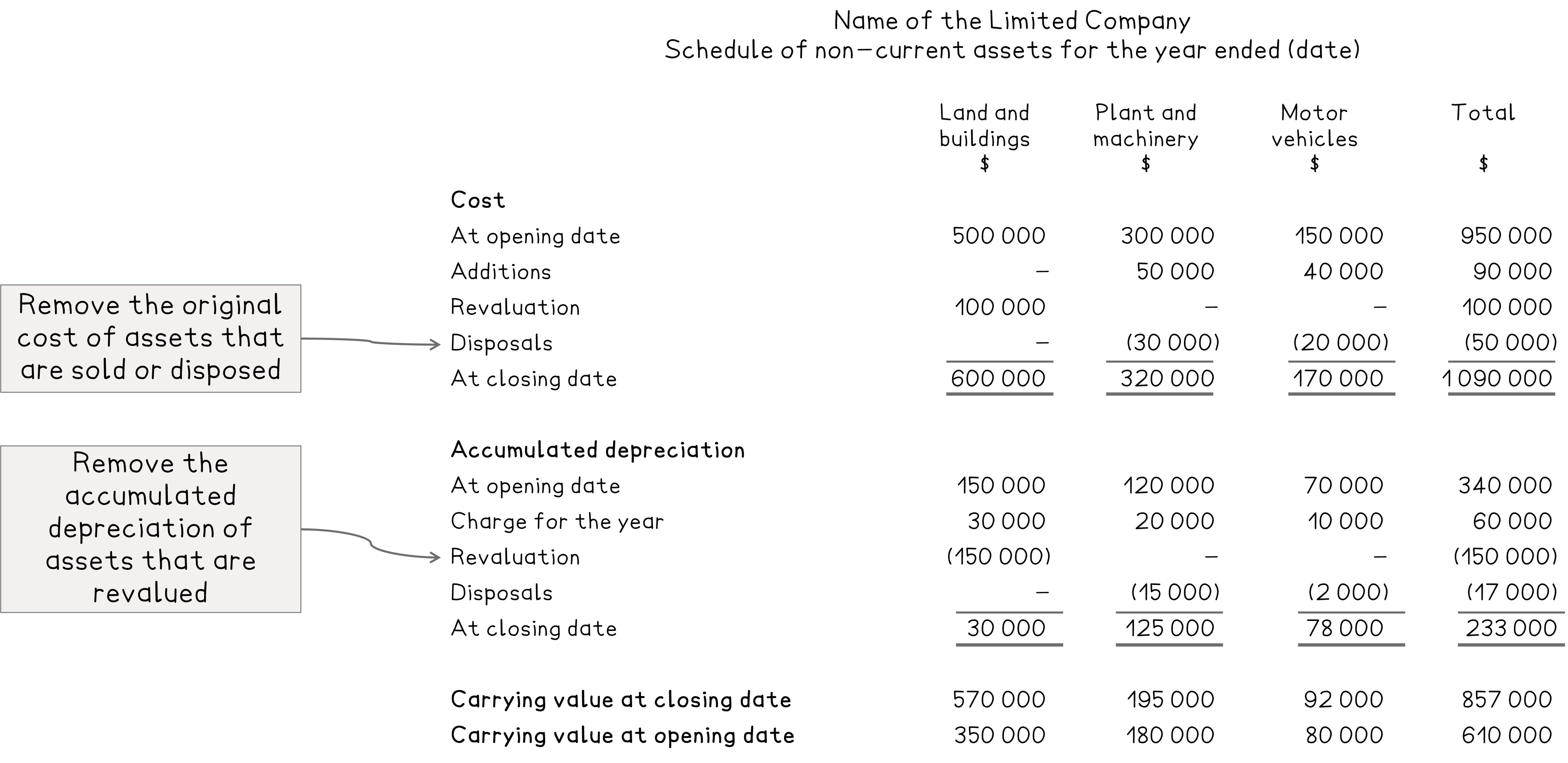

Schedule of non-current assets

What is a schedule of non-current assets?

A schedule of non-current assets is a note to the statement of financial position

It is required under IAS 16

It shows the movement in cost or valuation and accumulated depreciation for each class of non-current asset

It has a column for each class of non-current asset and a column for the total

Classes include: land and buildings, plant and machinery, motor vehicles, etc

How do I prepare a schedule of non-current assets?

Cost section

Start with the balances at the start of the year

Add any additions or acquisitions

These are the non-current assets that the business has gained during the year

Subtract any disposals

Add or subtract any amounts due to revaluations

This gives you the balances at the end of the year

Accumulated depreciation section

Start with the balances at the start of the year

Add the depreciation charge for the year

Check whether assets sold or purchased during the year are charged depreciation

Subtract the accumulated depreciation for disposed assets

Subtract the accumulated depreciation for revalued assets

This gives you the balances at the end of the year

Carrying value section

State the carrying values at the start of the year

State the carrying values at the end of the year

They should equal the closing balances for the cost minus the closing balances for the accumulated depreciation

Actions for each transaction

Event | Cost section | Accumulated depreciation section |

|---|---|---|

Addition (purchase) | Add the cost | No entry |

Disposal | Deduct the original cost | Deduct the accumulated depreciation |

Revaluation (upward) | Add the increase in value | Deduct any existing accumulated depreciation |

Revaluation (downward) | Deduct the decrease in value | Deduct any existing accumulated depreciation |

Depreciation charge for the year | No entry | Add the charge for the year |

Examiner Tips and Tricks

When an asset is revalued, the existing accumulated depreciation on that asset is eliminated (deducted) from the accumulated depreciation section. After revaluation, the asset sits at its new fair value with a clean slate of zero accumulated depreciation.

Worked Example

The cost section and accumulated depreciation section of Omega plc’s schedule of non-current assets at 31 December 2024 are as follows:

Land and buildings $ | Plant and machinery $ | Motor vehicles $ | |

|---|---|---|---|

Cost | |||

At 1 January 2024 | 300 000 | 210 000 | 140 000 |

Additions | 100 000 | 40 000 | - |

At 31 December 2024 | 400 000 | 250 000 | 140 000 |

Accumulated depreciation | |||

At 1 January 2024 | 70 000 | 85 000 | 56 000 |

Charge for the year | 10 000 | 33 000 | 28 000 |

At 31 December 2024 | 80 000 | 118 000 | 84 000 |

The following information has been provided for the year ended 31 December 2025:

The 'Land and buildings' balance at 31 December 2024 consists of Land costing $200 000 and Buildings costing $200 000. On 1 January 2025, the directors decided to revalue the land upwards to $290 000.

On 1 April 2025, a new machine was purchased at a cost of $55 000.

During the year, a motor vehicle which had originally cost $30 000 was sold for $11 000. There was a $1 000 loss on disposal.

The company's depreciation policy is as follows:

Land: No depreciation is charged.

Buildings: 5% per annum using the straight-line method.

Plant and machinery: 20% per annum using the reducing balance method.

Motor vehicles: 20% per annum using the straight-line method.

A full year's depreciation is provided in the year of acquisition and none is provided in the year of disposal.

Prepare the schedule of non-current assets for Omega plc for the year ended 31 December 2025, suitable for use as a note to the financial statements.

Answer:

Calculate the carrying values at 31 December 2024

Land and buildings $ | Plant and machinery $ | Motor vehicles $ | |

|---|---|---|---|

Cost | 400 000 | 250 000 | 140 000 |

Accumulated depreciation | 80 000 | 118 000 | 84 000 |

Carry value | 320 000 | 132 000 | 56 000 |

Calculate the increase in the value of the land due to the revaluation

$290 000 - $200 000 = $90 000

Calculate the accumulated depreciation of the sold vehicle

Calculate the net book value by adding the loss to the sale proceeds

$11 000 + $1 000 = $12 000

Subtract this from the original cost

$30 000 - $12 000 = $18 000

Calculate the depreciation charge for the year

Buildings

5% × $200 000 = $10 000

Plant and machinery

Add the purchase price to the carrying value from the start of the year

20% × ($132 000 + $55 000) = $37 400

Motor vehicles

Subtract the cost of the sold vehicle

20% × ($140 000 - $30 000) = $22 000

Omega plc

Schedule of Non-Current Assets for the year ended 31 December 2025

Land and buildings $ | Plant and machinery $ | Motor vehicles $ | Total $ | |

|---|---|---|---|---|

Cost or Valuation | ||||

At 1 January 2025 | 400 000 | 250 000 | 140 000 | 790 000 |

Revaluation | 90 000 | - | - | 90 000 |

Additions | - | 55 000 | - | 55 000 |

Disposals | - | - | (30 000) | (30 000) |

At 31 December 2025 | 490 000 | 305 000 | 110 000 | 905 000 |

Accumulated Depreciation | ||||

At 1 January 2025 | 80 000 | 118 000 | 84 000 | 282 000 |

Charge for the year | 10 000 | 37 400 | 22 000 | 69 400 |

Disposals | - | - | (18 000) | (18 000) |

At 31 December 2025 | 90 000 | 155 400 | 88 000 | 333 400 |

Carrying Amount | ||||

At 31 December 2025 | 400 000 | 149 600 | 22 000 | 571 600 |

At 31 December 2024 | 320 000 | 132 000 | 56 000 | 508 000 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?