Macroeconomic Equilibrium (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

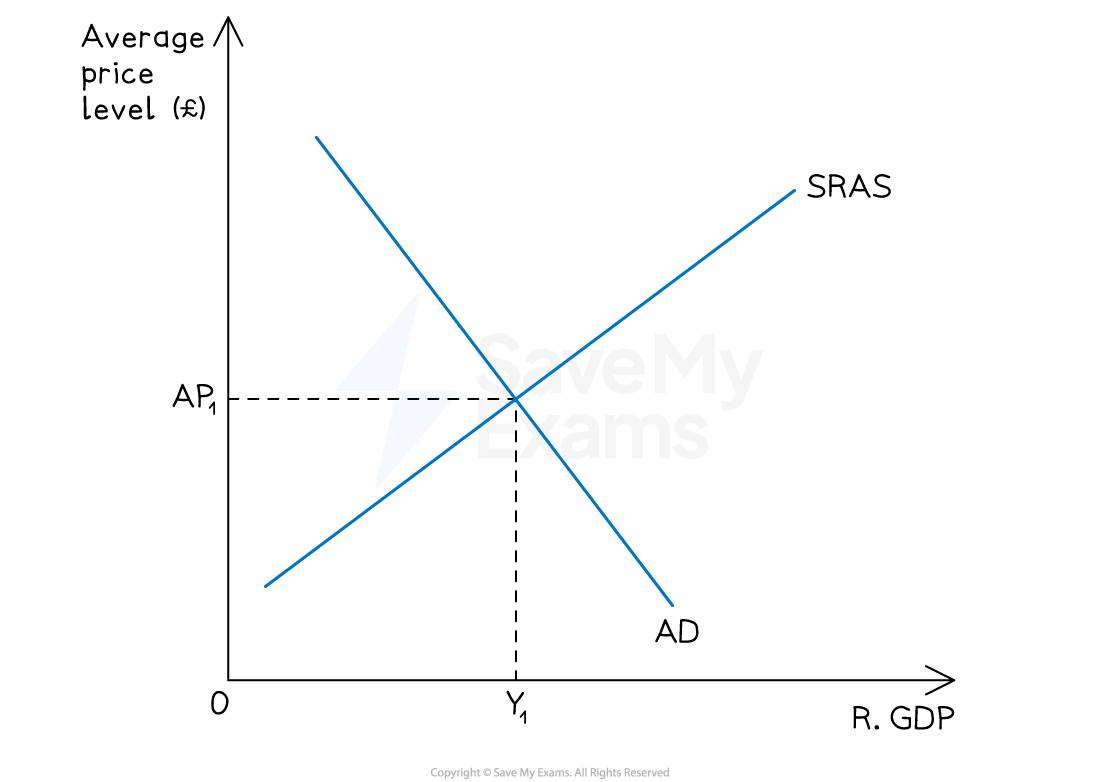

Short-run macroeconomic equilibrium

Real national output equilibrium occurs where aggregate demand (AD) intersects with short-run aggregate supply (SRAS)

Diagram analysis

This economy is in short run equilibrium at AP1Y1

Any changes to the components of AD will cause the AD curve to shift left or right, creating a new short-run equilibrium

Any changes to the determinants of SRAS will shift the SRAS curve left or right, creating a new short-run equilibrium

The level of employment in the economy is determined by the equilibrium level of output - at Y1, firms require a corresponding level of workers to produce that output

If equilibrium output rises, employment rises; if equilibrium output falls, employment falls

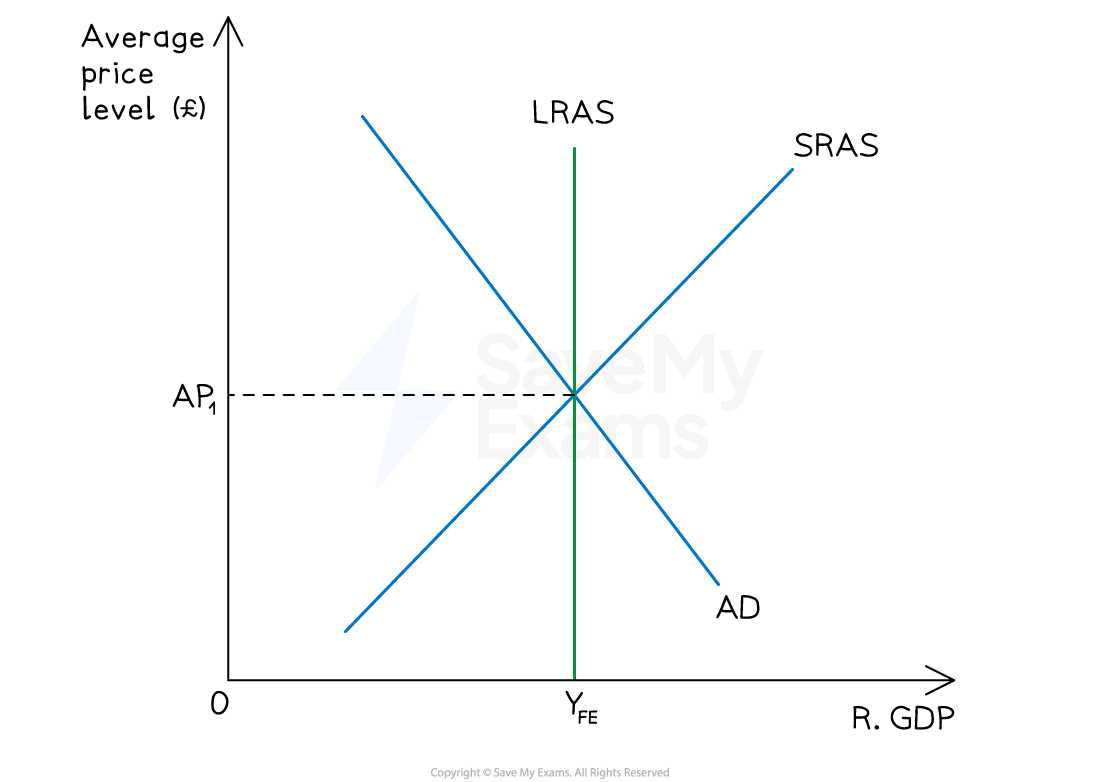

Long-run macroeconomic equilibrium

Free market economists believe that the economy will always return to its normal capacity level of output

In the short-run, there will be fluctuations around this capacity level of output

In the long-run, the economy will return to this normal capacity level of output, but perhaps at a different average price level

It is important to understand the long-run macroeconomic equilibrium as it is used to identify positive and negative output gaps in an economy (this is covered in more detail later on)

Diagram analysis

The LRAS curve demonstrates the normal capacity level of output of the economy using all of its scarce resources

The SRAS intersects with AD at the LRAS curve

This economy is producing at the full employment level of output (YFE)

The average price level at YFE is AP1

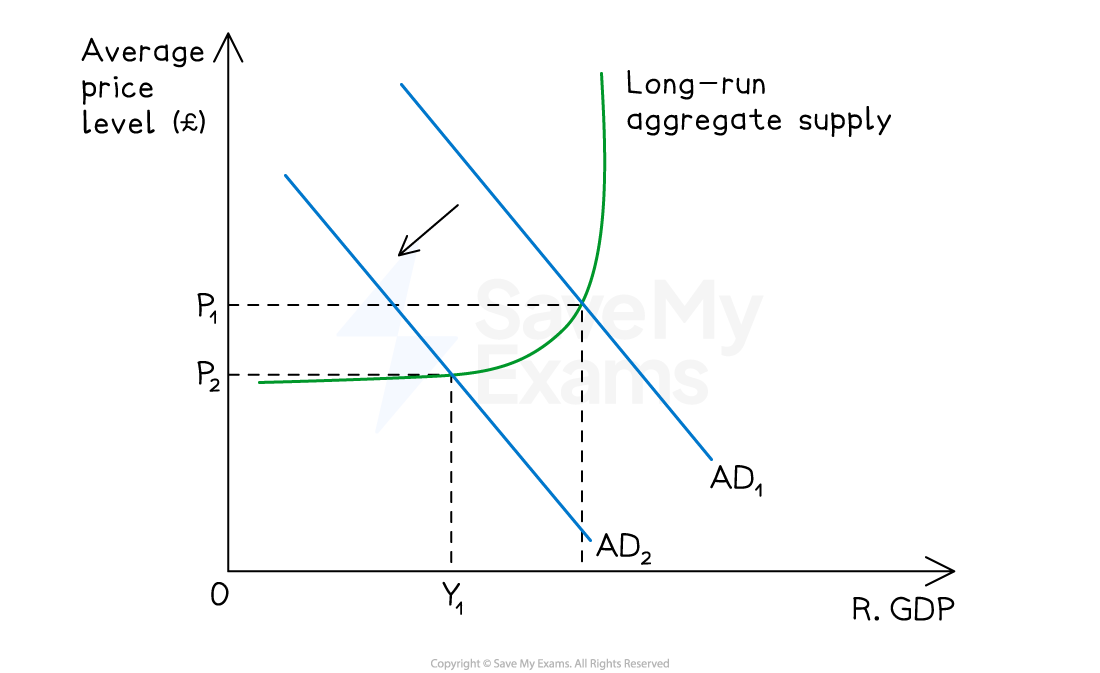

Keynesian long-run equilibrium

The Keynesian view challenges the classical assumption that the economy will always return to full employment output

In the Keynesian model, the economy can settle in long-run equilibrium below full employment - where AD intersects the elastic section of the Keynesian LRAS

At this point, there is significant spare capacity and unemployment in the economy

The price level is stable because spare resources can be brought into production without bidding up factor prices

The economy will not automatically self-correct - without government intervention it may remain at this low output equilibrium indefinitely

Diagram analysis

The economy is initially in equilibrium at P1YFE - at the full employment level of output on the vertical section of the Keynesian LRAS

A fall in AD causes the AD curve to shift left from AD1 to AD2

The new equilibrium is at P2Y1 - below the full employment level of output YFE

There is now a negative output gap equal to Y1YFE - the economy is producing below its potential

The price level has fallen from P1 to P2 - the economy is on the upward-sloping section of the Keynesian LRAS where both output and price level changes occur

Unlike the classical model, the economy will not automatically return to YFE - wages and prices are sticky downwards and the self-correction mechanism breaks down at low levels of output

This provides the Keynesian justification for government intervention - an increase in AD via expansionary fiscal policy can shift AD2 back rightward, raising output and employment back towards YFE

Aggregate demand and supply analysis

1. An increase in aggregate demand (AD)

Diagram analysis

The initial equilibrium level of output was at AP1Y1

An increase in one of the components of AD (e.g. consumption) causes the AD to increase AD1→AD2

Average prices in the economy rise to AP2 and the real level of output increases to Y2

The new short-run equilibrium is at AP2Y2

As output rises from Y1 to Y2, firms require more workers to meet higher demand - employment rises; conversely a fall in AD would reduce output and employment

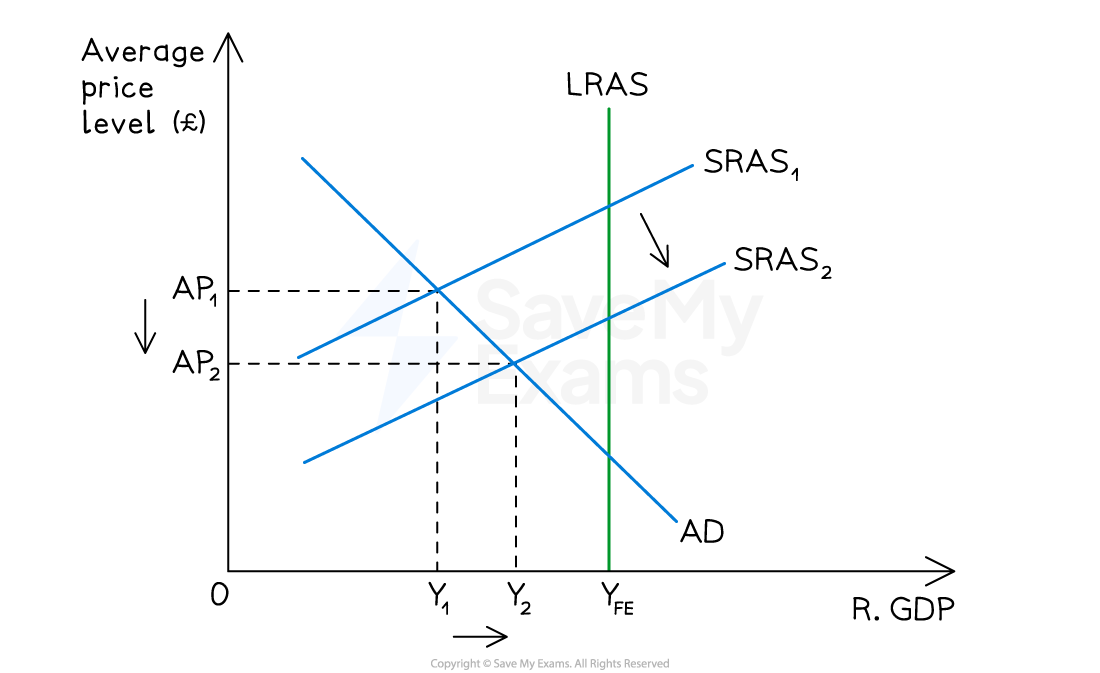

2. An increase in short run aggregate supply (SRAS)

Diagram analysis

The initial equilibrium level of output was at AP1Y1

This equilibrium represents a negative output gap equal to Y1YFE

An increase in one of the determinants of SRAS (e.g. productivity) causes the SRAS to increase SRAS1→SRAS2

Average prices in the economy fall to AP2 and the real level of output increases to Y2

The new short-run equilibrium is at AP2Y2

There is still a negative output gap but it is smaller (Y2YFE)

As output rises from Y1 to Y2, more workers are needed in production - employment rises and the negative output gap narrows, meaning unemployment falls though it does not return to zero until YFE is reached

Worked Example

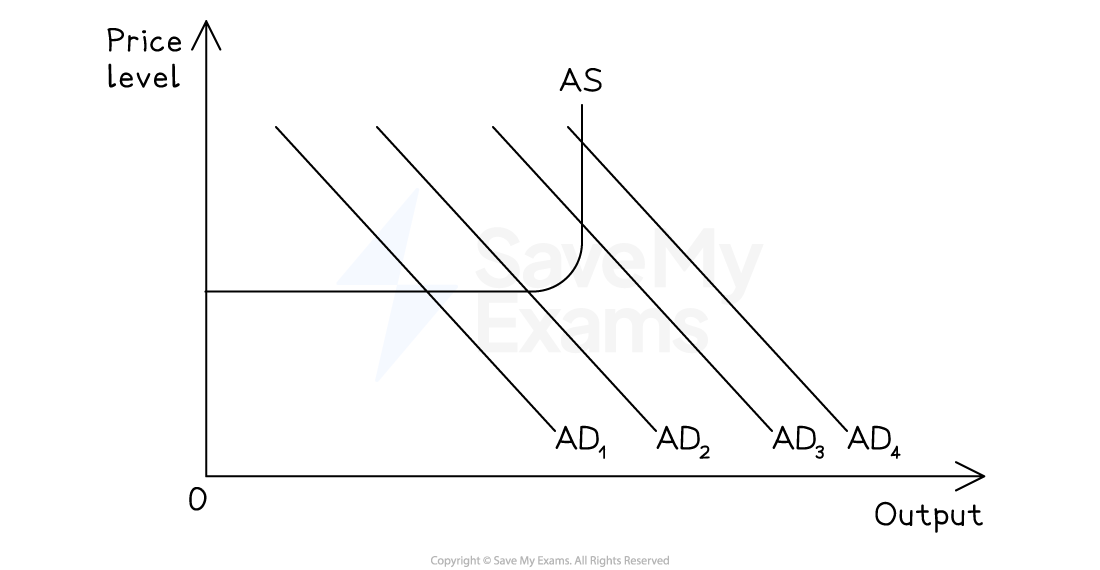

A government has increased output with no effect on the price level.

What must have been the initial level of aggregate demand?

A. AD1 B. AD2 C. AD3 D. AD4

Answer: A - AD1

Worked solution

This question tests understanding of the Keynesian LRAS and which section of the curve the economy is operating on.

The key condition in the question is that output increased with no effect on the price level. This can only occur on the highly elastic (flat) section of the Keynesian LRAS - where there is significant spare capacity and unemployment, so firms can increase output by drawing on idle resources without bidding up factor prices.

If AD shifts right from a position on the elastic section, real output rises, but the price level remains unchanged

If the economy were already on the upward-sloping or vertical section, any rightward shift in AD would raise the price level

Examiner Tips and Tricks

Always state the effect on all three variables when analysing an AD or AS shift - real output, the price level, and employment.

A common error is to identify the new equilibrium price and output but forget employment entirely. Remember that employment moves in the same direction as real output - rising output means firms need more workers; falling output means fewer workers are needed.

For the Keynesian model, always identify which section of the LRAS the economy is operating on before analysing the effect of an AD shift. A rightward shift in AD on the elastic section raises output without raising prices and increases employment - the same shift on the vertical section is purely inflationary with no output or employment effect.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?