Evaluating Policies to Reduce Inflation (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

How best to tackle inflation

Inflation is reduced by policies that slow aggregate demand growth, shift aggregate supply rightwards, or anchor inflationary expectations

The three main policy categories are:

contractionary monetary policy

contractionary fiscal policy, and

supply-side policy

Contractionary monetary policy

Contractionary monetary policy is the use of higher interest rates, reduced money supply growth, or quantitative tightening to reduce aggregate demand and inflationary pressure

Mechanism (the transmission mechanism)

The central bank raises the base interest rate

Commercial bank lending rates rise, mortgage and loan repayments become more expensive

Consumer spending falls (higher cost of credit, higher savings returns)

Investment falls (higher cost of borrowing for firms)

The exchange rate appreciates as foreign capital is attracted by higher returns, reducing export demand

Aggregate demand falls, reducing demand-pull inflationary pressure

Strengths and limitations

Strengths | Limitations |

|---|---|

|

|

|

|

|

|

|

|

Contractionary fiscal policy

Contractionary fiscal policy is the use of higher taxation, reduced government spending, or both, to reduce aggregate demand and inflationary pressure

Mechanism

The government raises direct or indirect taxes, reducing household disposable income and firm profits

Government reduces spending on public services, transfer payments, or infrastructure

Aggregate demand falls, reducing demand-pull inflationary pressure

A budget surplus (or smaller deficit) may also reduce the money supply if bonds previously financing the deficit are no longer issued

Strengths and limitations

Strengths | Limitations |

|---|---|

|

|

|

|

|

|

|

|

Supply-side policy

Supply-side policy aims to reduce inflation by increasing the productive capacity of the economy, shifting long-run aggregate supply (LRAS) rightwards and allowing output to rise without price pressure

Mechanism

Market-based policies (deregulation, tax cuts to incentivise work and investment, privatisation) increase productivity and reduce costs

Interventionist policies (education and training, infrastructure investment, R&D subsidies) raise long-run productive capacity

LRAS shifts right, so any given level of AD is met at a lower price level

Addresses cost-push inflation by reducing underlying production costs

Strengths and limitations

Strengths | Limitations |

|---|---|

|

|

|

|

|

|

|

|

Comparing the effectiveness of each

Policy | Best against | Key weakness |

|---|---|---|

Contractionary monetary |

|

|

Contractionary fiscal |

|

|

Supply-side |

|

|

The strongest policy mix typically combines all three

Monetary policy for short-term demand management

Fiscal policy for targeted adjustments, and

Supply-side policy for long-run capacity building

The choice depends on the cause of inflation

Demand-pull inflation responds to monetary and fiscal policy

Cost-push inflation responds better to supply-side policy

Case Study

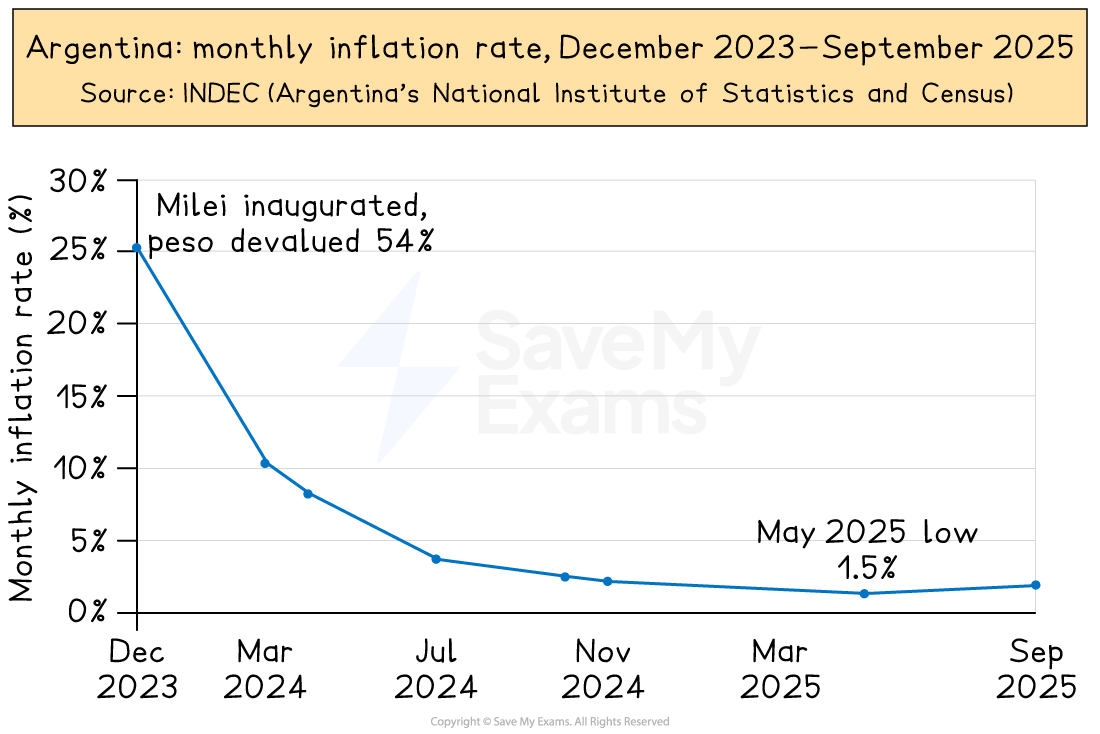

Argentina's anti-inflation programme, 2023 onwards

The context

When Javier Milei took office in December 2023, Argentina faced one of the world's highest inflation rates. Monthly inflation had reached 25.5% and annual inflation peaked at nearly 300% in April 2024.

The underlying cause was structural: decades of budget deficits financed by the central bank printing money - the quantity theory of money operating in practice.

The policy mix

The Milei administration combined all three anti-inflation policies

Contractionary fiscal policy - spending cut by 4.5% of GDP through subsidy elimination and public sector workforce reductions; first fiscal surplus in 14 years at 1.8% of GDP in 2024

Contractionary monetary policy - central bank prohibited from printing new pesos to fund government spending; broad money supply frozen; immediate 54% peso devaluation

Supply-side reform - deregulation, rollback of price controls, labour market liberalisation

The results

Monthly inflation fell from 25.5% in December 2023 to 2.1% by September 2025. Annual inflation decreased to 31.8% by November 2025, the lowest level in more than seven years. The current account moved from a 3.2% of GDP deficit to a 1% surplus in 2024.

The costs

Poverty rose from 42% in late 2023 to 53% in the first half of 2024 before recovering. GDP contracted by around 3.8% in 2024.

What this illustrates

The three policies worked together, not separately. Fiscal consolidation removed the root cause; monetary tightening anchored expectations; structural reform addressed long-run cost pressures

Short-term costs were substantial - rising poverty and unemployment confirm that contractionary policies impose unemployment costs, illustrating the conflict with other macroeconomic objectives

Credibility matters - central bank independence and rules-based policy are important for anti-inflation credibility

Limitations remain - Argentina's overnight interest rate was still around 45%, and annual inflation around 32% by late 2025. Even a successful programme has not returned Argentina to target-level inflation

Examiner Tips and Tricks

The highest-value framing for questions on policy responses to inflation, is to match the policy to the cause of inflation.

Demand-pull inflation responds to monetary and fiscal policy; cost-push inflation responds better to supply-side policy. Candidates who list all three policies without distinguishing what each is best against miss the key evaluation move.

For any policy discussed, evaluation should address time lags, side effects and cause-specificity. Monetary policy takes 12 to 24 months to fully transmit; supply-side policy takes years. Contractionary policies raise unemployment. Supply-side policies have uncertain outcomes. Strong answers weigh these costs against the benefit of reduced inflation.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?