Redistributive Policies (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

Redistribution policies

Governments use redistribution policies to reduce inequality and improve equity by transferring income or resources from higher-income to lower-income groups

The central evaluative tension for every policy is the equity-efficiency trade-off: does the policy improve fairness, and at what cost to productive and dynamic efficiency?

There are four key policies to consider: means-tested benefits, universal benefits, negative income tax and universal basic income

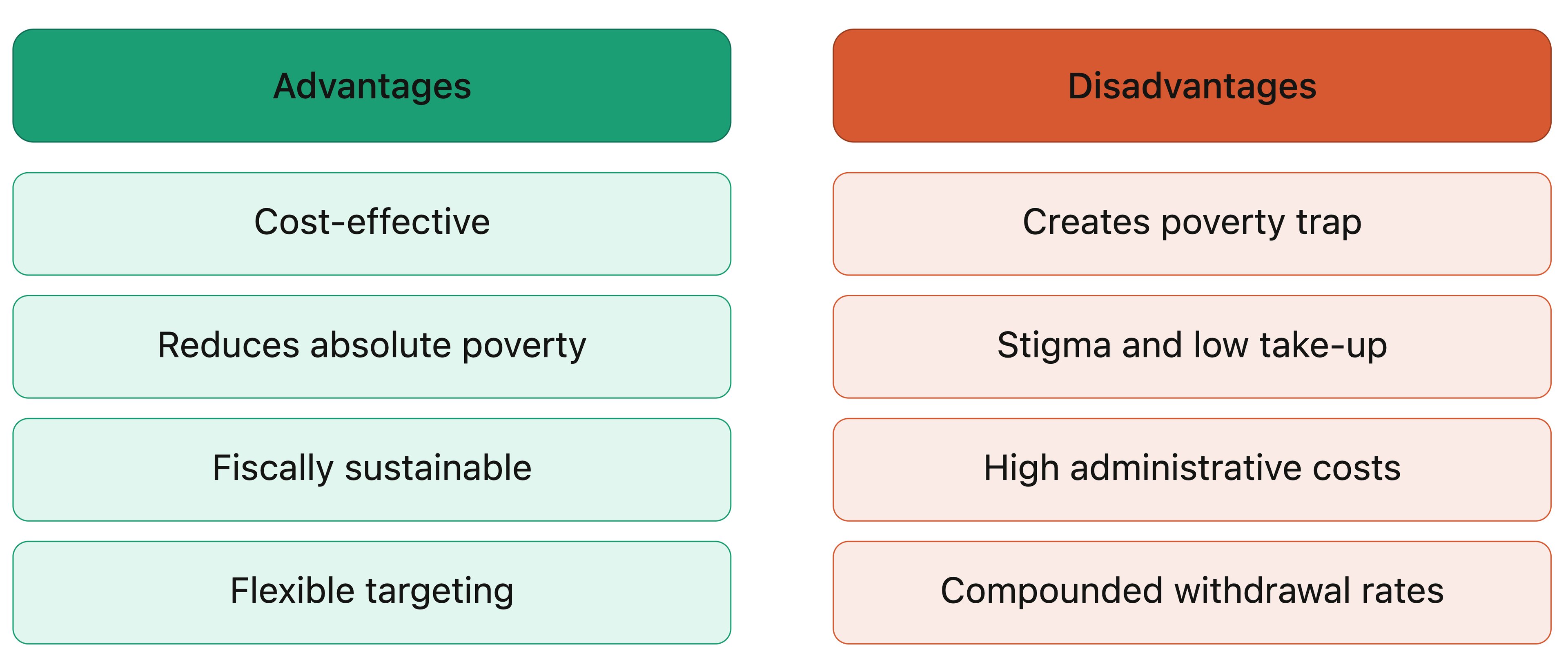

1. Means-tested benefits

These are benefits paid only to individuals whose income and/or wealth falls below a specified threshold - recipients must demonstrate financial need to qualify

The government targets support at those who need it most, making this approach cost-effective relative to universal provision

Examples include housing benefit, food assistance, unemployment support and healthcare subsidies for low-income households

Evaluating means-tested benefits

Advantages | Disadvantages |

|---|---|

|

|

|

|

|

|

|

|

Case Study

Universal Credit in the United Kingdom

The context

The UK's legacy benefit system consisted of six separate means-tested benefits including housing benefit, tax credits and income support

Each had different withdrawal rates and eligibility rules, creating a complex system where some low-income workers faced effective marginal tax rates (EMTR) above 90% - a severe poverty trap discouraging progression into work

Actions taken

Universal Credit (UC) was introduced from 2013, merging six benefits into a single payment with a unified taper rate of 55p withdrawn per £1 of earned income

The policy aimed to make work always pay by ensuring the EMTR never exceeded 55% - significantly below the rates in the legacy system

By 2023, approximately 6 million households were receiving Universal Credit

Outcomes

Evidence suggests UC improved work incentives at the margin compared to the legacy system

The unified taper rate reduced the most extreme poverty trap cases

However critics argue a 55% taper rate remains high, and that the interaction with childcare costs pushes effective marginal tax rates above 70% for many families

The five-week wait for first payment also pushed many new claimants into debt, illustrating that poorly designed implementation can undermine a well-intentioned policy - a form of government failure

2. Universal benefits

These are benefits paid to all individuals in a category regardless of income or wealth - no means test is applied

Examples include universal child benefit, state pensions paid to all retirees, and universal healthcare

The defining feature is that entitlement is based on status (being a child, being retired, being a citizen) rather than financial need

Evaluating universal benefits

Advantages | Disadvantages |

|---|---|

|

|

|

|

|

|

|

|

3. Negative income tax

This is a system in which the tax and benefit systems are merged

Individuals above a specified income threshold pay tax in the normal way, while those below it receive a government payment (the negative tax) rather than paying tax

Proposed by economist Milton Friedman as a way to eliminate the poverty trap while maintaining work incentives

The mechanism:

A break-even income is set - above this level individuals pay tax; below it they receive payments

As earned income rises towards the break-even point, the negative tax payment falls at a constant taper rate

Because the taper rate is consistent and moderate, the EMTR never becomes prohibitively high - work always pays at the margin

This replaces the complex array of means-tested benefits with a single, streamlined system

Evaluating negative income tax

Advantages | Disadvantages |

|---|---|

|

|

|

|

|

|

|

|

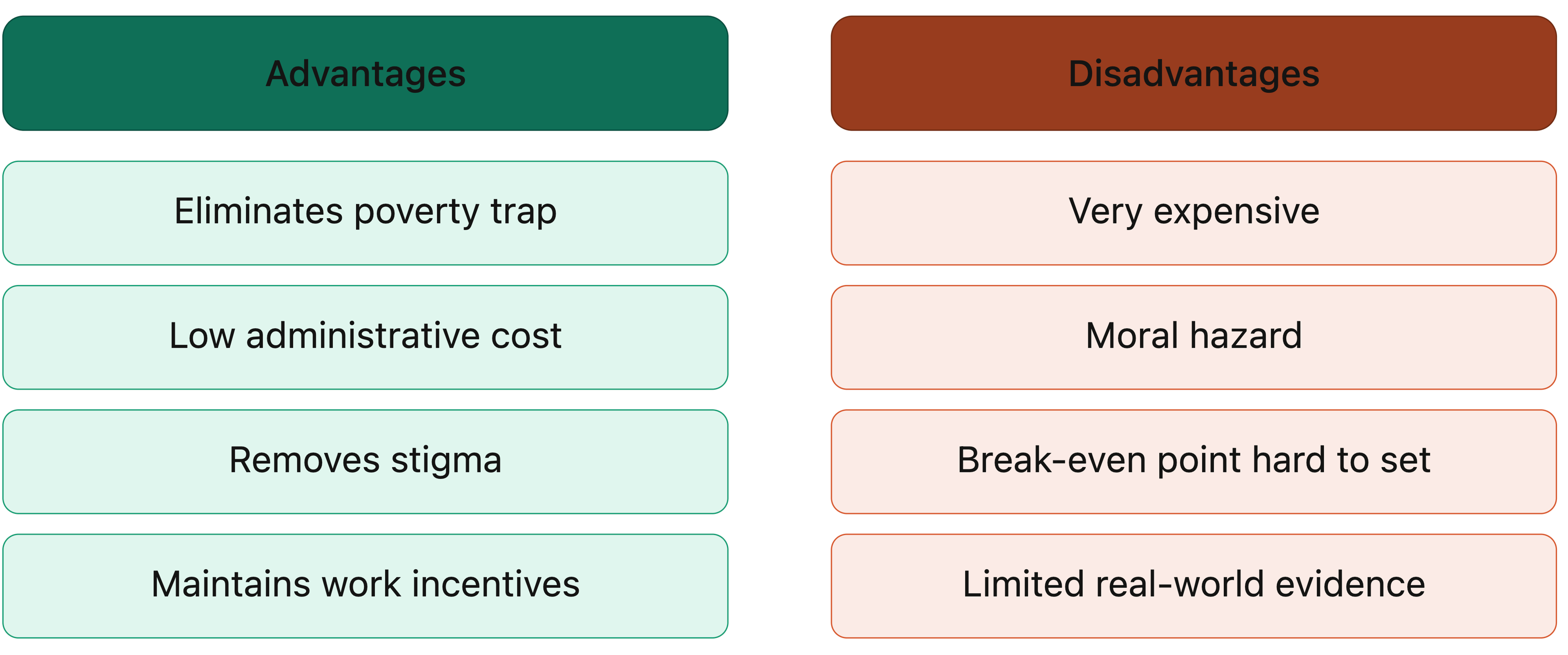

4. Universal basic income

Universal basic income (UBI) a regular, unconditional cash payment made to every citizen regardless of income, employment status or need

Unlike negative income tax, UBI is paid to everyone, not just those below a threshold

Unlike means-tested benefits, it is never withdrawn as income rises, eliminating the poverty trap entirely

UBI has gained significant policy attention as a potential response to technological unemployment and the gig economy

Evaluating universal basic income

Advantages | Disadvantages |

|---|---|

|

|

|

|

|

|

|

|

|

|

Case Study

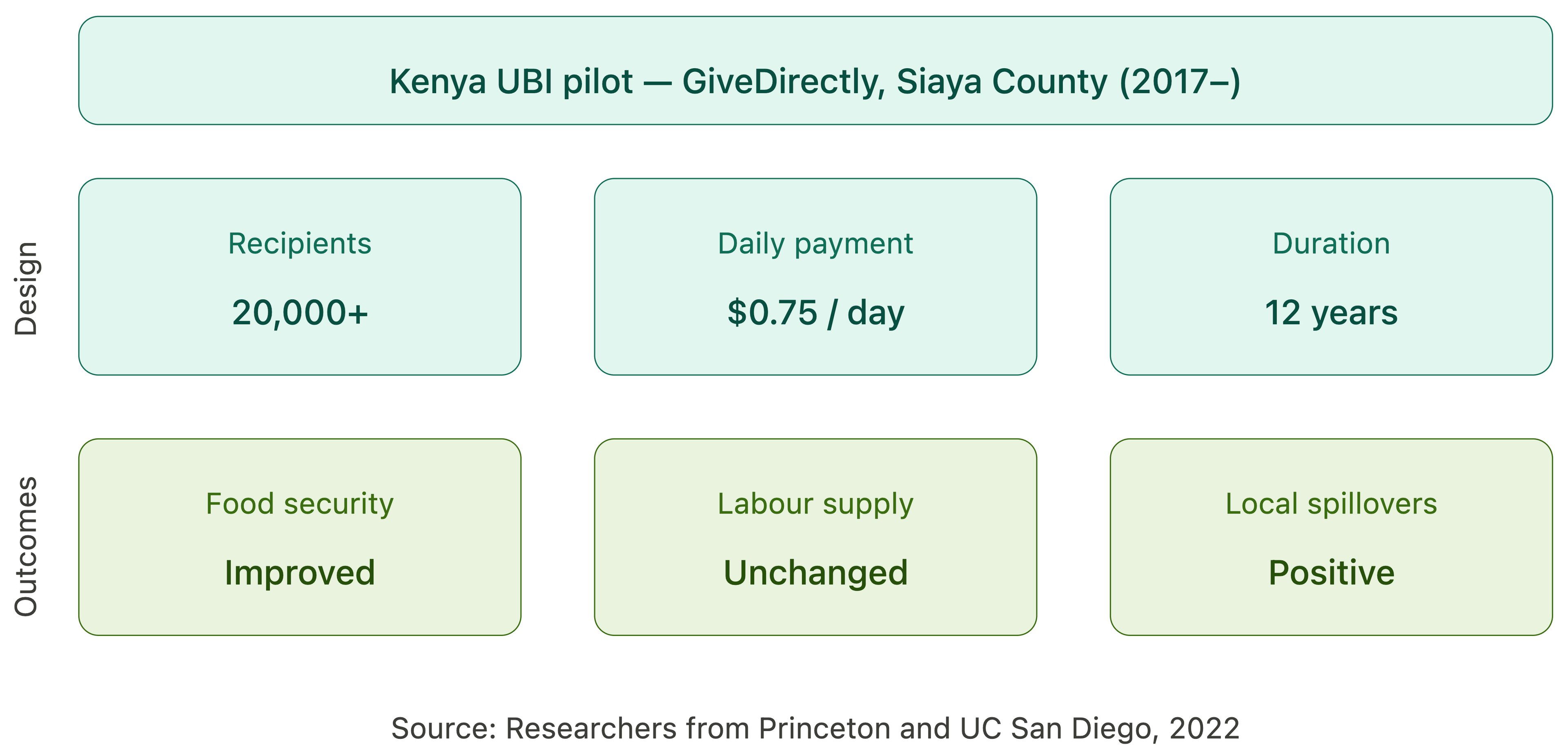

Universal basic income pilot in Kenya

The context

Kenya has high levels of both absolute and relative poverty, with significant rural populations engaged in subsistence agriculture and informal work

GiveDirectly, an NGO working with the Kenyan government, launched the world's largest and longest-running UBI experiment in 2017, providing unconditional cash transfers to over 20,000 recipients in rural villages in Siaya County

Actions taken

Long-term recipients received approximately $0.75 per day - roughly 75% of the average consumption level in recipient villages - for a guaranteed period of 12 years

Short-term recipients received the same total amount as a lump sum over two years

A control group of villages received no payments, allowing rigorous comparison of outcomes

Outcomes

Early results published by researchers from Princeton and UC San Diego found significant positive effects

Recipient households increased assets, food security and psychological wellbeing

There was evidence of positive spillover effects to non-recipient households in the same villages through increased local economic activity

Crucially, there was no significant reduction in labour supply - recipients worked as much as control group households, challenging the moral hazard concern

However critics note that a donor-funded pilot with a guaranteed end date cannot replicate the fiscal and behavioural dynamics of a permanent government-funded UBI at national scale

Comparing the four policies

Policy | Poverty trap? | Targets the poorest? | Administrative cost | Fiscal cost |

|---|---|---|---|---|

Means-tested benefits |

|

|

|

|

Universal benefits |

|

|

|

|

Negative income tax |

|

|

|

|

Universal basic income |

|

|

|

|

Examiner Tips and Tricks

The poverty trap is the central weakness of means-tested benefits - benefit withdrawal combined with income tax creates a high EMTR, so work does not pay at the margin.

NIT and UBI both solve the poverty trap but at significant fiscal cost - the key distinction is that NIT targets those below a threshold; UBI is paid to everyone.

Structure evaluation using the equity-efficiency trade-off: means-tested benefits are fiscally efficient but damage work incentives; UBI preserves incentives but is poorly targeted and very expensive.

The Kenya pilot challenges the moral hazard assumption - but pilot evidence may not generalise to permanent national-scale implementation.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?