1

4 marks

Read the following extracts (E to H) (opens in a new tab) before answering

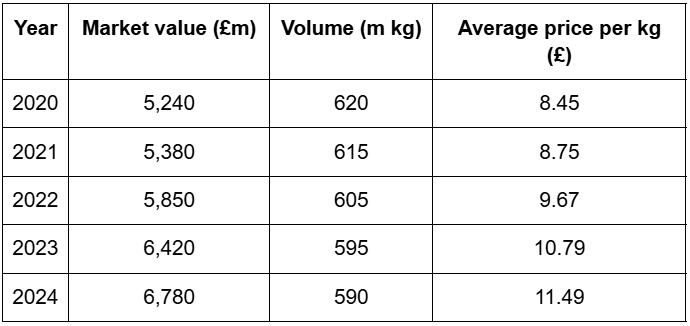

Using the data in Extract F, explain one implication of the level of capacity utilisation for the soft drinks manufacturer A, compared to B. You are advised to show your working

Was this exam question helpful?