Statement of Cash Flows (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

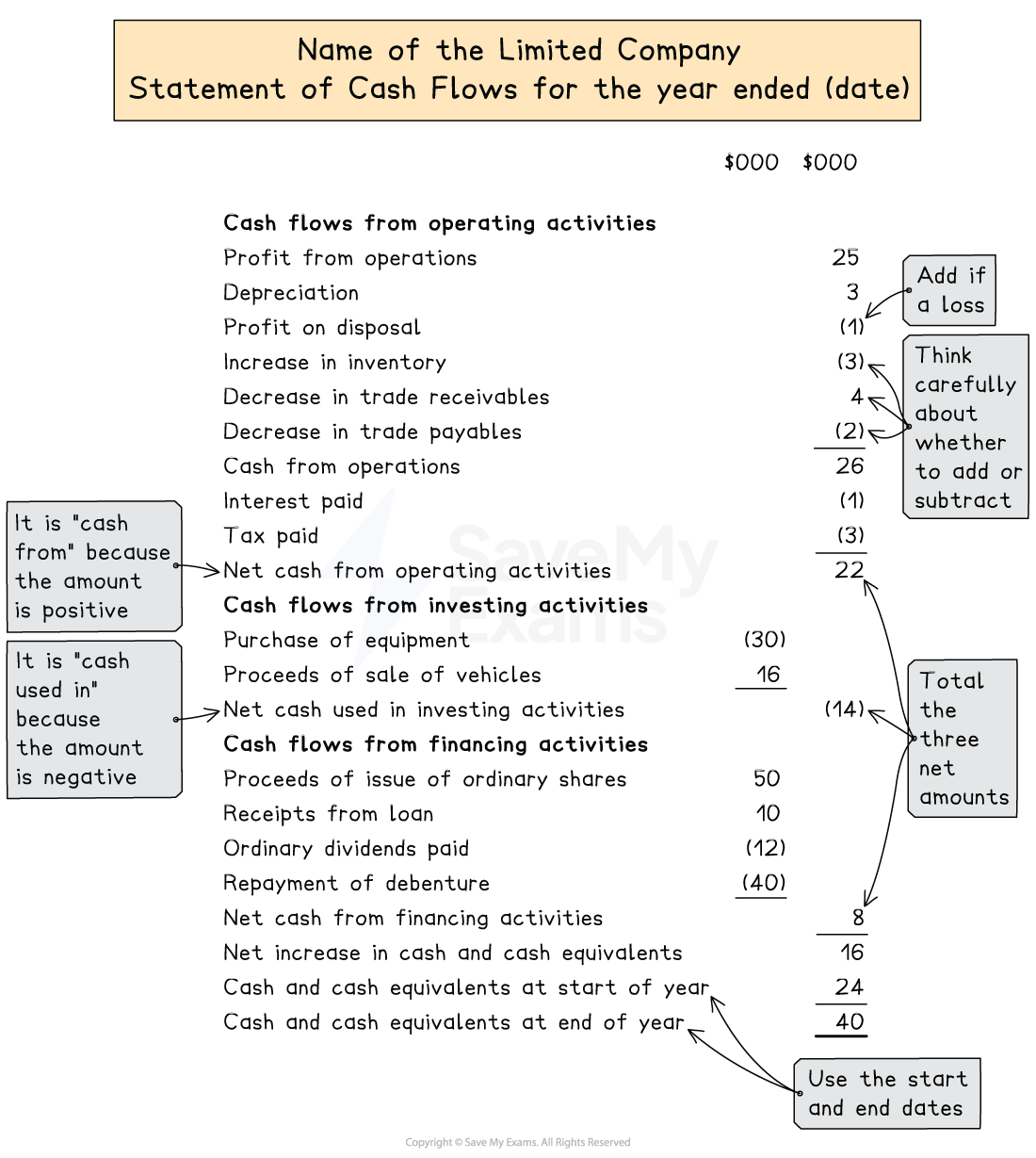

Statements of cash flows

What is a statement of cash flows?

A statement of cash flows shows the movement of cash and cash equivalents during the year

It separates the cash flows into three sections to show the cash from or used in these activities

Cash flows from operating activities

Cash flows from investing activities

Cash flows from financing activities

What are the uses of a statement of cash flows?

To show the amount of money that has entered and left the business during a period

To show why the profit for a period is different to the increase in cash

To show sources of finance during a period

To enable the directors to assess the liquidity of the business

To enable stakeholders to see how well cash has been used

To enable stakeholders to compare the year's cash flow with previous years or with other businesses

How do I prepare a statement of cash flows?

Cash flows from operating activities

Start with the profit from operations

This is the profit before loan interest and tax

Make adjustments for non-cash items included in the calculation for the profit

Add the depreciation charge for the year

Add the loss on disposal of non-current assets

Subtract the profit on disposal of non-current assets

Make adjustments for changes in working capital

Change in inventories

Add if it is a decrease

Subtract if it is an increase

Change in trade receivables

Add if it is a decrease

Subtract if it is an increase

Change in trade payables

Add if it is an increase

Subtract if it is a decrease

This gives the cash from or used in operations

It is cash from operations if it is a positive value

It is cash used in operations if it is a negative value

Subtract the actual amount paid for interest and tax

This gives the net cash from or used in operating activities

Examiner Tips and Tricks

It can be helpful to understand why changes to assets and liabilities are added or subtracted from the cash flows from operating activities.

A decrease to an asset is added to the cash flow because a part of its balance at the beginning of the year has been converted to cash. Whereas, a decrease to a liability is subtracted from the cash flow because the company has paid some of the balance off.

Cash flows from investing activities

Add the sale proceeds from the disposals of non-current assets

Subtract the purchase amounts of non-current assets

The net amount is the net cash from or used in investing activities

It is usually net cash used in investing activities

Cash flows from financing activities

Add the amounts raised to finance the company

Issue of share capital

Money from new debentures or loans

Subtract the amounts paid to investors, lenders and shareholders

Repayment of debentures or loans

Dividends paid

The net amount is the net cash from or used in financing activities

Examiner Tips and Tricks

A bonus issue raises no cash, so it is excluded from the cash flow statement. A rights issue raises cash, so the full amount received (nominal value + share premium) appears as a cash inflow under financing activities.

How do I calculate the profit from operations?

You might be given the profit from operations in the question or you might be required to calculate it

You can calculate the profit or the loss for the year by looking at the change in equity

Calculate the change in retained earnings

Add back the dividends paid

Add back any amounts of retained earnings that were transferred or used in a bonus issue of shares

You can then work backwards from the profit or loss to find the profit from operations

Add back the amount due for finance costs for the year

Add back the amount due for taxation for the year

Examiner Tips and Tricks

The amounts due for interest and tax might not be the amounts that were actually paid. The amounts due are used to calculate the profit from operations. The amounts paid are used to calculate the net cash from operating activities.

Worked Example

W plc's financial year ends on 31 December.

The following information for the year ended 31 December 2025 is available.

The following balances are given.

1 January 2025 $ | 31 December 2025 $ | |

|---|---|---|

Inventory | 29 000 | 21 000 |

Trade receivables | 32 000 | 33 000 |

Trade payables | 27 000 | 30 000 |

Cash and cash equivalents | 11 000 | 17 000 |

Accrued loan interest | - | 1 000 |

Ordinary share capital | 100 000 | 120 000 |

Share premium | 10 000 | 20 000 |

Retained earnings | 30 000 | 34 000 |

Debentures | 20 000 | 20 000 |

The following balances were on 1 January 2025.

$ | |

|---|---|

Non-current assets at cost | 200 000 |

Provision for depreciation | 85 000 |

Office equipment costing $25 000 was sold for $7 000. It had a carrying value of $10 000 at the point of sale. New office equipment was purchased for $105 000. Non-current assets are depreciated at 20% per annum using the straight-line method. A full year's depreciation is charged in the year of purchase but none is charged in the year of disposal.

There was a rights issue of shares during the year.

Loan interest, $1 000, was paid.

Taxation, $2 000, was paid.

Dividends, $12 000, were paid.

(a) Calculate the profit for the year 2025.

(b) Prepare the statement of cash flows for the year ended 31 December 2025.

Answer:

(a)

Calculate the profit

Find the increase in the retained earnings

Add the dividends paid

$ | |

|---|---|

Retained earnings at 31 December 2025 | 34 000 |

Retained earnings at 1 January 2025 | (30 000) |

Dividends paid | 12 000 |

Profit for the year | 16 000 |

Profit for the year was $16 000

(b)

Calculate the loan interest that was due

Add the amount paid to the amount that is still accrued

$1 000 + $1 000 = $2 000

Calculate the profit from operations

$ | |

|---|---|

Profit for the year | 16 000 |

Add: Loan interest | 2 000 |

Add: Tax | 2 000 |

Profit from operations | 20 000 |

Calculate the depreciation charge for the year

Find the total cost of the non-current assets at the end of the year

$200 000 - $25 000 + $105 000 = $280 000

Find 20% of this amount

20% × $280 000 = $56 000

Calculate the loss on sale of equipment

$10 000 - $7 000 = $3 000

Calculate the amount received from the rights issue

Subtract the old share capital from the new share capital

($120 000 + $20 000) - ($100 000 + $10 000) = $30 000

Calculate the change in inventory, trade receivables and trade payables

$ | |||

|---|---|---|---|

Inventory | 29 000 - 21 000 | 8 000 | Decrease |

Trade receivables | 33 000 - 32 000 | 1 000 | Increase |

Trade payables | 30 000 - 27 000 | 3 000 | Increase |

Prepare the statement of cash flows

$000 | $000 | |

|---|---|---|

Cash flows from operating activities | ||

Profit from operations | 20 | |

Depreciation | 56 | |

Loss on sale of equipment | 3 | |

Decrease in inventory | 8 | |

Increase in trade receivables | (1) | |

Increase in trade payables | 3 | |

Cash from operations | 89 | |

Interest paid | (1) | |

Tax paid | (2) | |

Net cash from operating activities | 86 | |

Cash flows from investing activities | ||

Purchase of equipment | (105) | |

Proceeds of sale of equipment | 7 | |

Net cash used in investing activities | (98) | |

Cash flows from financing activities | ||

Proceeds of rights issue of ordinary shares | 30 | |

Dividends paid | (12) | |

Net cash from financing activities | 18 | |

Net increase in cash and cash equivalents | 6 | |

Cash and cash equivalents at 1 January 2025 | 11 | |

Cash and cash equivalents at 31 December 2025 | 17 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?