Foreign Direct Investment (FDI) & External Investment (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

External capital flow that affect developing economies

FDI is an equity flow — foreign firms acquire ownership of productive assets in the host economy

External debt is a credit flow — the host country borrows from foreign lenders and is obliged to repay

FDI and external debt are two of the main forms of external capital flow that affect developing economies — alongside aid and remittances

Both can support development, but both also carry significant risks if poorly managed

FDI brings risk-sharing (the foreign investor bears losses if the project fails), while external debt creates fixed repayment obligations regardless of how the borrowed funds perform

Foreign direct investment (FDI)

Foreign Direct Investment (FDI) is long-term cross-border investment in productive assets (factories, equipment, infrastructure) by foreign firms establishing or expanding operations abroad

The investing firm acquires significant ownership and control - typically defined as a stake of 10% or more in the host-country entity

FDI is the main vehicle through which multinational companies operate internationally

FDI is distinct from portfolio investment, which involves the purchase of shares or bonds without controlling stakes and is far more volatile

FDI typically involves a long-term commitment, making it more stable than portfolio flows that can reverse rapidly during financial stress

Consequences of FDI

The consequences overlap with those of MNCs, but should be understood as the effects of the capital flow itself, not the firm

Positive consequences

Consequence | Explanation |

|---|---|

Fills the savings gap |

|

Job creation |

|

Technology and skills transfer |

|

Tax revenue |

|

Export earnings |

|

More stable than portfolio flows |

|

Negative consequences

Consequence | Explanation |

|---|---|

Profit repatriation |

|

Limited local linkages |

|

Crowding out |

|

Tax avoidance |

|

Vulnerability to MNC decisions |

|

External debt

External debt is owed to foreign creditors - including foreign governments, international financial institutions and private bondholders

Most low- and middle-income economies carry some external debt; problems arise when the burden becomes unsustainable

Cause | Explanation |

|---|---|

Borrowing for development |

|

Persistent trade deficits |

|

External shocks |

|

Rising global interest rates |

|

Currency depreciation |

|

Capital flight |

|

Lender enthusiasm |

|

Consequences of debt

Debt is not inherently negative - borrowing for productive investment can support growth

The problems arise when debt becomes excessive or is used unproductively

Negative consequences

Consequence | Explanation |

|---|---|

Debt service burden |

|

Crowding out public spending |

|

Currency risk |

|

Loss of policy autonomy |

|

Sovereign default risk |

|

Debt overhang |

|

Case Study

Sri Lanka's 2022 Debt Crisis

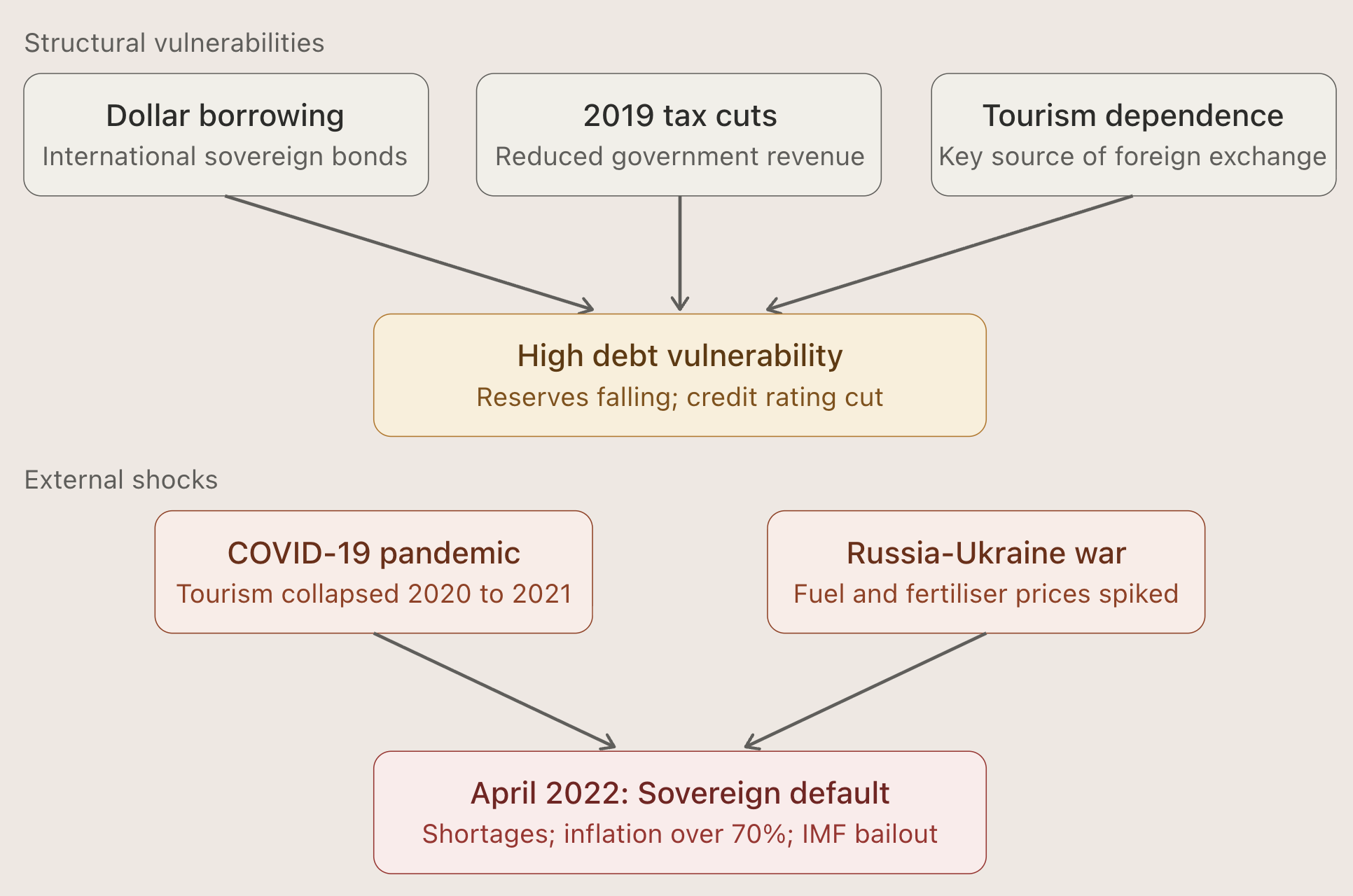

Context

After the end of its civil war in 2009, Sri Lanka pursued ambitious infrastructure-led development funded substantially through external borrowing — including international sovereign bonds, loans from China for infrastructure projects, and multilateral lending. Debt-to-GDP rose sharply through the 2010s.

Causes of the crisis

Heavy reliance on foreign-currency external debt, particularly US dollar-denominated international sovereign bonds

2019 tax cuts that reduced government revenue and widened fiscal deficits

COVID-19 collapse of tourism in 2020–21 — Sri Lanka's largest source of foreign exchange

2022 Russian invasion of Ukraine raised global fuel and fertiliser prices, draining reserves

Loss of access to international capital markets as credit ratings fell

Outcomes

April 2022: Sri Lanka announced its first sovereign default in its history

Severe shortages of fuel, food and medicine triggered mass protests and the resignation of the President

Inflation peaked above 70% in 2022; the rupee lost more than half its value against the dollar

IMF bailout agreement of approximately US$3 billion approved in March 2023, requiring tax increases and spending reforms

Debt restructuring with bilateral creditors (including China and India) and private bondholders followed

Poverty rates rose sharply; long-term economic damage will take years to reverse

The Sri Lankan case illustrates how external debt vulnerability can compound rapidly when external shocks combine with weak domestic fiscal management.

Examiner Tips and Tricks

The strongest analytical move is to distinguish FDI from external debt clearly — FDI involves risk-sharing with the foreign investor; debt creates fixed repayment obligations regardless of project success. This distinction is the foundation of higher-mark answers comparing the two flows.

For FDI evaluation, the two strongest critical points are profit repatriation (which reduces long-run host benefits) and limited local linkages (which reduces the multiplier effect when MNCs import most inputs).

For debt evaluation, distinguish between debt for productive investment (supports growth if returns exceed interest costs) and debt for consumption or non-productive uses (creates obligations without revenue to service them). The currency denomination matters too — foreign-currency debt carries exchange rate risk that local-currency debt does not.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?