Demand for Money & Interest Rate Determination (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

The demand for money and interest rate determination

The interest rate is the price of money, determined where demand meets supply.

Keynes's liquidity preference theory explains interest rates through the demand for and supply of money itself

Classical loanable funds theory explains them through the demand for and supply of funds available for lending

The demand for money: liquidity preference theory

Liquidity preference is the desire to hold wealth in the form of money (the most liquid asset) rather than in less liquid financial assets such as bonds

Keynes identified three motives for holding money

The three motives

Motive | Purpose | Sensitivity to interest rates |

|---|---|---|

Transactions |

|

|

Precautionary |

|

|

Speculative |

|

|

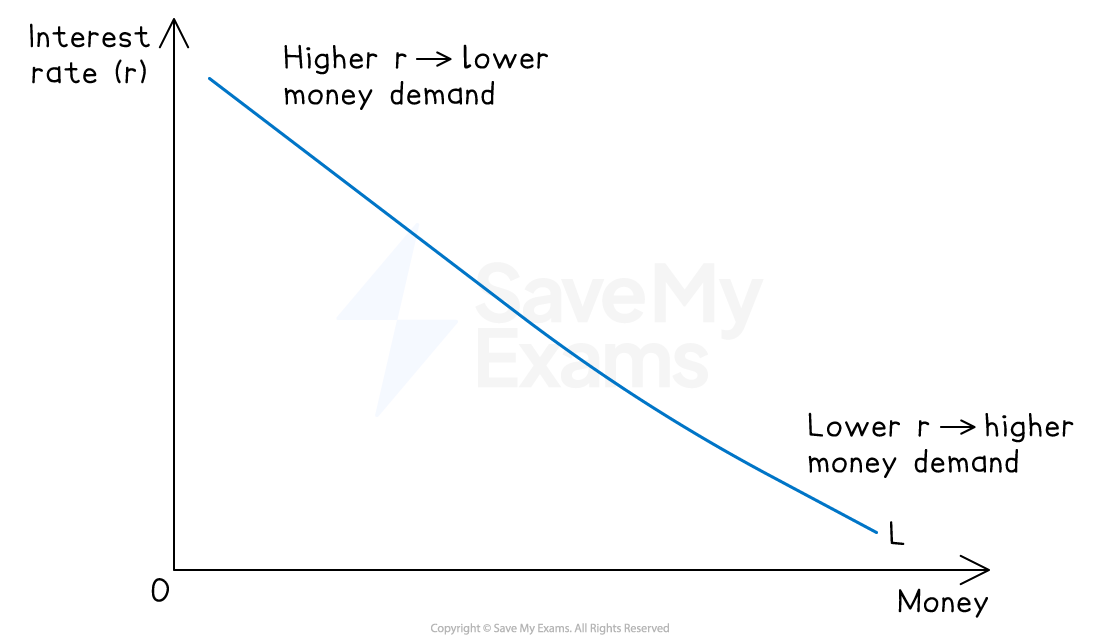

Total demand for money

Adding the three motives together gives the total demand for money curve (L), which slopes downwards against the interest rate

Higher interest rates increase the opportunity cost of holding money, reducing money demand

Lower interest rates reduce the opportunity cost of holding money, increasing money demand

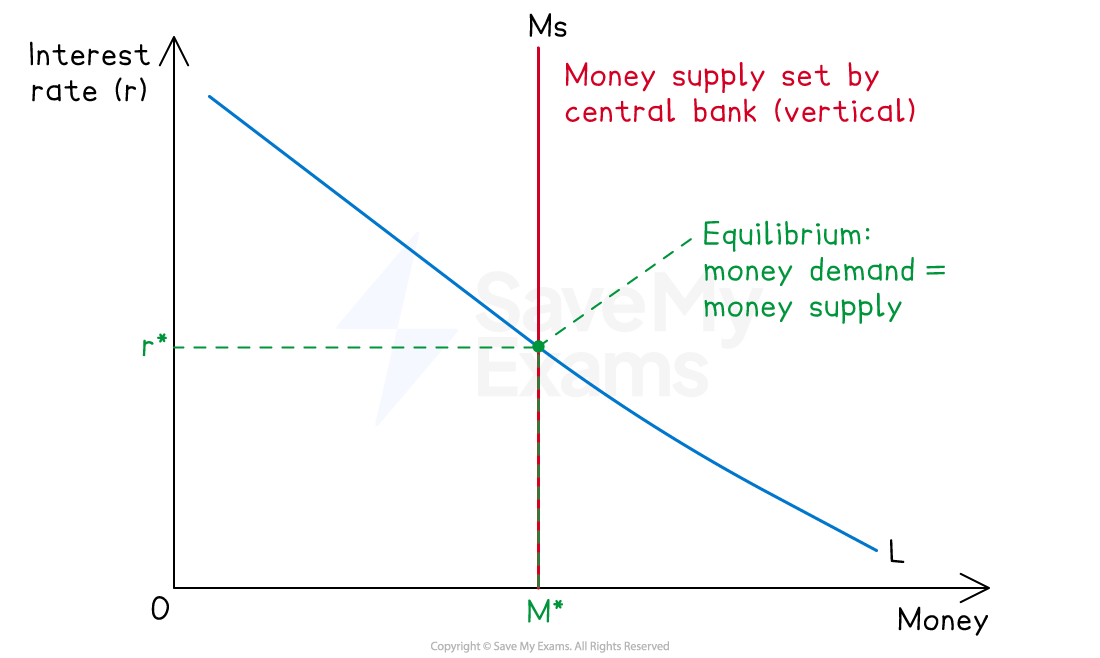

Interest rate determination: liquidity preference theory

The supply of money (Ms) is set by the central bank and is usually drawn as vertical

It does not respond to the interest rate

The equilibrium interest rate is where money demand equals money supply

Changes in money supply or money demand shift the curves and change the equilibrium interest rate

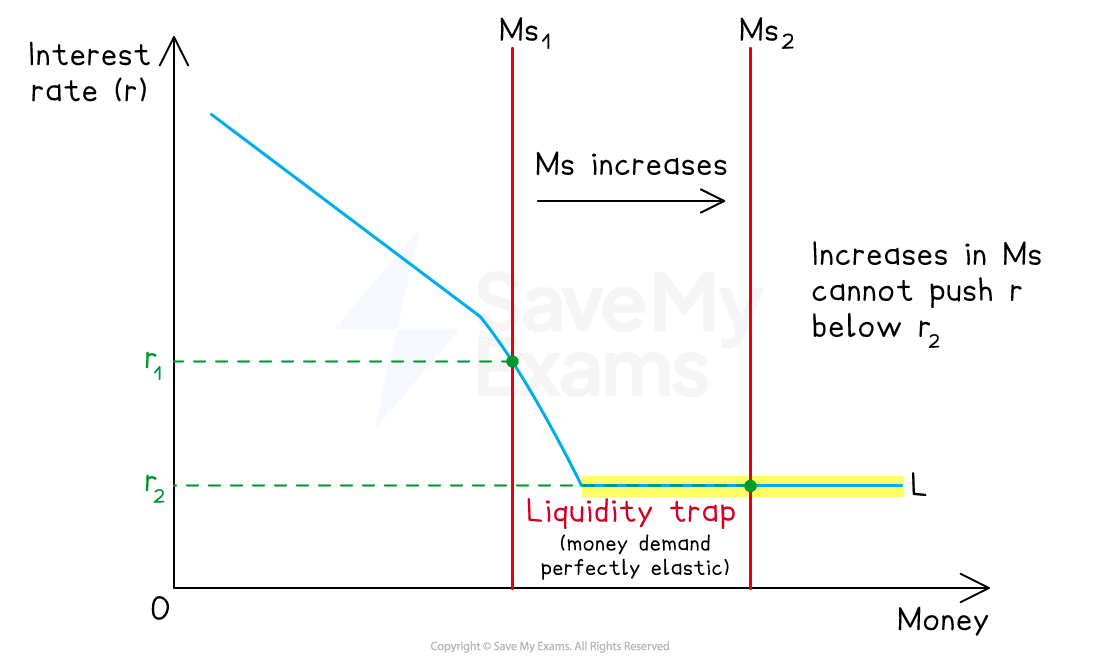

The liquidity trap

The liquidity trap is a situation in which interest rates are so low that money demand becomes perfectly elastic

Any increase in money supply is absorbed into idle balances rather than reducing interest rates further

At very low interest rates, everyone expects rates to rise and bond prices to fall - so no one wants to hold bonds

Money supply increases have no effect on interest rates - the liquidity preference curve becomes horizontal

Monetary policy loses its effectiveness in stimulating the economy - implications for central banks are significant, particularly during recessions

The Bank of England faced this problem after the 2008 financial crisis, which is one reason quantitative easing was introduced

Interest rate determination: loanable funds theory

Loanable funds theory is the classical view that the interest rate is determined by the demand for and supply of funds available for borrowing and lending in the financial market

How does it work?

Supply of loanable funds comes from savings - households with surplus income lend to borrowers

The higher the interest rate, the greater the reward for saving, so supply of loanable funds rises with the interest rate

Demand for loanable funds comes from borrowers - firms seeking to invest and households seeking to borrow

The higher the interest rate, the higher the cost of borrowing, so demand for loanable funds falls as the interest rate rises

Equilibrium interest rate is set where supply of savings equals demand for borrowing

Key implication

In the loanable funds view, the interest rate coordinates saving and investment decisions over time

A rise in saving pushes down interest rates and encourages investment — the classical mechanism by which economies self-correct

Comparing the two theories

Feature | Liquidity preference (Keynes) | Loanable funds (Classical) |

|---|---|---|

What determines the interest rate |

|

|

Role of the central bank |

|

|

Role of saving |

|

|

Why people hold money |

|

|

Implication for monetary policy |

|

|

Short run vs long run |

|

|

Why the disagreement matters

Keynes argued that the classical view misses the speculative motive for holding money

Saving is not automatically channelled into investment because some of it is held as idle balances

This is why Keynes believed an increase in saving could reduce aggregate demand without reducing interest rates enough to stimulate offsetting investment

Modern economic thinking often treats the two theories as complementary rather than mutually exclusive

Liquidity preference explains short-run interest rate movements driven by monetary policy

Loanable funds explains long-run rates driven by real saving and investment decisions

Worked Example

Explain the role of liquidity preference in the determination of interest rates and assess its importance. [12 marks]

Indicative answer structure

AO1 Knowledge: Define liquidity preference; identify the three motives for holding money (transactions, precautionary, speculative); state that the interest rate is determined where money demand equals money supply

AO2 Analysis: Explain why the liquidity preference curve slopes downwards - higher interest rates raise the opportunity cost of holding money; explain how a change in money supply (vertical Ms curve) shifts the equilibrium interest rate; explain the liquidity trap as a special case where money demand becomes perfectly elastic

AO3 Evaluation: Liquidity preference matters for understanding short-run interest rate movements and the effectiveness of monetary policy; it explains why monetary policy can fail (liquidity trap); but it is not the only theory - loanable funds theory emphasises the role of saving and investment in determining long-run rates. Contemporary central banks use liquidity preference insights when setting policy but recognise that real factors (productivity, demographics, global saving) also matter. The theory is important but not sufficient on its own

Examiner Tips and Tricks

In essays, treat the two theories as explaining different aspects of interest rate determination, not as one being right and the other wrong.

Strong answers present liquidity preference as the short-run, monetary-policy-relevant theory, and loanable funds as the long-run, saving-investment-relevant theory. Candidates who pick a side without acknowledging the other miss evaluation marks.

Diagrams are essential for this topic - particularly for liquidity preference. A correctly labelled liquidity preference diagram (L curve, vertical Ms, equilibrium r*) is expected and rewarded. For the liquidity trap, show the horizontal section at low interest rates explicitly.

Use the post-2008 quantitative easing episode as an evaluative anchor for the liquidity trap. Central banks faced near-zero interest rates and conventional monetary policy had stopped working - exactly the situation Keynes described. QE was the policy response. This links the theory directly to contemporary policy and strengthens evaluation.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?