The Phillips Curve (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

The Phillips curve and the inflation-unemployment relationship

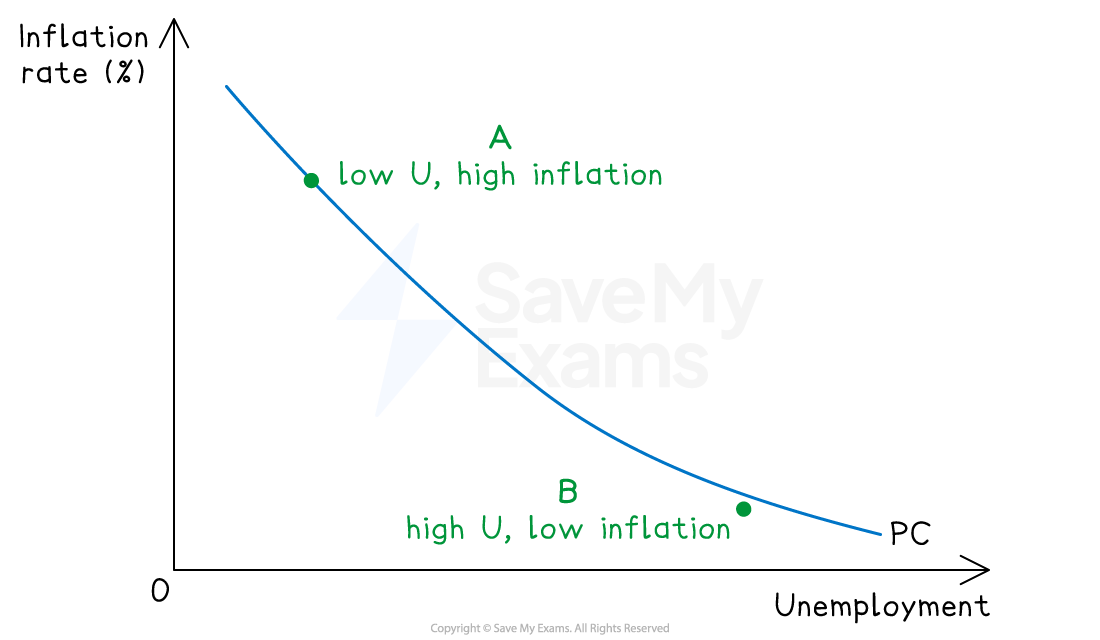

The Phillips curve describes the observed relationship between unemployment and inflation

The traditional version showed a stable inverse trade-off

The expectations-augmented version, developed after the 1970s, distinguishes a short-run trade-off from a vertical long-run curve at the natural rate of unemployment (NAIRU)

The traditional Phillips curve

The traditional Phillips curve, based on A.W. Phillips's 1958 study of UK data from 1861 to 1957, describes a stable inverse relationship between the rate of unemployment and the rate of wage inflation, later extended to price inflation

How does it work?

When unemployment is low, labour markets are tight - employers compete for scarce workers, bidding up wages

Higher wages feed into higher prices as firms pass on cost increases - inflation rises

When unemployment is high, the opposite occurs - workers compete for scarce jobs, wages stagnate, and inflation falls

The result is a downward-sloping curve relating inflation to unemployment

Implications for policy

Policymakers face a stable trade-off between inflation and unemployment

Choosing a point on the curve becomes a political decision — accept higher inflation to reduce unemployment, or accept higher unemployment to reduce inflation

The 1960s consensus (Samuelson and Solow, 1960) treated this trade-off as exploitable through monetary and fiscal policy

Why the traditional Phillips curve broke down

The 1970s produced stagflation - simultaneously high inflation and high unemployment - which the traditional Phillips curve could not explain

The 1973 oil shock raised production costs sharply, pushing inflation up

At the same time, the recession that followed pushed unemployment up

Both variables rose together, contradicting the stable inverse relationship the original curve predicted

This empirical failure prompted the development of the expectations-augmented Phillips curve

The expectations-augmented Phillips curve

The expectations-augmented Phillips curve, developed by Milton Friedman (1968) and Edmund Phelps (1967), modifies the traditional model by incorporating inflationary expectations

It distinguishes a short-run trade-off from a vertical long-run curve at the natural rate of unemployment

The short-run Phillips curve (SRPC)

For any given level of inflationary expectations, there is a downward-sloping short-run Phillips curve - the standard inverse trade-off

Workers and firms set wages and prices based on expected inflation

If actual inflation differs from expected, real wages and unemployment are temporarily affected

A rise in actual inflation that exceeds expectations reduces real wages, prompting firms to hire more workers - unemployment falls below the natural rate

This explains why the SRPC slopes downwards in the short run

The long-run Phillips curve (LRPC)

The long-run Phillips curve is vertical at the natural rate of unemployment (NAIRU) - the rate at which inflation neither accelerates nor decelerates

Over time, workers and firms adjust their expectations to actual inflation

Once expectations have fully adjusted, the temporary effect on real wages disappears - unemployment returns to its natural rate

This means there is no long-run trade-off between inflation and unemployment - only the short-run one

The LRPC is therefore vertical at the NAIRU, regardless of the inflation rate

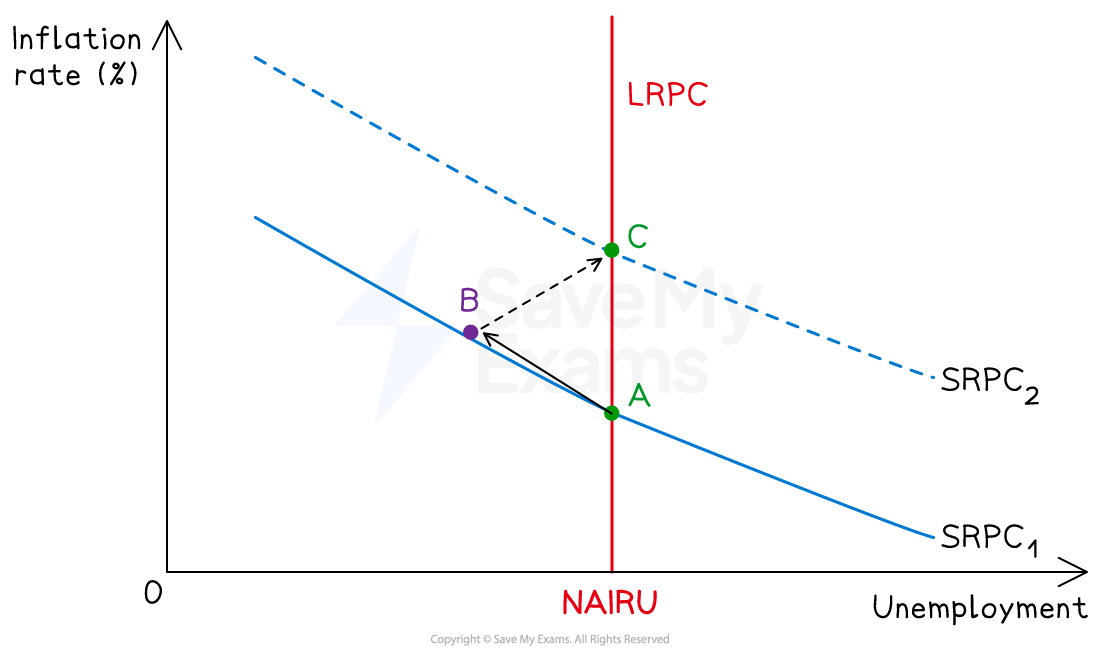

How attempts to exploit the trade-off fail

The expectations-augmented theory predicts that any attempt by policymakers to push unemployment below the NAIRU through expansionary policy will fail in the long run

Initially, expansionary monetary policy raises AD, and inflation rises, real wages fall, unemployment falls below NAIRU

The economy moves up the SRPC from point A to point B

Workers observe the higher inflation and revise their expectations upwards

The SRPC shifts upwards as inflation expectations rise

Real wages return to their original level, firms reduce hiring, and unemployment returns to the NAIRU - but at a higher rate of inflation (point C)

Any further attempt to reduce unemployment below NAIRU repeats this process - the SRPC shifts up again, locking in higher inflation without lasting employment gains

The natural rate of unemployment (NAIRU)

NAIRU stands for the Non-Accelerating Inflation Rate of Unemployment

This is the level of unemployment consistent with stable inflation

Below NAIRU, inflation accelerates as expectations rise

Above NAIRU, inflation decelerates as expectations fall

The NAIRU is determined by structural factors such as labour market flexibility, skills mismatch, frictional unemployment, regulation

Reducing the NAIRU itself requires supply-side policies (training, deregulation, improved job matching) rather than demand-side stimulus

Comparing the two theories

Feature | Traditional Phillips curve | Expectations-augmented Phillips curve |

|---|---|---|

Shape |

|

|

Trade-off in long run |

|

|

Role of expectations |

|

|

Implication for monetary policy |

|

|

How to reduce unemployment permanently |

|

|

Explained by 1970s stagflation? |

|

|

Why the disagreement matters for policy

Under the traditional view, monetary policy is a powerful tool, as central banks can fine-tune the inflation-unemployment mix

Under the expectations-augmented view, monetary policy can only manage inflation expectations in the long run; unemployment is determined by supply-side conditions

Modern central banks largely operate under the expectations-augmented framework

They target inflation explicitly (e.g. the Bank of England's 2% target) and treat unemployment as primarily a supply-side issue

Examiner Tips and Tricks

Use the expectations-augmented version as the default, not the traditional one. Strong essay answers introduce the original Phillips curve briefly, explain why it broke down in the 1970s, and then build the analysis around SRPC, LRPC, and NAIRU. Candidates who treat the traditional curve as the main framework miss the modern theoretical understanding.

Diagrams are essential for this topic. Mark schemes expect candidates to draw at least the SRPC and LRPC, with NAIRU labelled and the vertical LRPC at the NAIRU. A more sophisticated diagram showing SRPC shifting upwards as expectations adjust earns higher analysis marks. Show the path A → B → C clearly when discussing how attempts to exploit the trade-off fail.

Use the post-2021 global inflation episode as an evaluative anchor. Central banks raised rates aggressively in 2022–2023 to prevent inflation expectations from un-anchoring - exactly the concern the expectations-augmented framework predicts. The episode shows the framework remains influential in real-world policy, even if the precise NAIRU is uncertain.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?