Causes & Effects of Changing Exchange Rates (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

Changes in the exchange rate under different systems

Changes under a floating system

Under a freely floating exchange rate, the rate changes continuously in response to:

Interest rate differentials

Higher domestic interest rates attract capital inflows (hot money), increasing demand for the currency and causing appreciation

Inflation differentials

Higher domestic inflation makes exports less competitive, reducing export demand and causing depreciation; this is the basis of purchasing power parity (PPP) theory

Current account movements

A current account deficit means more domestic currency is being sold to buy foreign goods and services, putting downward pressure on the rate

Speculation

If traders expect a currency to fall, they sell it now, creating a self-fulfilling depreciation; conversely, expected appreciation attracts speculative buying

Economic performance and confidence

Strong growth and political stability attract FDI and portfolio investment, increasing currency demand

Changes under a fixed system

The exchange rate does not change as a result of market forces - the central bank neutralises market pressure through intervention

The rate can only change through a deliberate policy decision (devaluation or revaluation)

If market pressure against the peg becomes overwhelming - for example, if a current account deficit persists and reserves are depleted - the peg may be forced to collapse, as occurred in the 1992 ERM crisis when sterling was forced out of the European Exchange Rate Mechanism

Changes under a managed float

The rate moves with market forces within informal limits

The central bank intervenes to 'lean against the wind' - selling the currency if it rises too far, buying if it falls too far

The rate can trend in one direction over time if fundamentals support it, unlike a strict fixed rate

The Marshall-Lerner Condition and J-Curve

The Marshall-Lerner condition states that a currency depreciation will improve the current account only if the sum of the price elasticities of demand for exports and imports exceeds one

PED(X) + PED(M) > 1

When the condition is satisfied, the volume response to the price change is large enough to outweigh the adverse initial price effect, and the current account improves

When the condition is not satisfied (PED(X) + PED(M) < 1), demand for both exports and imports is too inelastic — the current account worsens following depreciation

This follows the revenue rule which states that in order to increase revenue, firms should lower prices for products that are price elastic in demand

If the combined elasticity of exports/imports is less than 1 (inelastic), a depreciation (fall in price) will actually worsen the current account balance

The J-Curve effect

It is also important to recognise that there is a time lag between the depreciation of the currency and any subsequent improvement in the current account balance

This time lag is explained by the J-Curve effect

It takes time for firms and consumers to respond to changes in price

Once it becomes evident that price changes will last for a longer period of time, firms and consumers change their patterns

E.g. a firm in the USA has been importing electric scooters from the UK. If the Euro depreciates, the price of scooters in France becomes relatively cheaper. In the short term, the USA firm will not switch immediately to purchasing scooters from France, as the exchange rate may soon bounce back. They also have a positive relationship with their UK suppliers. In the long term they are likely to switch

The J Curve explains what happens to a trade balance over time when the country's currency depreciates

Diagram analysis

In the short run, the sum of PEDs for exports and imports was less than one / inelastic (or the Marshall-Lerner condition was not fulfilled) so the deficit widens

However, in the long run the Marshall-Lerner condition is met so it leads to a surplus

With any currency depreciation/devaluation, the trade balance will initially worsen before it improves

Existing contracts - firms and households are locked into import and export contracts agreed at the old exchange rate; until these expire, trade volumes cannot adjust to the new relative prices

Consumer habits and brand loyalty - buyers do not switch suppliers immediately following a price change; it takes time for consumers and firms to identify cheaper alternatives, trial them and build new supply relationships

Supply-side capacity constraints - domestic export industries cannot instantly scale up production to meet increased foreign demand following depreciation; new capacity takes time to build, meaning export volumes rise only gradually even when export prices have fallen

Case Study

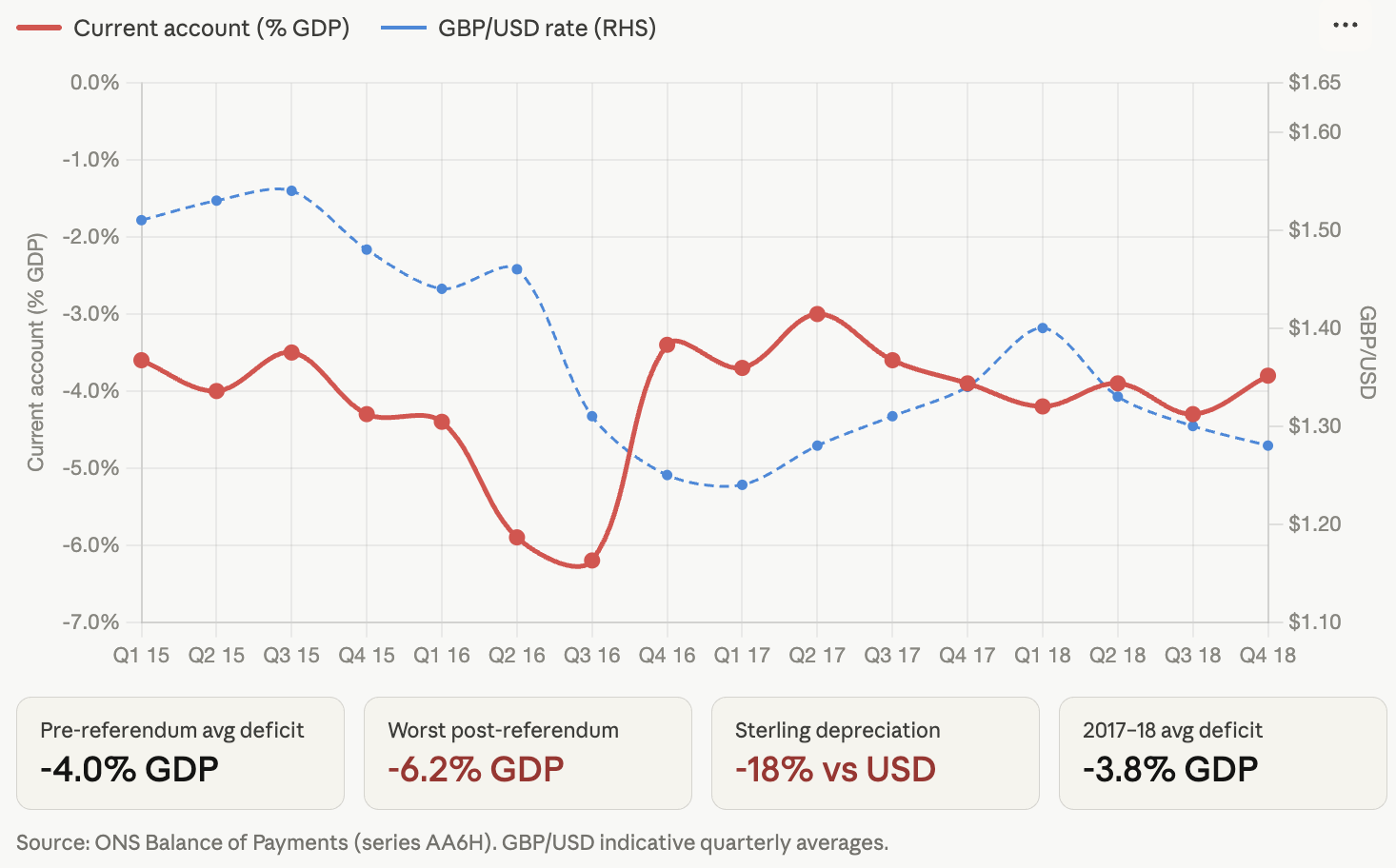

UK current account following the Brexit depreciation, 2016–2018

The context

Following the Brexit referendum in June 2016, sterling depreciated approximately 15% on a trade-weighted basis - one of the largest peacetime depreciations of a major currency in modern history. With the UK running a persistent current account deficit of around 5–6% of GDP, the depreciation provided a near-perfect real-world test of both the Marshall-Lerner condition and the J-curve effect.

Actions taken

Sterling fell from approximately £1 = $1.48 to £1 = $1.22 by January 2017 — an 18% depreciation against the US dollar

The Bank of England cut interest rates and expanded quantitative easing in August 2016, reinforcing the depreciation

The UK remained in the EU single market during transition, meaning trade barriers were unchanged

Outcomes

In the short run the current account deficit widened, consistent with J-curve theory - import costs rose immediately while export volumes were slow to respond due to existing contracts and capacity constraints

UK goods export volumes began rising from mid-2017 as foreign buyers responded to lower sterling prices, consistent with the Marshall-Lerner condition being met in the long run

However, the deficit remained above 3% of GDP through 2018 — suggesting PED for UK exports and imports was relatively inelastic, and that Brexit uncertainty constrained the full Marshall-Lerner improvement

The case illustrates that even when the condition is met, structural factors can limit the scale of current account improvement

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?