Cash Budgets (Cambridge (CIE) A Level Accounting): Revision Note

Exam code: 9706

Cash budgets

How to prepare a cash budget?

The cash budget shows all the projected money coming in and going out

The cash budget includes all transactions relating to cash, cheque and bank transactions

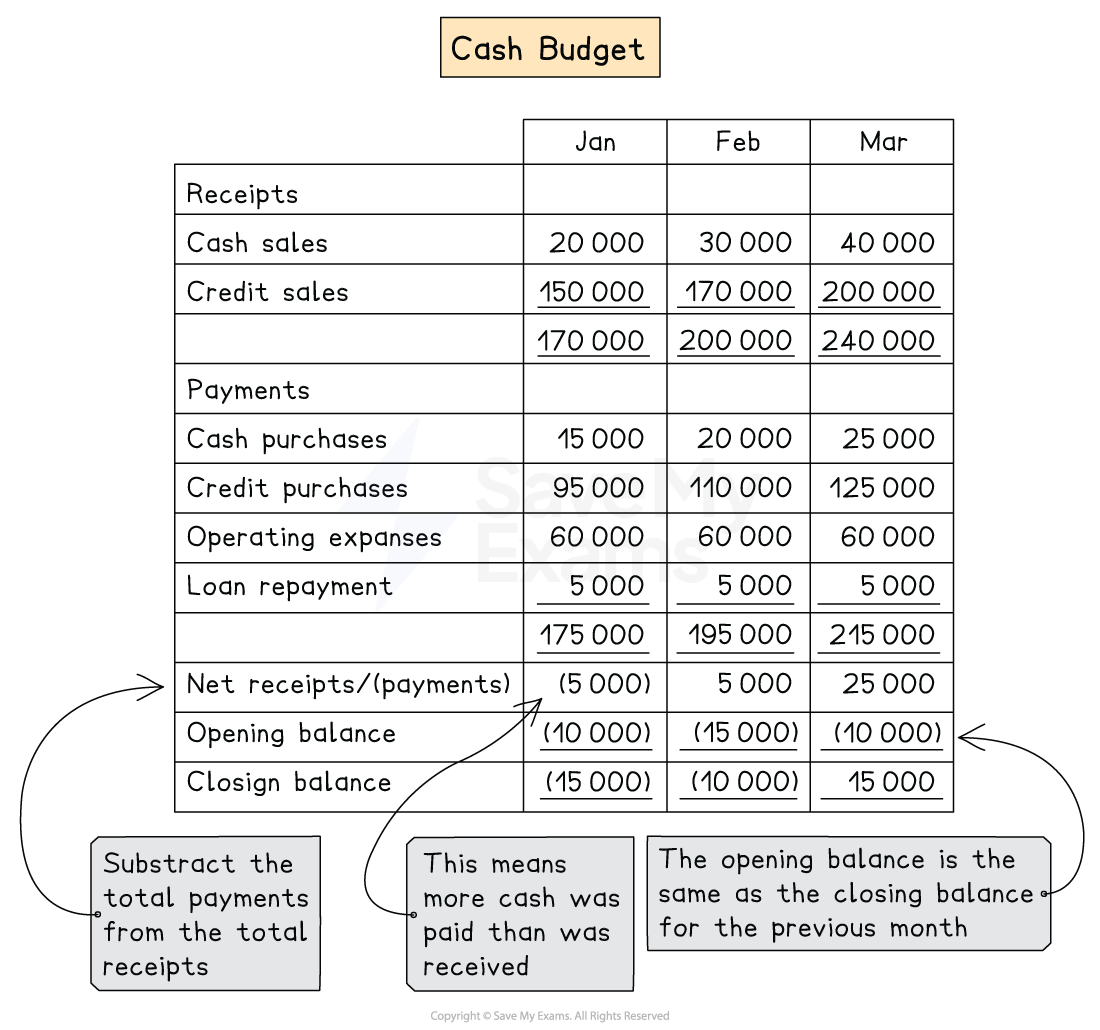

Here is an example of the cash budget

STEP 1

Calculate the receipts for each periodThis may include:

Receipts of cash sales

Receipts from credit sales

Sale of non-current assets

Capital

Loans

STEP 2

Calculate the payments for each periodThis may include:

Payment of cash purchases

Payments for credit purchases

Purchase of non-current assets

Drawings

Loan repayments

Cash expenses only

STEP 3

Calculate the net receipts or payments by using this formulaTotal receipts - total payments

STEP 4

Write down the opening balanceThis is the same as the closing balance for the previous month

Brackets indicate that the bank is overdrawn

STEP 5

Find the closing balanceAdd the net cash flow to the opening balance

Examiner Tips and Tricks

If depreciation is included in the expenses, then you need to subtract it from the total. Depreciation does not affect the cash budget.

Worked Example

Cushions manufacture a range of cushions. Here is the following information relating to a cash budget:

January | February | March | |

|---|---|---|---|

Sales $ | 60 000 | 58 000 | 66 000 |

Purchases $ | 30 000 | 28 000 | 31 000 |

Expenses (including depreciation) | 15 000 | 12 000 | 12 000 |

Additional information

40% of sales are made on cash basis. The remaining 60% of customers will pay one month later. Sales in December are expected to be $40 000.

Payments to suppliers are made one month later. The purchases expected in December is to be $20 000.

Expenses are paid in the month they are incurred.

The opening balance in January is expected to be $3 000 overdrawn.

Depreciation for existing non-current assets for the year is $12 000.

In February a new van was purchased for $17 000. The policy is that vehicles are not depreciated in the year of purchase.

Loan repayments will be $1 500 each month starting in February

Prepare the cash budget for January, February and March

Answer

Calculate the receipts for all three months

Sales:

January

Cash sales = 40% × $60 000 = $24 000

Credit sales = 60% × $40 000 = $24 000

February

Cash sales = 40% × $58 000 = $23 200

Credit sales = 60% × $60 000 = $36 000

March

Cash sales = 40% × $66 000 = $26 400

Credit sales = 60% × $58 000 = $34 800

Calculate the payments for all three months

Purchases

January = $20 000

February = $30 000

March = $28 000Expenses

Depreciation for the month = $12 000 ÷ 12 = $1 000 per month

January = $15 000 - $1 000 = $14 000

February = $12 000 - $1 000 = $11 000

March = $12 000 - $1 000 = $11 000

The answer will be presented as the following cash budget:

January $ | February $ | March $ | |

|---|---|---|---|

Receipts | |||

Cash sales | 24 000 | 23 200 | 26 400 |

Credit customer - one month | 24 000 | 36 000 | 34 800 |

Total receipts | 48 000 | 59 200 | 61 200 |

Payments | |||

Credit suppliers - one month | 20 000 | 30 000 | 28 000 |

Expenses | 14 000 | 11 000 | 11 000 |

Van | 17 000 | ||

Loan repayment |

| 1 500 | 1 500 |

Total Payments | 34 000 | 59 500 | 40 500 |

Net receipts or payments | 14 000 | (300) | 20 700 |

Opening balance | (3 000) | 11 000 | 10 700 |

Closing balance | 11 000 | 10 700 | 31 400 |

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?