Monetary Policy & Exchange Rate Policy (Cambridge (CIE) A Level Economics): Revision Note

Exam code: 9708

The link between monetary policy and exchange rate policy

Monetary policy uses interest rates and money supply controls to influence aggregate demand and inflation

Exchange rate policy manages the value of a currency to influence trade balance, inflation, and competitiveness

The two are causally linked - interest rate changes drive capital flows that affect the exchange rate, and exchange rate management often relies on monetary policy tools

Recap from AS

The AS syllabus covers the basic tools and effects of both policies

Interest rates as the central bank's main tool

Expansionary vs contractionary monetary policy

Fixed, managed and floating exchange rate regimes

Simple effects of currency appreciation and depreciation

This page builds on that foundation and adds the transmission mechanism in detail, quantitative easing, and the integrated effectiveness analysis of both policies across multiple macroeconomic objectives

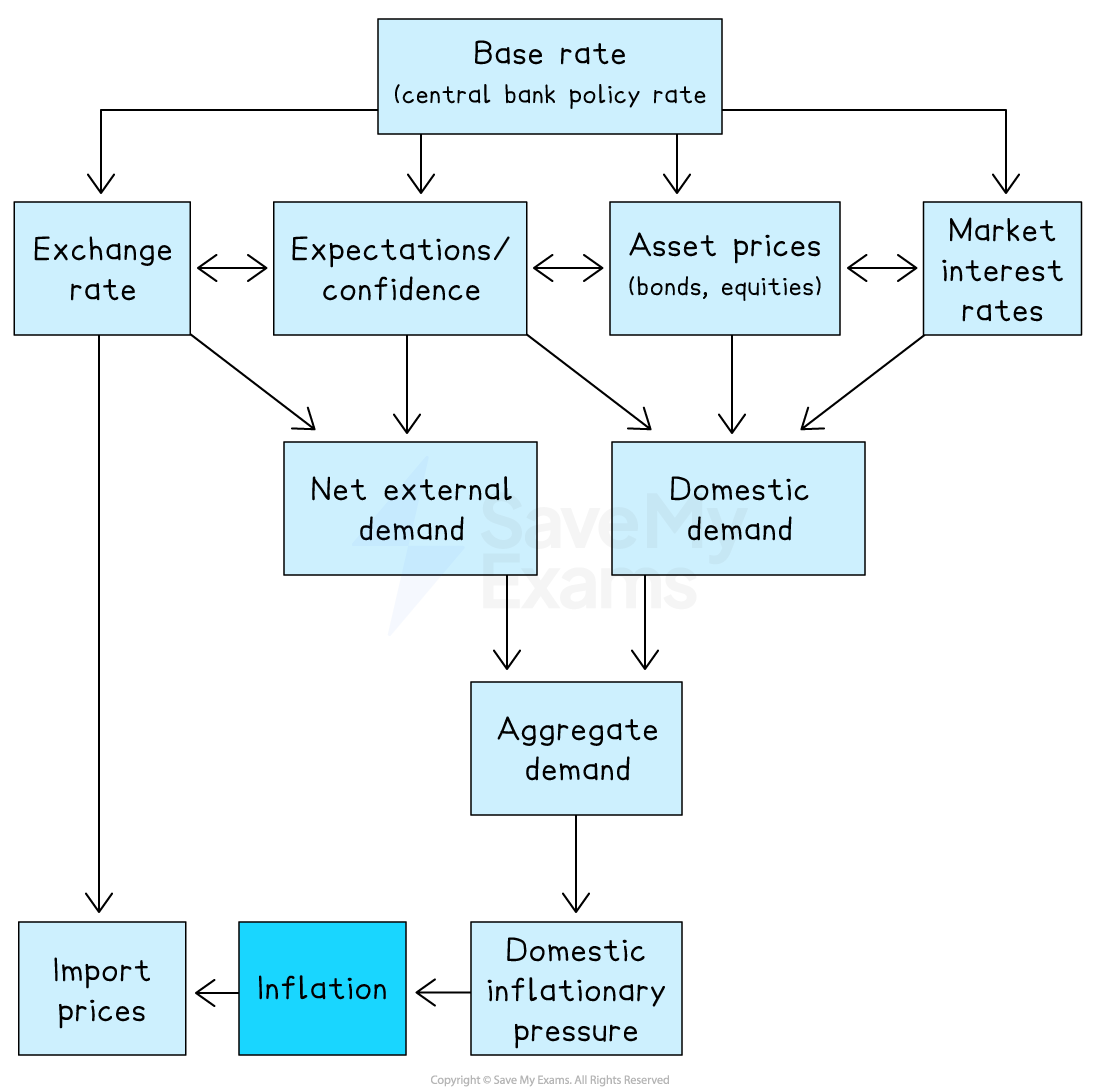

The monetary policy transmission mechanism

The transmission mechanism is the chain of cause-and-effect through which a change in the central bank's policy interest rate affects aggregate demand, output, employment and the price level

The diagram below maps the full mechanism

Base rate changes flow through four transmission channels

Channels feed into demand components, which converge into aggregate demand

Aggregate demand drives domestic inflationary pressure, which feeds inflation

The exchange rate channel also affects inflation directly via import prices, separate from the AD route

A rise in the base rate transmits through the four channels as follows

Channel | Mechanism |

|---|---|

Market interest rates |

|

Asset prices |

|

Expectations / confidence |

|

Exchange rate |

|

The bidirectional arrows in the diagram show the channels also interact

For example, expectations of higher rates can themselves drive asset prices and the exchange rate before official rate changes occur

The combined effect of a rate rise is a fall in aggregate demand

The reverse applies for a rate cut

Time lags and limitations

The full effect of a rate change typically takes 12 to 24 months to materialise

Channels work at different speeds

Exchange rate effects appear within weeks

Market interest rate effects on consumption build over months as fixed-rate deals expire

The mechanism may break down at the zero lower bound (the liquidity trap, covered in 9.4.7)

Channels can be disrupted when commercial banks are repairing damaged balance sheets and fail to pass on rate changes (a key issue post-2008)

Quantitative easing

Quantitative easing is a monetary policy tool in which the central bank creates new reserves electronically and uses them to buy financial assets (typically government bonds), expanding the money supply and reducing long-term interest rates

QE works through the same transmission mechanism but operates on long-term rates rather than the short-term base rate

Bond purchases push prices up and yields down, feeding into the asset prices channel and indirectly into market interest rates

QE is used when conventional monetary policy reaches its limits - typically at the zero lower bound

It was used extensively after the 2008 financial crisis and during the COVID-19 pandemic by major central banks

Limitation

QE may inflate asset prices (housing, equities) more than it stimulates real activity creating distributional concerns and asset bubble risk

Exchange rate policy

Exchange rate policy is the use of central bank intervention, interest rate adjustments, or capital controls to influence the external value of a currency in pursuit of macroeconomic objectives

It operates on the exchange rate channel of the transmission diagram directly

Three regime types

Regime | Description | Implication |

|---|---|---|

Floating |

|

|

Fixed |

|

|

Managed (dirty float) |

|

|

The link with monetary policy: the impossible trinity

Monetary policy and exchange rate policy are not independent tools

They both operate through the exchange rate channel shown in the transmission diagram

A central bank cannot simultaneously control the interest rate and the exchange rate under free capital mobility - this is the impossible trinity (or trilemma)

Choosing a fixed exchange rate means giving up monetary policy independence

Choosing monetary policy independence means accepting exchange rate volatility

Most major economies operate floating exchange rates to preserve monetary policy independence

Effectiveness across macroeconomic objectives

Monetary policy and exchange rate policy work through different (but overlapping) channels and produce different effects across each objective

Objective | Monetary policy | Exchange rate policy |

|---|---|---|

Low inflation |

|

|

Economic growth |

|

|

Low unemployment |

|

|

Balance of payments |

|

|

Equitable income distribution |

|

|

The key insight is that the same policy serves different objectives through different transmission paths, and these paths often conflict

For example, raising rates to control inflation worsens the BoP through the same exchange rate channel that anchors expectations

Strengths and limitations

Strengths | Limitations | |

|---|---|---|

Monetary policy |

|

|

Exchange rate policy |

|

|

Worked Example

Discuss the transmission mechanism of monetary policy and consider why it might not always be effective in achieving the central bank's objectives.

[13 marks]

Indicative answer structure

AO1 Knowledge: Define monetary policy and the transmission mechanism; identify the central bank's main objectives (typically price stability, often growth and employment as secondary)

AO2 Analysis: Walk through the four channels - market interest rates, asset prices, expectations, exchange rate. Show how a rate rise reduces AD through each. Note that the exchange rate channel also affects inflation directly through import prices

AO3 Evaluation: The mechanism may not work effectively because of

Time lags of 12–24 months

The liquidity trap at the zero lower bound

Cost-push inflation that monetary policy cannot address

Broken transmission channels (e.g. impaired banking systems)

Conflicting policy objectives (fighting inflation may worsen unemployment)

Exchange rate effects that conflict with BoP objectives

Conclude that the transmission mechanism is theoretically clear but empirically conditional

Examiner Tips and Tricks

For monetary policy questions, trace the full transmission mechanism rather than just stating that "higher rates reduce AD." The strongest answers walk through all four channels and note that the exchange rate channel feeds into inflation by two routes (via net external demand and directly via import prices). Drawing or describing the diagram structure earns higher analysis marks.

For exchange rate policy questions, the key insight is the impossible trinity

a country cannot simultaneously have a fixed exchange rate, free capital mobility, and independent monetary policy

The strongest answers use this framework to evaluate exchange rate policy choices, showing why countries that fix their currency must sacrifice monetary policy independence.

Use the post-2021 global inflation episode as an evaluative anchor. Major central banks raised rates aggressively from 2022 onwards. The episode showed monetary policy can transmit through the expected channels but with significant time lags and uneven effects across sectors.

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?