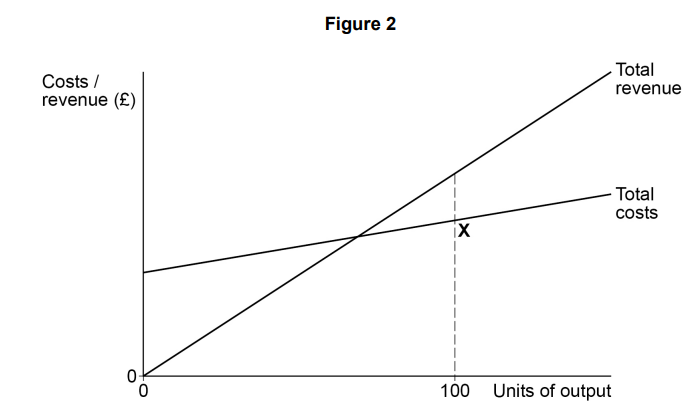

Biggs Ltd

Biggs Ltd operates in the snack food market, selling crisps, nuts and other savoury products. Potatoes are a key ingredient in its snacks. The price of potatoes has risen by 35% over the last two years.

The company is one of six firms who dominate a market that has been growing strongly for ten years. The market growth is largely due to the development of new snacks designed for children. However, Biggs Ltd’s market share has been falling since 2019.

Biggs Ltd plans to launch a completely new range of products in 2024. It will promote this by sponsoring a major televised sporting competition which has children and families as its audience.

Appendix A Extract from Biggs Ltd’s recent financial statements

| 2023

£000s | 2022

£000s |

Revenue | 47 569 | 46 994 |

Gross profit | 22 289 | 22 820 |

Operating profit | 4 650 | 4 701 |

Payables | 5 056 | 5 221 |

Appendix B Labour productivity for Biggs Ltd and the snack food industry average (shown as an index number, base year = 2017)

Year | Biggs Ltd | Industry average |

2020 | 104.2 | 104.3 |

2023 | 100.3 | 105.9 |

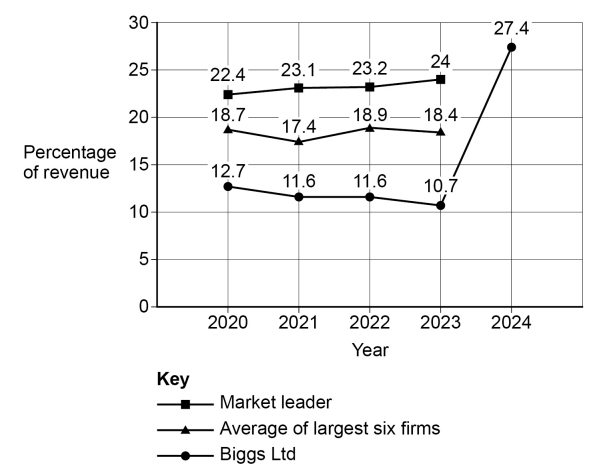

Appendix C Marketing expenditure as a percentage of revenue, 2020–2024*

* 2024 based on Biggs Ltd’s forecast.

Appendix D Results of market research conducted with families on Biggs Ltd’s new product range and the promotional campaign

Survey question | Average survey score by age group |

6 to 16 years | 17 to 35 years | 36 years and over |

I will definitely try the new products when they are available. | 9.9 | 7.2 | 1.8 |

The promotional campaign improves my view of Biggs Ltd’s brand. | 8.3 | 6.3 | 8.0 |

I frequently consume snack foods at sports events. | 8.9 | 6.9 | 2.7 |

Scale: 10 = strongly agree, 5 = neither agree nor disagree, 0 = strongly disagree |

Source: Data from 27 interviews with families, conducted by Biggs Ltd in 2021.

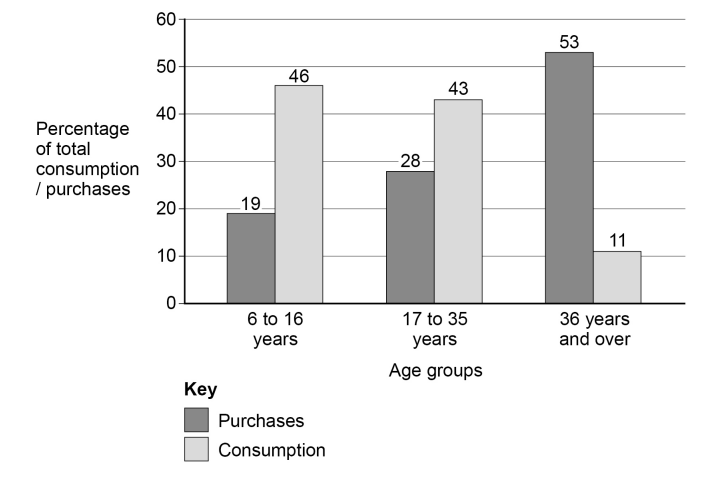

Appendix E Percentage of snack products bought and consumed by different box age groups

Results from a recent survey of 3000 respondents conducted by an independent market research firm.